MITRAJAYA HOLDINGS BERHAD - Announcements

MITRAJAYA HOLDINGS BERHAD - Announcements

MITRAJAYA HOLDINGS BERHAD - Announcements

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

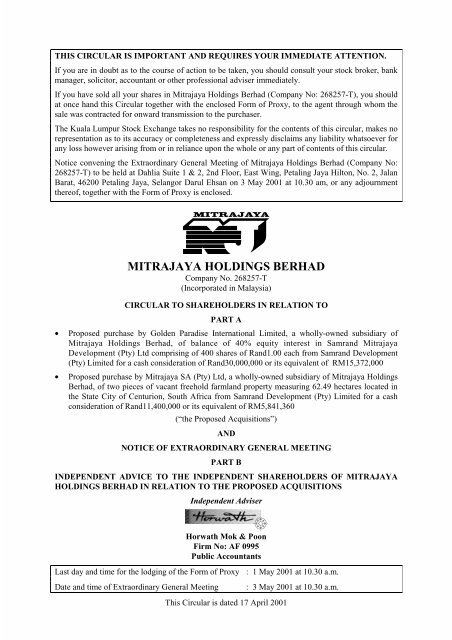

THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION.<br />

If you are in doubt as to the course of action to be taken, you should consult your stock broker, bank<br />

manager, solicitor, accountant or other professional adviser immediately.<br />

If you have sold all your shares in Mitrajaya Holdings Berhad (Company No: 268257-T), you should<br />

at once hand this Circular together with the enclosed Form of Proxy, to the agent through whom the<br />

sale was contracted for onward transmission to the purchaser.<br />

The Kuala Lumpur Stock Exchange takes no responsibility for the contents of this circular, makes no<br />

representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for<br />

any loss however arising from or in reliance upon the whole or any part of contents of this circular.<br />

Notice convening the Extraordinary General Meeting of Mitrajaya Holdings Berhad (Company No:<br />

268257-T) to be held at Dahlia Suite 1 & 2, 2nd Floor, East Wing, Petaling Jaya Hilton, No. 2, Jalan<br />

Barat, 46200 Petaling Jaya, Selangor Darul Ehsan on 3 May 2001 at 10.30 am, or any adjournment<br />

thereof, together with the Form of Proxy is enclosed.<br />

<strong>MITRAJAYA</strong> <strong>HOLDINGS</strong> <strong>BERHAD</strong><br />

Company No. 268257-T<br />

(Incorporated in Malaysia)<br />

CIRCULAR TO SHAREHOLDERS IN RELATION TO<br />

PART A<br />

• Proposed purchase by Golden Paradise International Limited, a wholly-owned subsidiary of<br />

Mitrajaya Holdings Berhad, of balance of 40% equity interest in Samrand Mitrajaya<br />

Development (Pty) Ltd comprising of 400 shares of Rand1.00 each from Samrand Development<br />

(Pty) Limited for a cash consideration of Rand30,000,000 or its equivalent of RM15,372,000<br />

• Proposed purchase by Mitrajaya SA (Pty) Ltd, a wholly-owned subsidiary of Mitrajaya Holdings<br />

Berhad, of two pieces of vacant freehold farmland property measuring 62.49 hectares located in<br />

the State City of Centurion, South Africa from Samrand Development (Pty) Limited for a cash<br />

consideration of Rand11,400,000 or its equivalent of RM5,841,360<br />

(“the Proposed Acquisitions”)<br />

AND<br />

NOTICE OF EXTRAORDINARY GENERAL MEETING<br />

PART B<br />

INDEPENDENT ADVICE TO THE INDEPENDENT SHAREHOLDERS OF <strong>MITRAJAYA</strong><br />

<strong>HOLDINGS</strong> <strong>BERHAD</strong> IN RELATION TO THE PROPOSED ACQUISITIONS<br />

Independent Adviser<br />

Horwath Mok & Poon<br />

Firm No: AF 0995<br />

Public Accountants<br />

Last day and time for the lodging of the Form of Proxy : 1 May 2001 at 10.30 a.m.<br />

Date and time of Extraordinary General Meeting : 3 May 2001 at 10.30 a.m.<br />

This Circular is dated 17 April 2001

DEFINITIONS<br />

Except where the context otherwise requires, the following definitions shall apply throughout this<br />

Circular:<br />

EGM : Extraordinary General Meeting<br />

EPS : Earnings per share<br />

GPIL : Golden Paradise International Limited<br />

HMP : Horwath Mok & Poon<br />

KLSE : Kuala Lumpur Stock Exchange<br />

MHB : Mitrajaya Holdings Berhad<br />

MHB Group : Mitrajaya Holdings Berhad and its subsidiary companies<br />

MSA : Mitrajaya SA (Pty) Ltd<br />

NTA : Net tangible assets<br />

Proposed GPIL Acquisition : Proposed purchase by GPIL of balance of 40% equity<br />

interest in Samitra comprising of 400 shares of Rand1.00<br />

each from Samrand for a cash consideration of<br />

Rand30,000,000 or its equivalent of RM15,372,000<br />

Proposed MSA Acquisition : Proposed purchase by MSA of two pieces of vacant<br />

freehold farmland property measuring 62.49 hectares<br />

located in the State City of Centurion, South Africa from<br />

Samrand for a cash consideration of Rand11,400,000 or its<br />

equivalent of RM5,841,360<br />

Proposed Acquisitions : Proposed GPIL Acquisition and Proposed MSA<br />

Acquisition<br />

RM and sen : Ringgit Malaysia and sen respectively<br />

Rand : South African Rand<br />

Samitra : Samrand Mitrajaya Development (Pty) Ltd<br />

Samrand : Samrand Development (Pty) Limited<br />

Conversion rate assumed in this Circular:-<br />

Rand 100: RM51.24 (The rate is taken from the Maybank Forex on 3 rd January 2001 which was the<br />

date that the Memorandum of Agreement was signed and later announced to the KLSE on 8 January<br />

2001)

CONTENTS<br />

PART A<br />

CIRCULAR TO THE SHAREHOLDERS OF MHB CONTAINING:<br />

SECTION PAGE<br />

1. INTRODUCTION 1<br />

2. DETAILS OF THE PROPOSED ACQUISITIONS 2<br />

3. INVESTMENT RISK CONSIDERATIONS 6<br />

4. INDUSTRY OVERVIEW AND FUTURE PROSPECTS 8<br />

5. FINANCIAL EFFECTS OF THE PROPOSED ACQUISITIONS 9<br />

6 CONDITIONS OF THE PROPOSED ACQUISITIONS 10<br />

7. DIRECTORS’ AND SUBSTANTIAL SHAREHOLDERS’ INTEREST 10<br />

8. INDEPENDENT ADVISER 10<br />

9. INDEPENDENT VALUATION 11<br />

10. EXTRAORDINARY GENERAL MEETING 11<br />

11. ADDITIONAL INFORMATION 11<br />

12. DIRECTORS’ RECOMMENDATION 11<br />

PART B<br />

INDEPENDENT ADVICE LETTER FROM HORWATH MOK & POON<br />

APPENDICES PAGE<br />

I INFORMATION ON MHB 22<br />

II INFORMATION ON SAMITRA 31<br />

III INFORMATION ON SAMRAND 46<br />

IV VALUER’S LETTER FROM HENRY BUTCHER, LIM & LONG SDN BHD 49<br />

V VALUER’S LETTER FROM MILLS FITCHET 52<br />

VI FURTHER INFORMATION 53<br />

NOTICE OF EXTRAORDINARY GENERAL MEETING<br />

FORM OF PROXY<br />

12<br />

58<br />

ENCLOSED

PART A<br />

Directors:-<br />

<strong>MITRAJAYA</strong> <strong>HOLDINGS</strong> <strong>BERHAD</strong><br />

Company No. 268257-T<br />

(Incorporated in Malaysia)<br />

Dato’ Samsudin bin Abu Hassan (Chairman)<br />

Tan Sri Dato’ Ir Jamilus bin Md Hussin (Executive Vice-Chairman)<br />

Tan Eng Piow (Managing Director)<br />

Foo Chek Lee (Executive Director)<br />

Roland Kenneth Selvanayagam (Executive Director)<br />

General (R) Dato’ Ismail bin Hassan (Independent Non–Executive Director)<br />

Low Mun Wai (Independent Non–Executive Director)<br />

To: The Shareholders of Mitrajaya Holdings Berhad<br />

Dear Sir/Madam<br />

THE PROPOSED ACQUISITIONS<br />

1. INTRODUCTION<br />

1<br />

Registered Office:-<br />

99, Jalan SS21/37<br />

Damansara Utama<br />

47400 Petaling Jaya<br />

Selangor Darul Ehsan<br />

17 April 2001<br />

1.1 On 19 January 2001, the Board of MHB announced the following:-<br />

i) GPIL, a wholly-owned subsidiary of MHB, had on 15 January 2001 entered<br />

into a Comprehensive Agreement with Samrand, MSA and Samitra to acquire<br />

from Samrand, 400 shares of Rand1.00 each representing 40% of the issued<br />

and paid-up share capital of Samitra for a cash consideration of<br />

Rand30,000,000 or approximately RM15,372,000. GPIL currently owns 60%<br />

equity interest in Samitra (“Proposed GPIL Acquisition”); and<br />

ii) MSA, a wholly-owned subsidiary of MHB, had entered into the<br />

abovementioned Comprehensive Agreement and further thereto, MSA had on<br />

15 January 2001 entered into a Deed of Sale with Samrand to acquire from<br />

Samrand two pieces of vacant freehold farmland property known as Portion<br />

251 and Portion 252 (a portion of Portion 2) of the farm<br />

OLIEVENHOUTBOSCH No. 389, Registration Division JR, Province of<br />

Gauteng in the State City of Centurion, South Africa for a total cash<br />

consideration of Rand11,400,000 or approximately RM5,841,360 (“Proposed<br />

MSA Acquisition”). Portion 2 of the farm OLIEVENHOUTBOSCH No. 389 is<br />

a master title for a total land area of 707.56 hectares. Portion 251 and<br />

Portion 252 has been subdivided out from this master title of Portion 2 and<br />

it is commonly described as “a portion of Portion 2”.

1.2 In view of the interest of Dato’ Samsudin bin Abu Hassan as mentioned in Section 7<br />

below, the Proposed Acquisitions are considered a related party transaction falling<br />

within the ambit of Chapter 20 of the Securities Commission’s Policies and<br />

Guidelines on Issue/Offer of Securities and Section 118 of the KLSE Listing<br />

Requirements. Accordingly, HMP has been appointed by the Independent Directors<br />

as the independent adviser to the Independent Directors and minority shareholders of<br />

MHB on the Proposed Acquisitions and an independent valuer has been appointed to<br />

provide an independent valuation on the development property of Samitra and the<br />

freehold property to be acquired from Samrand.<br />

1.3 The purpose of this Circular is to provide you with the details, rationale and financial<br />

effects of the Proposed Acquisitions and to seek your approval for the ordinary<br />

resolutions pertaining to the Proposed Acquisitions to be tabled at the forthcoming<br />

EGM to be convened at Dahlia Suite 1 & 2, 2nd Floor, East Wing, Petaling Jaya<br />

Hilton, No. 2, Jalan Barat, 46200 Petaling Jaya, Selangor Darul Ehsan on 3 May<br />

2001 at 10.30 am or any adjournment thereof.<br />

SHAREHOLDERS OF MHB ARE ADVISED TO READ THE CONTENTS OF BOTH<br />

PART A AND PART B OF THIS CIRCULAR CAREFULLY BEFORE VOTING ON<br />

THE ORDINARY RESOLUTIONS PERTAINING TO THE PROPOSED<br />

ACQUISITIONS<br />

2. DETAILS OF THE PROPOSED ACQUISITIONS<br />

2.1 Proposed Purchase by GPIL of balance of 40% equity interest in Samitra from<br />

Samrand ("Proposed GPIL Acquisition")<br />

On 15 January 2001, GPIL entered into a Comprehensive Agreement to acquire from<br />

Samrand, 400 shares of Rand1.00 each representing 40% of the issued and paid-up<br />

share capital of Samitra for a cash consideration of Rand30,000,000 or<br />

approximately RM15,372,000. The balance 600 shares of Rand1.00 each<br />

representing 60% of the issued and paid-up share capital of Samitra is currently held<br />

by GPIL. Following completion of this Proposed GPIL Acquisition, Samitra will<br />

become a wholly–owned subsidiary of GPIL.<br />

The Proposed GPIL Acquisition is not conditional on the Proposed MSA<br />

Acquisition.<br />

2.1.1 Information on Samitra<br />

Samitra was incorporated in South Africa as a private limited company on 11<br />

September 1998. Its present authorised share capital is Rand1,010 comprising of<br />

1,000 ordinary shares of Rand1.00 each of which 1,000 shares have been issued and<br />

fully paid and 1,000 redeemable preference shares of Rand0.01each of which 100<br />

redeemable preference shares have been issued and fully paid. The principal activity<br />

of Samitra is that of property development.<br />

The current development project of Samitra is the Samrand Golf and Country Estate<br />

located on several pieces of prime freehold land with a combined area of<br />

approximately 238 hectares located in the State City of Centurion, South Africa and<br />

just 20 minutes drive from the city of Johannesburg. The Samrand Golf and Country<br />

Estate is strategically located within a thriving commercial belt between<br />

Johannesburg and Pretoria.<br />

2

This prestigious mixed development consist of a residential golf estate with an 18hole<br />

Gary Player–designed international competition standard golf course,<br />

approximately 1,200 units of bungalow lots and 18-hole golf course and resort. The<br />

first 9-hole of the golf course has been playable since June 1999, whereas<br />

construction of the second 9-hole is completed and expected to be playable by April<br />

2001. The Samrand Golf and Country Estate was launched in mid-1999 and to-date<br />

has raked in sales value of Rand40,000,000 from up to-date sales of Residential 1<br />

Stands (bungalow lots). Construction of the golf course and infrastructure works is<br />

fully managed and undertaken by MSA. The remaining infrastructure works are<br />

expected to be complete by end of 2001.<br />

The Samrand Golf and Country Estate mixed development involves the sale of a total<br />

of approximately 672 Residential 1 Stands (bungalow lots). Sales of Phase 1<br />

involving 117 Residential 1 Stands was launched in June 1999 and it is fully sold.<br />

Subsequently, sales on Phase 2 involving 134 Stands was launched in June 2000 and<br />

68 Stands have been sold to-date representing 51% sales on Phase 2. Total sales from<br />

Phase 1 and Phase 2 achieved to-date is 185 Stands which constitutes 28% of total<br />

Residential 1 Stands available for sale. Phase 3 Sales consisting of 202 Residential 1<br />

Stands will be launched in 2001 / 2002 whereas balance of 216 Residential 1 Stands<br />

will be launched in Year 2002 / 2003. The development also involves sales on<br />

Residential 2 and 31 Business 4 Stands (business and office buildings lots) over the<br />

period from 2003 to 2005.<br />

Total sales revenue expected is approximately Rand351,900,000 against a total<br />

estimated development costs of Rand174,300,000 which cover all of the entire<br />

development i.e. Residential 1 and 2 and Business 4 Stands.<br />

Remaining infrastructure works expected to be completed by end 2001 are for the<br />

provision of internal civil infrastructure services to the remaining development<br />

covering roads, water supply, sewer, stormwater, telephone and electrical services.<br />

Total estimated cost is Rand20,000,000. The percentage of completion for the<br />

development to-date is 50%.<br />

2.1.2 Basis of determining the purchase consideration<br />

The purchase consideration of Rand30,000,000 for the Proposed GPIL Acquisition<br />

was negotiated on a willing buyer-willing seller basis after taking into consideration<br />

the potential earnings of Samitra. MHB has commissioned a local independent<br />

registered valuer, Henry Butcher, Lim and Long Sdn Bhd to carry out a valuation on<br />

the development property of Samitra. In their valuation report dated 28 February<br />

2000 enclosed in Appendix IV, Henry Butcher, Lim and Long Sdn Bhd have stated<br />

that the market value of the development property of Samitra to be Rand95,600,000<br />

comprising Rand2,400,000 for the 18-hole golf course and Rand93,200,000 for the<br />

unsold vacant stands on the Samrand Golf and Country Estate. Henry Butcher, Lim<br />

& Long Sdn Bhd have also valued the ten completed showhouses which have been<br />

sold off at Rand11,920,000. The value of the completed showhouses is not taken into<br />

consideration in MHB’s basis of determining the purchase consideration. Henry<br />

Butcher, Lim & Long Sdn Bhd have adopted the “Comparison Method” and<br />

“Discounted Cashflow Approach (known as Development Approach)” of valuation.<br />

40% of this valuation is Rand38,240,000.<br />

The initial investment in Samitra by Samrand was on 18 July 1999 and the original<br />

cost of investment was Rand10,920,437 and does not represent Samrand’s 40%<br />

interest in Samitra as Samrand only holds 400 shares in Samitra and had subscribed<br />

for the shares at Rand1.00 each.<br />

3

2.1.3 Terms of the Proposed GPIL Acquisition<br />

A sum of Rand1,000,000 has been paid by GPIL to Samrand upon execution of the<br />

Memorandum of Agreement. GPIL has paid Samrand another Rand1,800,000 on 31<br />

January 2001.<br />

Samrand is indebted to Samitra for the amount of Rand4,400,000 and as partial<br />

discharge of the purchase consideration, GPIL has paid Samrand’s debt of<br />

Rand4,400,000 directly to Samitra, on behalf of Samrand, on the date of the<br />

execution of the Comprehensive Agreement. The payment of this debt will then be<br />

set-off against the balance purchase price.<br />

The balance of Rand22,800,000 will be paid on completion, i.e. 30 April 2001 or at a<br />

later date as mutually agreed.<br />

There will be no liabilities to be assumed by GPIL or MHB other than the payment<br />

of the purchase consideration.<br />

2.1.4 Rationale for the Proposed GPIL Acquisition<br />

The Proposed GPIL Acquisition will increase MHB’s effective interest in Samitra<br />

from 60% to 100%. The Directors are of the opinion that the increase in the effective<br />

interest in Samitra will be beneficial to the Group for the following reasons:–<br />

(i) The Proposed GPIL Acquisition will enable MHB to procure full control of<br />

Samitra on the implementation of the development plans of the residential golf<br />

estate.<br />

(ii) The consolidation of interest in Samitra through the Proposed GPIL<br />

Acquisition will also accord the MHB Group with higher accretion of<br />

earnings.<br />

(iii) In addition to the enhancement of earnings and the profits being retained<br />

within the MHB Group, the cash resources from the Samitra project can<br />

also be utilised to fund other operations of the MHB Group in South Africa.<br />

(iv) Currently, the Samitra project is financed by the MHB Group through inter–<br />

company loans. It is therefore financially meaningful for MHB to acquire a<br />

higher stake in order to enjoy a larger share of the profits of the project.<br />

2.2 Proposed Purchase by MSA of two pieces of freehold property from Samrand<br />

("Proposed MSA Acquisition")<br />

On 15 January 2001, MSA entered into a Comprehensive Agreement together with a<br />

Deed of Sale with Samrand to acquire two pieces of freehold property known as<br />

Portion 251 and Portion 252 (a portion of Portion 2) of the farm<br />

OLIEVENHOUTBOSCH No. 389, Registration Division JR, Province of Gauteng in<br />

the State City of Centurion, South Africa ("the freehold property") for a total<br />

purchase consideration of Rand11,400,000 or approximately RM5,841,360 to be<br />

satisfied by cash payment. The freehold property covers approximately 62.49<br />

hectares farmland adjoining the western boundary of the prestigious Samrand Golf<br />

and Country Estate development. The freehold property will be acquired free from<br />

charges and encumbrances on a "as is where is" basis and with vacant possession.<br />

Portion 2 of the farm OLIEVENHOUTBOSCH No. 389 is a master title for a total<br />

land area of 707.56 hectares. Portion 251 and Portion 252 has been subdivided out<br />

from this master title of Portion 2 and it is commonly described as “a portion of<br />

Portion 2”.<br />

4

The Proposed MSA Acquisition will be conditional upon the conclusion of the<br />

Proposed GPIL Acquisition.<br />

2.2.1 Information on the freehold property<br />

The freehold property with an acreage of 62.49 hectares vacant farmland is adjoining<br />

the Samrand Golf and Country Estate currently developed by Samitra.<br />

The freehold property is enclosed within the Samrand Golf and Country Estate<br />

surrounded by an eight kilometres electrified security fencing which has been<br />

constructed at a cost of Rand4,000,000. The freehold property is overlooking and<br />

form part of the Samrand Golf and Country Estate. The development on this property<br />

is in the early stage of planning and total estimated development cost is<br />

Rand65,000,000.<br />

The development of this freehold property will be an extension of the existing<br />

Samrand Golf and Country Estate mixed development.<br />

It is proposed that the development of the freehold property together with the<br />

Samrand Golf and Country Estate be based on creating a high standard secured<br />

suburban in Johannesburg. Accordingly, based on preliminary plans, the proposed<br />

comprehensive mixed development would include approximately 400 bungalow lots<br />

with expected sales value of Rand141,050,000.<br />

2.2.2 Basis of determining the purchase consideration<br />

The purchase consideration of Rand11,400,000 works out the land cost to be<br />

Rand18.0 per square metre (psm) or approximately RM8.90 psm. The purchase<br />

consideration was arrived at on a willing buyer-willing seller basis after taking into<br />

account the development potential and strategic location of the freehold property and<br />

the current transacting price of neighbouring farmland which is going at about the<br />

same rate.<br />

A valuation was procured by MSA on the freehold property and was conducted by a<br />

South African property valuer, Mills Fitchet. The open market value of the freehold<br />

property according to the valuation report dated 31 December 2000 is<br />

Rand11,700,000.<br />

MHB also commissioned Henry Butcher, Lim & Long Sdn Bhd, an independent<br />

registered valuer to conduct a valuation on the freehold property and the latter’s<br />

report on 28 February 2001 as enclosed in Appendix IV indicates the same market<br />

value of Rand11,700,000. Henry Butcher, Lim & Long Sdn Bhd have adopted the<br />

“Comparison Method” and “Discounted Cashflow Approach (known as<br />

Development Approach)” of valuation.<br />

Samrand initially acquired the freehold property on 9 February 1996 and the original<br />

cost of investment to Samrand was Rand5,207,000.<br />

2.2.3 Terms of the Proposed MSA Acquisition<br />

A sum of Rand1,000,000 has been paid to Samrand upon execution of the<br />

Memorandum of Agreement. Another sum of Rand1,800,000 has been paid on 31<br />

January 2001.<br />

There is currently a bond registered in favour of ABSA Bank Ltd over the freehold<br />

property. As partial payment of the purchase consideration, MSA will pay<br />

Rand5,700,000 in favour of ABSA Bank Ltd for the release of the freehold property<br />

5

in the name of MSA to be registered in the Deeds office at Pretoria. This amount will<br />

then be set off against the balance of the purchase price for the freehold property.<br />

The balance of Rand2,900,000 payable on the purchase price will be paid by MSA to<br />

Samrand on the date of registration of the freehold property in the name of MSA.<br />

There will be no liabilities to be assumed by MSA or MHB other than the<br />

payment of the purchase consideration.<br />

2.2.4 Rationale for the Proposed MSA Acquisition<br />

The Proposed MSA Acquisition provides an opportunity for the MHB Group to have<br />

a relatively large piece of freehold land in Johannesburg with good potential for<br />

residential and commercial development. It enables the MHB Group to build up<br />

further, significantly, its land bank in a strategic location to ensure a substantial<br />

steady sourced income from its property development activities in South Africa<br />

in the long term.<br />

Tapping on the existing completed infrastructure of the adjoining development of the<br />

Samrand Golf and Country Estate would allow the development of the freehold<br />

property to progress much faster. In addition to this, the saleable area ratio would be<br />

higher as it can form part of the residential golf estate without having to alienate<br />

further land for public amenities and recreational facilities. The pricing of the<br />

products to be launched is also expected to be at higher rates taking into account the<br />

already proven and established Samrand Golf and Country Estate.<br />

3. INVESTMENT RISK CONSIDERATIONS<br />

Shareholders should carefully consider, in addition to other information contained herein, the<br />

following information (which may not be exhaustive) before voting on the Ordinary<br />

Resolutions pertaining to the Proposed Acquisitions:<br />

3.1 Political, Social and Economic Considerations<br />

The future growth and continued success of Samitra and MSA in South Africa are<br />

subject to risks that are linked to any developments in political, social and economic<br />

conditions where the MHB Group's current overseas operations are substantially in.<br />

Although it is notable that Samitra and MSA recorded profitability during the<br />

last two years, no assurance is given that any changes in the political, social and<br />

economic conditions in South Africa will not have any adverse impact on the<br />

property development business of Samitra and MSA.<br />

3.2 Business Risks<br />

The MHB Group’s investment in South Africa is subject to the risks inherent in<br />

property development industry. These include, inter alia, supply of labour and<br />

building materials, changes in labour and building materials costs, changes in<br />

general economic, business and credit conditions, demand for residential,<br />

commercial and industrial properties and changes in the legal and environmental<br />

framework within which this industry operates. These business risks implicit in<br />

all commercial activities and changes to these factors will definitely have<br />

implications to the Group’s operations. However, MHB being an established<br />

company with proactive management, is well positioned to successfully manage<br />

these business risks in the ever changing business environment.<br />

6

Furthermore, the MHB Group having been in operations in South Africa for the last<br />

two and a half years, has a better understanding of the business environment<br />

there and is able to adapt to any changes in which it operates.<br />

3.3 Competition<br />

The Samrand Golf and Country Estate is located in a strategic metropolitan area and<br />

the added feature of a golf course as part of the residential estate enhances the value<br />

of the properties in this area. At present, there are no keen competition from existing<br />

developer and contractor in this region. However, the potential of the property<br />

development and construction industry in this region may attract new players into the<br />

market. Nonetheless, Samitra and MSA are confident of its location as mentioned<br />

earlier and expect that its product launches will be well received. This is further<br />

augmented by the fact that the Samitra Golf and Country Estate is a fast maturing<br />

township and its development is way ahead of other developments in the vicinity.<br />

While the property development and construction industry are currently going<br />

through a period of rapid expansion, resulting in some price softening, these trends<br />

should not be detrimental to the industry. It is important to note that demand for<br />

residential and commercial units continues to grow.<br />

3.4 Foreign Exchange Risk<br />

As a significant part of the Samitra and MSA's business are conducted in a foreign<br />

currency, any fluctuation in relation to the Malaysian Ringgit will have an effect on<br />

the MHB Group's share of Samitra and MSA's results. No assurance is given that any<br />

change in the foreign currency exchange rates will not have an adverse effect on the<br />

MHB Group's share of Samitra and MSA's results.<br />

3.5 Dependence on Key Personnel<br />

The continued success of Samitra and MSA is highly dependent upon the<br />

abilities and continued efforts of its existing directors and senior management. The<br />

future success of Samitra and MSA will also depend upon their ability to attract and<br />

retain skilled personnel for their expansion programme.<br />

3.6 Forward-Looking Statements<br />

Certain statements in this announcement are forward-looking statements. Such<br />

forward-looking statements are not guarantees of future performance and involve<br />

known and unknown risks, uncertainties and other factors, which may cause the<br />

actual results, performance or achievements to differ materially from future results,<br />

performance or achievements expressed or implied in such forward-looking<br />

statements. Such factors include general economic and business conditions, changes<br />

in property development and construction industry competition and other factors.<br />

3.7 Policies on foreign investments and repatriation of profits in South Africa<br />

(i) Policies on foreign investment<br />

There are no restrictions on foreign investments in companies incorporated in<br />

South Africa. All capital introduced into South Africa may be repatriated at any<br />

time.<br />

(ii) Policies on repatriation of profits<br />

There are no restrictions in South Africa on the payment of dividends or profits<br />

after applicable tax deductions are made.<br />

7

4. INDUSTRY OVERVIEW AND FUTURE PROSPECTS<br />

The Republic of South Africa has the strongest economy in Africa. Approximately 75% of<br />

South Africa’s economic activity takes place in its four primary metropolitan areas, which<br />

together represent about 3% of the total land area of the country. These metropolitan areas<br />

are Gauteng, surrounding Johannesburg; the Durban-Pinetown area in KwaZulu-Natal; the<br />

Cape Peninsula; and the Port Elizabeth-Uitenhage area in the Eastern Cape. Gauteng, where<br />

most of South Africa’s gold mines are situated, is the financial and industrial centre of the<br />

country and accounts for 37% of all economic activity. Construction is one of the essential<br />

industries in South Africa.<br />

(Source:Doing Business In South Africa by Ernst & Young International, Ltd<br />

dated September 2000)<br />

As quoted by ABSA Bank on the review for the third quarter 2000, despite various<br />

macroeconomic factors that negatively influenced the position of the consumers in the third<br />

quarter of 2000, house prices have still increased strongly for year 2000 as compared to<br />

1999. The average price of a house came to some Rand272,000 in the third quarter of year<br />

2000. This represents a year-on-year increase of 19.1% in nominal terms and 11.8% in real<br />

terms. These are the biggest price increases since the first half of 1998, just before the effect<br />

of the Asian financial crisis hit South Africa.<br />

It is expected that inflation rate will move upwards in 2001, mainly due to the result of the<br />

impact of the notably weaker exchange rate compared with the beginning of year 2000,<br />

higher fuel prices, as well as an increase in domestic demand, which will lead to a higher<br />

growth in credit extension. Consistent with the increase in inflation rate, the lending rates<br />

will rise further in the second quarter of 2001 in view of the economic prospects. Taking into<br />

account the already strong price increases in the first three quarters of 2000, it is<br />

foreseen that house prices will increase by approximately 16.0% in nominal terms and by<br />

about 10.0% in real terms this year as a whole.<br />

(Source:ABSA Bank Ltd Quarterly Housing Review: Third Quarter 2000<br />

dated 25 October 2000)<br />

Montagu Property Group, Africa’s foremost marketer of residential townships and golf<br />

course estates, which is currently marketing 6 security developments across Gauteng which<br />

includes Samrand Golf and Country Estate, expressed that the current market in residential<br />

property is the strongest for the past 10 years.<br />

Montagu Property Group has achieved 200 sales at the Samrand Golf and Country Estate<br />

since the launch. As purchasers are often reluctant to purchase in a development in its<br />

infancy stage, Samitra’s initial success can be attributed to the wonderful location of the<br />

project, halfway between the 2 major cities on the reef, Johannesburg and Pretoria.<br />

In the next three to five years, the residential sector of the property market will perform the<br />

best of the entire property spectrum, a view expressed by the Head of Standard Bank<br />

Properties.<br />

(Source: Residential Property Market Report from Montagu Property Group)<br />

8

5. FINANCIAL EFFECTS OF THE PROPOSED ACQUISITIONS<br />

The financial effects of the Proposed Acquisitions on MHB are as follows:–<br />

5.1 Share Capital<br />

There will be no effect on the issued and paid-up capital of MHB as the Proposed<br />

Acquisitions will be satisfied wholly by cash and does not involve the issuance of<br />

MHB shares.<br />

5.2 Shareholding Structure<br />

As the Proposed Acquisitions will be on a cash basis, it will not have any effect on<br />

MHB’s shareholding structure.<br />

5.3 Earnings<br />

5.4 NTA<br />

The Proposed Acquisitions will have no immediate effect on earnings but are<br />

expected to contribute positively to the earnings of MHB Group in future.<br />

The effect of the Proposed Acquisitions on the NTA of MHB Group is as follows:-<br />

RM’000<br />

Audited NTA of MHB Group at 31 December 2000 125,680<br />

Estimated goodwill arising on acquisition of the remaining<br />

40% equity interest in Samitra (14,569)<br />

Adjusted NTA of MHB Group 111,111<br />

Before Proposed<br />

Share Acquisition<br />

in Samitra<br />

9<br />

After Proposed<br />

Share Acquisition<br />

in Samitra<br />

RM’000 RM’000<br />

Share Capital 94,874 94,874<br />

Reserves 30,806 30,806<br />

Shareholders’ Funds 125,680 125,680<br />

Less: Intangible Assets - (14,569)<br />

NTA 125,680 111,111<br />

NTA per share (sen) 132.47 117.11

5.5 Gearing<br />

As the Proposed Acquisitions will be on a cash basis and will be fully funded by<br />

internally generated fund, it is not expected to have any effect on MHB’s gearing<br />

position.<br />

6. CONDITIONS OF THE PROPOSED ACQUISITIONS<br />

The Proposed Acquisitions is conditional upon the following approvals:<br />

(i) the shareholders of MHB at an EGM to be convened;<br />

(ii) the shareholders of Samrand; and<br />

(iii) the approval of any other relevant authorities.<br />

7. DIRECTORS’ AND SUBSTANTIAL SHAREHOLDERS’ INTEREST<br />

Dato' Samsudin bin Abu Hassan, being a Non-Executive Chairman and a substantial<br />

shareholder of MHB is deemed to be interested in the Proposed Acquisitions by virtue of him<br />

being also a Director and a major shareholder of Samrand. Consequently, Dato' Samsudin bin<br />

Abu Hassan and persons connected to him will abstain from deliberation at Board Meetings<br />

and voting on the Proposed Acquisitions at the EGM to be convened.<br />

NRB Holdings Limited and SMG Holdings Limited are also substantial shareholder of MHB<br />

and are connected to Dato’ Samsudin bin Abu Hassan and will abstain from voting on the<br />

proposed Acquisitions at the EGM to be convened.<br />

Number of MHB shares held as at 19.03.2001<br />

Direct % Indirect %<br />

Dato’ Samsudin bin Abu Hassan – - 22,400,000 (Note1) 18.89<br />

SMG Holdings Limited – - 22,400,000 (Note2) 18.89<br />

NRB Holdings Limited – - 22,400,000 (Note3) 18.89<br />

Note 1 Interest by virtue of substantial interest in SMG Holdings Limited.<br />

Note 2 Deemed substantial Interest in NRB Holdings Limited. SMG Holdings Limited is listed on the<br />

Johannesburg Stock Exchange.<br />

Note 3 Held via OSK Nominees (Asing) Sdn Bhd.<br />

Dato’ Samsudin bin Abu Hassan, NRB Holdings Limited and SMG Holdings Limited have<br />

given their undertaking that they shall ensure that the persons connected with him/them will<br />

abstain from voting on the resolutions relating to the proposed Acquisitions.<br />

Save as disclosed, none of the other Directors, substantial shareholders or persons connected<br />

with the Directors or substantial shareholders of MHB have interest in the above Proposed<br />

Acquisitions.<br />

8. INDEPENDENT ADVISER<br />

Your Independent Directors have appointed HMP as Independent Adviser to advise the<br />

Independent Directors and minority shareholders on the Proposed Acquisitions. The<br />

Independent Advice of HMP on the Proposed Acquisitions is set out in Part B of this<br />

Circular.<br />

10

SHAREHOLDERS ARE ADVISED TO READ PART A AND PART B OF THIS<br />

CIRCULAR BEFORE TAKING ANY ACTION.<br />

9. INDEPENDENT VALUATION<br />

In view of the interest of the director and substantial shareholders as mentioned in Section 7<br />

above, an independent valuer has been appointed to provide an independent valuation on the<br />

landed properties of Samitra and the freehold property to be acquired by MSA.<br />

A copy of the valuer’s letter by Henry Butcher, Lim & Long Sdn Bhd is enclosed in<br />

Appendix IV of this Circular.<br />

10. EXTRAORDINARY GENERAL MEETING<br />

An EGM, the notice of which is set out in this Circular, will be held at Dahlia Suite 1 & 2,<br />

2nd Floor, East Wing, Petaling Jaya Hilton, No. 2, Jalan Barat, 46200 Petaling Jaya, Selangor<br />

Darul Ehsan on 3 May 2001 at 10.30 a.m. or any adjournment thereof, for the purpose of<br />

considering and if thought fit, passing the Ordinary Resolutions to give effect to the Proposed<br />

Acquisitions.<br />

If you are unable to attend and vote in person at the EGM, you should complete and<br />

return the enclosed Form of Proxy in accordance with the instructions therein as soon as<br />

possible and in any event so as to arrive at the Registered Office of the Company at 99,<br />

Jalan SS21/37, Damansara Utama, 47400 Petaling Jaya, Selangor Darul Ehsan not later than<br />

48 hours before the time-set for holding the EGM. The lodging of the Form of Proxy will<br />

not, however, preclude you from attending and voting in person at the EGM should you<br />

subsequently wish to do so.<br />

11. ADDITIONAL INFORMATION<br />

Shareholders are requested to refer to the attached appendices for additional information.<br />

12. DIRECTORS’ RECOMMENDATION<br />

Your Directors, after careful deliberations on the Proposed Acquisitions, are of the opinion<br />

that the terms of the Proposed Acquisitions are fair and reasonable and that the Proposed<br />

Acquisitions are in the best interest of the Company.<br />

Accordingly, your Directors, save for Dato’ Samsudin bin Abu Hassan who is deemed<br />

interested in the Proposed Acquisitions, recommend that you vote in favour of the Ordinary<br />

Resolutions pertaining to the Proposed Acquisitions to be tabled at the forthcoming EGM to<br />

give effect to the Proposed Acquisitions.<br />

Yours faithfully<br />

For and on behalf of the Board of Directors of<br />

<strong>MITRAJAYA</strong> <strong>HOLDINGS</strong> <strong>BERHAD</strong><br />

GENERAL (R) DATO’ ISMAIL BIN HASSAN<br />

Independent Director<br />

11

PART B<br />

To: The Shareholders of Mitrajaya Holdings Berhad<br />

Dear Sirs/Mesdames<br />

12<br />

17 April 2001<br />

INDEPENDENT ADVICE TO THE SHAREHOLDERS IN CONNECTION WITH<br />

THE PROPOSED GPIL ACQUISITION AND THE PROPOSED MSA<br />

ACQUISITION<br />

1. INTRODUCTION<br />

HORWATH MOK & POON<br />

Public Accountants<br />

A member of Horwath International<br />

Level 16 Tower C<br />

Megan Phileo Avenue<br />

12 Jalan Yap Kwan Seng<br />

50450 Kuala Lumpur<br />

Tel (603) 2166 0000<br />

Fax (603) 2166 9200<br />

E mail horwath@po.jaring.my<br />

Website http://www.horwath.com/himy.htm<br />

1.1 On 15 January 2001, GPIL, a wholly-owned subsidiary company of MHB, had<br />

entered into a Comprehensive Agreement with Samrand, MSA and Samitra to<br />

acquire 400 shares of Rand1.00 each representing 40% of the issued and paid-up<br />

capital of Samitra for a cash consideration of Rand30,000,000 or approximately<br />

RM15,372,000 from Samrand. GPIL currently holds 60% equity interest in<br />

Samitra.<br />

On the same date, MSA, a wholly-owned subsidiary company of MHB and a party<br />

to the above mentioned Comprehensive Agreement, had entered into a Deed of<br />

Sale with Samrand to acquire two pieces of freehold property for a cash<br />

consideration of Rand11,400,000 or approximately RM5,841,360.<br />

1.2 In view of certain directors’ and substantial shareholders’ interests as described in<br />

Section 1.2 of the Company’s Circular to Shareholders, the Independent Directors<br />

of MHB have appointed Horwath Mok & Poon (“HMP”) as the Independent<br />

Adviser to the Shareholders of MHB in relation to the Proposed Acquisitions as<br />

set out in Section 1.1 above.<br />

HMP had, via our letter dated 8 March 2001, confirmed to the KLSE our<br />

eligibility to act as Independent Adviser to the Shareholders of MHB.

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

1.3 The purpose of this Independent Advice Letter (“IAL”) is to provide the<br />

shareholders of MHB with an independent evaluation, from the financial point of<br />

view, of the terms and conditions of the Proposed Acquisitions, and HMP’s<br />

recommendation thereon.<br />

2. DETAILS OF THE PROPOSED ACQUISITIONS<br />

2.1 Details of the Proposed GPIL Acquisition<br />

Samitra is a property development company incorporated in South Africa with an<br />

authorised share capital of Rand1,010 comprising 1,000 ordinary shares of<br />

Rand1.00 each and 1,000 redeemable preference shares of Rand0.01 each, all of<br />

which have been issued and fully paid.<br />

The purchase consideration Rand30,000,000 has been arrived at on a willing<br />

buyer-willing seller basis after taking into consideration the potential earnings of<br />

Samitra. Upon execution of the Memorandum of Agreement, GPIL has paid<br />

Samrand Rand1,000,000 and another Rand1,800,000 on 31 January 2001. On the<br />

date of execution of the Comprehensive Agreement, GPIL has paid to Samitra an<br />

amount of Rand4,400,000 as partial discharge of the amount owing by Samrand to<br />

Samitra. This amount will be set-off against the balance of the purchase<br />

consideration. The balance of Rand22,800,000 will be paid on completion.<br />

Based on the audited financial statements of Samitra for the financial year ended<br />

31 December 2000, the financial position of Samitra is as follows:-<br />

Balance Sheet at 31 December 2000<br />

13<br />

Audited as at<br />

31 December 2000 Translated*<br />

Rand’000 RM’000<br />

FIXED ASSETS 28 14<br />

INVESTMENT 720 369<br />

CURRENT ASSETS 89,870 46,050<br />

CURRENT LIABILITIES (42,921) (21,993)<br />

Net Current Assets 46,949 24,057<br />

47,697 24,440

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

Balance Sheet at 31 December 2000 (Cont’d)<br />

FINANCED BY:-<br />

14<br />

Audited as at<br />

31 December 2000 Translated*<br />

Rand’000 RM’000<br />

SHARE CAPITAL 15,250 7,815<br />

RETAINED PROFITS 3,917 2,007<br />

Shareholders’ Equity 19,167 9,822<br />

LONG TERM LIABILITY<br />

Shareholder’s Loan 28,530 14,618<br />

47,697 24,440<br />

Source: Audited financial statements of Samitra for the financial year ended 31 December<br />

2000<br />

* - Translated based on Rand100 to RM51.24, the quoted selling rate on 3 January 2001<br />

(the date of execution of the Memorandum of Agreement).<br />

The current development project undertaken by Samitra comprises the Samrand<br />

Golf and Country Estate which resides on several pieces of freehold land with a<br />

combined area of approximately 238 hectares located in the State City of<br />

Centurion, South Africa. Further description of the development project is set out<br />

in Section 2.1.1 of Part A of the Circular to Shareholders.<br />

Further information on Samitra are set out in Appendix II of the Company’s<br />

Circular to Shareholders.<br />

2.2 Details of the Proposed MSA Acquisition<br />

The freehold property to be acquired constitutes 62.49 hectares of vacant farmland<br />

which adjoins the Samrand Golf and Country Estate currently developed by<br />

Samitra. The purchase consideration of Rand11,400,000 was arrived at on a<br />

willing buyer-willing seller basis after taking into account the potential<br />

development of the land, its strategic location and the current transacting price of<br />

neighbouring farmland.

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

3. CONDITIONS TO THE PROPOSED ACQUISITIONS<br />

The Proposed Acquisitions are subject to the following approvals:-<br />

(i) the shareholders of MHB at an EGM to be convened;<br />

(ii) the shareholders of Samrand; and<br />

(iii) the approval of any other relevant authorities.<br />

4. EVALUATION OF THE PROPOSED ACQUISITIONS<br />

HMP has been appointed by the Independent Directors of MHB to provide the<br />

shareholders of MHB with a fairness opinion, from a financial point of view, of<br />

the terms and conditions of the above mentioned Proposed Acquisitions. HMP<br />

was not involved in any negotiations on the terms and conditions of the Proposed<br />

Acquisitions.<br />

In rendering our opinion, we have reviewed the business and financial information on<br />

MHB and Samitra. We have discussed the said information with the senior<br />

management of MHB.<br />

In our review and analysis in formulating our opinion, we have relied upon the<br />

reasonableness, accuracy and completeness of the financial and other information<br />

on MHB and Samitra provided to us by MHB and also the valuation report on the<br />

landed properties of Samitra and the freehold property to be acquired by MSA by<br />

Henry Butcher, Lim & Long Sdn. Bhd dated 28 February 2001 (hereinafter<br />

referred to as the “Valuation Report”). We have further assumed that such<br />

information has been prepared in good faith and reflect the judgements and<br />

estimates of MHB’s management as of the date hereof and that the management<br />

of MHB are unaware of any facts that would make the financial information and<br />

other information provided to us incomplete, misleading or inaccurate. We have<br />

not assumed any responsibility for independent verification of, and express no<br />

opinion as to, any such information.<br />

Our opinion is necessarily based on the financial information prepared by MHB<br />

as set out in Appendix I and II of the Company’s Circular to Shareholders, and on<br />

the Valuation Report as enclosed in Appendix IV of the said Circular. Finally, we<br />

have assumed that the Proposed Acquisitions will be consummated based on the<br />

terms set forth in the Company’s Announcement to the KLSE without material<br />

modification.<br />

15

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

As Independent Adviser to the shareholders of MHB, our scope of evaluation in<br />

regard to the Proposed Acquisitions is confined only to the financial terms of the<br />

Proposed Acquisitions and the terms of settlement of the same, and not the merits<br />

or otherwise of the commercial decisions regarding the Proposed Acquisitions.<br />

In preparing this opinion, we have paid attention to those factors which we believe are<br />

of general importance to an assessment of the terms of the Proposed Acquisitions<br />

from a financial point of view and therefore of general concern to the general body of<br />

the shareholders. We are not in possession of information relating to, and have<br />

not given any consideration to, separate specific investment objectives, financial<br />

situation and particular needs of any individual shareholder or any group of<br />

shareholders. We recommend that any individual shareholder or any group of<br />

shareholders who may require advice in relation to the Proposed Subscription in<br />

the context of their individual objectives, financial situation and particular needs<br />

should consult their stockbroker, bank manager, solicitor, or professional adviser.<br />

In evaluating the Proposed Subscription and the terms of settlement, we have paid<br />

particular attention to the following issues relating to the financial terms and<br />

effects of the proposed consideration and the terms of settlement:-<br />

• The objective of the Proposed Acquisitions;<br />

• Whether the consideration for each of the Proposed Acquisitions are fair<br />

and reasonable; and<br />

• The financial effects of the Proposed Acquisitions to MHB.<br />

4.1 RATIONALE FOR THE PROPOSED ACQUISITIONS<br />

The rationale for the Proposed GPIL Acquisition and the Proposed MSA<br />

Acquisition as detailed in Sections 2.1.4 and 2.2.4, respectively of Part A of the<br />

Circular to Shareholders is to enable MHB to acquire full control over The<br />

Samrand Golf and Country Estate development (via the Proposed GPIL<br />

Acquisition) and to further capitalise on the aforesaid development through the<br />

acquisition of the freehold property (via the Proposed MSA Acquisition) which<br />

adjoins the development of the Samrand Golf and Country Estate. Synergies are<br />

expected to arise from the Proposed MSA Acquisition by way of increased<br />

saleable area of the freehold property as future developments on the said property<br />

can share common public amenities and recreational facilities which are already<br />

included in the current development.<br />

The Directors opine that the Samrand Golf and Country Estate and the freehold<br />

property are strategically located and would provide a stable source of income to<br />

be derived from residential and commercial development.<br />

16

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

4.2 BASIS OF THE CONSIDERATION FOR THE PROPOSED ACQUISITIONS<br />

We note that the consideration for the Proposed GPIL Acquisition has been<br />

arrived at taking into consideration the potential earnings of Samitra whilst the<br />

consideration for the Proposed MSA Acquisition has been arrived at taking into<br />

account the current transacting price of neighbouring farmland.<br />

In respect of the acquisition of Samitra, we have evaluated the reasonableness of<br />

the consideration for the Proposed Acquisitions based on the Realisable Net Asset<br />

Value (“RNAV”) with principal reliance on the Valuation Report in our<br />

evaluation of the consideration for the Proposed GPIL Acquisition, as the<br />

principal basis of evaluation.<br />

In respect of the Proposed MSA Acquisition, we have relied solely on the<br />

Valuation Report.<br />

In view that Samitra is a development company with significant land bank, we are<br />

of the opinion that the most appropriate basis of evaluating the reasonableness of<br />

the consideration is by applying the RNAV model. In conjunction with our<br />

evaluation, we have also reviewed the basis of valuation used in the Valuation<br />

Report.<br />

Due consideration has also been given to the qualitative aspects of the Proposed<br />

Acquisitions.<br />

4.2.1 Realisable Net Asset Value Model<br />

As Samitra is a development company, the most appropriate method of valuation<br />

to be considered is the Realisable Net Asset Value (“RNAV”) model. This model<br />

involves estimating the revaluation reserve on the landed properties of Samitra<br />

and then imputing the estimated revaluation reserve on the NTA of the company<br />

to arrive at the RNAV. In applying the RNAV model we have principally relied<br />

on the Valuation Report.<br />

The market value of the landed properties of Samitra (including the freehold<br />

property to be acquired pursuant to the Proposed MSA Acquisition as extracted<br />

from the Valuation Report) is set out below:-<br />

Table A<br />

Rand’000<br />

Ten (10) completed show-houses, separately registered on<br />

freehold stands<br />

11,920<br />

Completed 18-hole Gary Player designed golf course 2,400<br />

Portion 251 (48.253 ha) & 252 (14.23 ha) 11,700<br />

Total value of unsold vacant land as per cash flow 93,200<br />

Grand total 119,220<br />

Source : Valuation Report prepared by Henry Butcher, Lim & Long Sdn. Bhd. dated 28<br />

February 2001.<br />

17

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

Valuation of 40% equity interest to be acquired pursuant to the Proposed GPIL<br />

Acquisition<br />

The estimation of the revaluation reserve on landed properties of Samitra is<br />

derived as follows:-<br />

Reference Rand’000<br />

Ten (10) completed show-houses, separately<br />

registered on freehold stands (Note 1)<br />

Completed 18-hole Gary Player designed golf<br />

Table A<br />

N/A<br />

course<br />

Table A<br />

2,400<br />

Total value of unsold vacant land as per cash flow Table A 93,200<br />

Total estimated value of land I 95,600<br />

Land cost as at 8 February 2001 (Note 2) II 2,877<br />

Estimated gross revaluation reserve III = I – II 92,723<br />

Less : Deferred tax on revaluation reserve at 30%* IV = III x 30% 27,817<br />

Estimated net revaluation reserve<br />

Profit on sale of ten (10) completed [after tax]<br />

V = III - IV 64,906<br />

(Note1)<br />

Adjusted Audited NTA of Samitra at 31 December<br />

VI<br />

1,260<br />

2000 (Note 3)<br />

VII<br />

3,917<br />

RNAV of Samitra VIII = V + VI +VII 70,083<br />

Equity interest to be acquired at 40% VIII x 40% 28,033<br />

* Corporate tax rate of South Africa. The deferred tax has been provided for as the properties are<br />

expected to be sold in the foreseeable future.<br />

Note 1 : The ten (10) completed show-houses, separately registered on freehold stands have been<br />

excluded from the estimation of the revaluation reserve because, as represented by the<br />

management of Samitra, the ten (10) show-houses have been disposed of to a related<br />

company subsequent to the financial year end but before 8 February 2001 (the material<br />

date of valuation). The effect of the ten (10) completed show-houses on the valuation of<br />

Samitra is to the extent of profit recognised on sale of the same. The profit recognised on<br />

sale (after tax), based on the management accounts of Samitra for the financial period up<br />

to 8 February 2001, is approximately Rand1,260,000.<br />

Note 2 : The land cost as at 8 February 2001 is provided by the management of Samitra and based<br />

on representation by the same, the land cost for the 18-hole Gary Player designed golf<br />

course and the unsold vacant land has not been subject to any material change up to the<br />

date of the Valuation Report of 28 February 2001 (the material date of valuation of which<br />

was 8 February 2001).<br />

Note 3 : The Adjusted Audited NTA has been arrived at by deducting the Preference Share and<br />

the attributable Share Premium Reserve arising from the issue of preference share of<br />

Rand1 and Rand15,249,549 respectively, from the audited NTA of Samitra as the<br />

preference share was issued solely to GPIL, and hence the attributable Share Premium<br />

Reserve is not distributable to the minority shareholder.<br />

18

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

Based on the above analysis, the value of 40% equity interest in Samitra is<br />

estimated at Rand28,033,000 (about RM14,364,000). Hence, the consideration<br />

for the Proposed GPIL Acquisition of Rand30,000,000 (about RM15,372,000)<br />

represents a slight “premium” of approximately 7.0% over the RNAV of Samitra.<br />

Valuation of the freehold property to be acquired pursuant to the Proposed<br />

MSA Acquisition<br />

The above mentioned freehold property to be acquired has been included in the<br />

Valuation report and has been estimated at Rand11,700,000 (refer to Table A –<br />

Portions 251 & 252).<br />

4.2.2 Qualitative Aspects<br />

. In assessing the reasonableness of the consideration of the Proposed Acquisitions,<br />

due consideration should also be given to MHB Group’s business intentions in<br />

undertaking the Proposed Acquisitions.<br />

The Proposed GPIL Acquisition will render MHB Group full control of Samitra<br />

particularly in the aspects of implementation of development plans. Full control<br />

of Samitra would also lead to increased earnings to MHB Group. Further, the<br />

robust cash flows expected from the development project would strengthen<br />

the overall cash flow position of the Group.<br />

In view of the fact that the development project undertaken by Samitra is currently<br />

funded by the MHB Group, the acquisition of the remaining 40% equity interest<br />

by MHB would effectively retain the inter-company funds within the MHB<br />

Group.<br />

The Proposed MSA Acquisition would create synergies to MHB Group’s<br />

operations in South Africa mainly due to the reason that the freehold property,<br />

which comprises 62.49 hectares of vacant farmland adjoins the Samrand Golf and<br />

Country Estate currently being developed by Samitra. It is therefore reasonable to<br />

anticipate cost savings from the future commercial development of the freehold<br />

property as some infrastructure and public facilities which are already part of the<br />

current development project can be shared by future development projects on the<br />

freehold property to be acquired.<br />

Although the Proposed Acquisitions would be transacted in foreign currency<br />

(namely the South African Rand), the exposure of MHB Group to foreign<br />

exchange fluctuations in this respect is mitigated as the investments are based in<br />

South Africa and the business and returns from the investments would be<br />

denominated in the same foreign currency, hence creating a form of natural hedge<br />

on the investment.<br />

19

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

4.3 FINANCIAL EFFECTS OF THE PROPOSED ACQUISITIONS<br />

We have considered the financial effects of the Proposed Acquisitions on the<br />

share capital, earnings and NTA of MHB Group as follows:-<br />

4.3.1 Share Capital<br />

The Proposed Acquisitions will not have any effect on the issued and paid-up<br />

share capital of MHB.<br />

4.3.2 Earnings<br />

4.3.3 NTA<br />

The Proposed Acquisitions will have no immediate effect on earnings but are<br />

expected to contribute positively to the earnings of MHB Group in future.<br />

The effect of the Proposed Acquisitions on the NTA of MHB Group is as<br />

follows:-<br />

20<br />

RM’000<br />

Audited NTA of MHB Group at 31 December 2000 125,680<br />

Estimated goodwill arising on acquisition of the remaining<br />

40% equity interest Samitra (14,569)<br />

Adjusted NTA of MHB Group 111,111<br />

The Proposed Acquisitions are expected to contribute positively to the NTA of<br />

MHB Group in future.<br />

5. DIRECTORS’ AND SUBSTANTIAL SHAREHOLDERS’ INTERESTS<br />

Based on the register of shareholders and directors of Samrand as at 15 February<br />

2001, Dato’ Samsudin bin Abu Hassan is a major shareholder and director. Dato’<br />

Samsudin bin Abu Hassan also holds, via his substantial shareholdings in NRB<br />

Holdings Limited and SMG Holdings Limited, 22,400,000 ordinary shares in<br />

MHB representing 18.89% equity interest in the same.<br />

Accordingly, Dato’ Samsudin bin Abu Hassan and persons connected to him will<br />

abstain from deliberation at Board Meetings and voting on the Proposed<br />

Acquisitions and, NRB Holdings Limited and SMG Holdings Limited will abstain<br />

from voting on the Proposed Acquisitions at the EGM to be convened.<br />

Save as disclosed above, none of the other directors and/or substantial<br />

shareholders MHB and persons connected to them have any interest, direct or<br />

indirect, in the Proposed Acquisitions.

Independent Advice Letter to the Shareholders<br />

of Mitrajaya Holdings Berhad<br />

6. OTHER INFORMATION<br />

Other information relevant to our IAL are included as Appendices herewith.<br />

7. CONCLUSION AND RECOMMENDATION<br />

The matter in consideration by the shareholders of MHB which is the subject of<br />

this IAL is whether they should vote in favour of the Proposed Acquisitions.<br />

Our opinion, is formed principally based on the reasonableness of the<br />

consideration for the Proposed GPIL Acquisition and the Proposed MSA<br />

Acquisition. Based on our evaluation of the consideration for the Proposed GPIL<br />

Acquisition set out in Section 4.2.1 and 4.2.2 above, we noted that<br />

notwithstanding the slight premium of 7.0% payable over the minority interest in<br />

the RNAV of Samitra, the consideration for the Proposed GPIL Acquisition is not<br />

unreasonable based on the expected cash flows from the realisation of the<br />

development properties. The slight premium is also justifiable as MHB Group,<br />

after the Proposed GPIL Acquisition, would procure full control over the<br />

operations of Samitra. In respect of the Proposed MSA Acquisition, the<br />

consideration of Rand11,400,000 (RM5,841,360) closely approximates the market<br />

value reported in the Valuation Report of Rand11,700,000 (about RM5,995,000).<br />

We have also evaluated the reasonableness of the consideration for the Proposed<br />

Acquisitions giving due consideration to the qualitative aspects as detailed in<br />

Section 4.2.2 above and are of the opinion, that the qualitative benefits are<br />

realisable.<br />

On the assumption that MHB’s strategy for the acquisition is consummated, there<br />

would be potential for robust growth in results and cash flows of MHB Group.<br />

After taking into consideration the various factors discussed above, we are of the opinion<br />

that, on the basis of the information available to us, the financial terms of the<br />

Proposed Acquisitions are fair and reasonable and are not detrimental to the<br />

minority shareholders of MHB and we recommend that you vote in favour of the<br />

resolutions pertaining to the Proposed Acquisitions to be tabled at the forthcoming<br />

EGM.<br />

Yours faithfully<br />

HORWATH MOK & POON<br />

ONN KIEN HOE<br />

Partner<br />

21

INFORMATION ON MHB<br />

1. History and Business<br />

22<br />

APPENDIX I<br />

MHB was incorporated in Malaysia on 28 June 1993 under the Companies Act, 1965, as a private<br />

limited company under the name of Persmurni Sdn Bhd with an issued and paid-up share capital<br />

of RM2.00 comprising two (2) ordinary shares of RM1.00 each. It changed its name to<br />

Persmurni Berhad on 6 November 1993 upon its conversion to a public company. The Company<br />

subsequently changed its name to Mitrajaya Holdings Berhad on 19 November 1993.<br />

MHB was listed on the Second Board of KLSE on 8 December 1994 and subsequently<br />

transferred to the Main Board of the KLSE on 29 May 1998.<br />

MHB is principally an investment holding company. The MHB Group is involved in investment<br />

holding, civil engineering and construction works, sales of construction materials, property<br />

development, manufacturing and selling of premix products, manufacturing and selling of readymix<br />

concrete and renting of plant and machinery.<br />

2. Share Capital<br />

The present authorised share capital of MHB is RM500,000,000 comprising 500,000,000<br />

ordinary shares of RM1.00 each. As at 19 March 2001, the issued and paid-up share capital of<br />

MHB is RM118,592,903 comprising 118,592,903 ordinary shares of RM1.00 each.<br />

Date of<br />

Allotment<br />

No. of Ordinary<br />

Shares of<br />

RM1.00<br />

Each Allotted<br />

Consideration<br />

Cumulative<br />

Issued And<br />

Paid-Up Share<br />

Capital<br />

28.06.1993 2 Cash 2<br />

22.08.1994 18,099,642 Issued pursuant to the acquisition of<br />

Pembinaan Mitrajaya Sdn Bhd<br />

22.08.1994 323,648 Issued pursuant to the acquisition of<br />

Daya Asfalt Sdn Bhd<br />

26.11.1994 600,000 Issued pursuant to a public issue at an<br />

issue price of RM3.50 per share<br />

25.03.1998 15,218,634 Issued pursuant to a Bonus Issue on<br />

the basis of four (4) new ordinary<br />

shares for every five (5) existing<br />

ordinary shares of RM1.00 each<br />

29.05.1998 19,023,292 Issued pursuant to a Rights Issue at<br />

an issue price of RM1.18 per share on<br />

the basis of one (1) new ordinary<br />

share for every one (1) existing<br />

ordinary share of RM1.00 each held<br />

before the bonus issue<br />

11.11.1998<br />

to<br />

30.12.1998<br />

371,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

18,099,644<br />

18,423,292<br />

19,023,292<br />

34,241,926<br />

53,265,218<br />

53,636,218

Date of<br />

Allotment<br />

13.01.1999<br />

to<br />

08.06.1999<br />

No. of Ordinary<br />

Shares of<br />

RM1.00<br />

Each Allotted<br />

Consideration<br />

755,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

07.06.1999 200,000 Issued pursuant to the exercise of the<br />

Warrants1 at an exercise price of<br />

RM1.55 per share.<br />

18.06.1999 50,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

23.06.1999<br />

to<br />

25.06.1999<br />

02.07.1999<br />

to<br />

13.08.1999<br />

92,000 Issued Pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

172,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

17.08.1999 200 Issued pursuant to the exercise of the<br />

Warrants1 at an exercise price of<br />

RM1.55 per share.<br />

06.09.1999<br />

to<br />

13.09.1999<br />

15,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

07.10.1999 333 Issued pursuant to the exercise of the<br />

Warrants1 at an exercise price of<br />

RM1.55 per share.<br />

11.10.1999<br />

to<br />

25.02.2000<br />

256,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

03.03.2000 200 Issued pursuant to the exercise of the<br />

Warrants1 at an exercise price of<br />

RM1.55 per share.<br />

06.03.2000 168,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

14.03.2000 400,000 Issued pursuant Private Placement at<br />

an issue price of RM4.00 per share.<br />

15.03.2000<br />

to<br />

23.03.2000<br />

350,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

23<br />

Cumulative<br />

Issued And<br />

Paid-Up Share<br />

Capital<br />

54,391,218<br />

54,591,218<br />

54,641,218<br />

54,733,218<br />

54,905,218<br />

54,905,418<br />

54,920,418<br />

54,920,751<br />

55,176,751<br />

55,176,951<br />

55,344,951<br />

55,744,951<br />

56,094,951

Date of<br />

Allotment<br />

No. of Ordinary<br />

Shares of<br />

RM1.00<br />

Each Allotted<br />

Consideration<br />

27.03.2000 199,800 Issued pursuant to the exercise of the<br />

Warrants1 at an exercise price of<br />

RM1.55 per share.<br />

30.03.2000 102,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

31.03.2000 1,363,000 Issued pursuant to the Private<br />

Placement at an issue price of<br />

RM4.00 per share.<br />

05.04.2000 62,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

12.04.2000 150,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

02.05.2000 50,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

09.05.2000 44,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

24.05.2000 60,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

30.05.2000 25,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

05.06.2000 46,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

12.06.2000 28,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

26.06.2000 8,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

05.07.2000 12,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

24<br />

Cumulative<br />

Issued And<br />

Paid-Up Share<br />

Capital<br />

56,294,751<br />

56,396,751<br />

57,759,751<br />

57,821,751<br />

57,971,751<br />

58,021,751<br />

58,065,751<br />

58,125,751<br />

58,150,751<br />

58,196,751<br />

58,224,751<br />

58,232,751<br />

58,244,751

Date of<br />

Allotment<br />

No. of Ordinary<br />

Shares of<br />

RM1.00<br />

Each Allotted<br />

Consideration<br />

19.07.2000 224,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

07.08.2000 122,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

18.08.2000 205,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

29.08.2000 120,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

01.09.2000 1,500 Issued pursuant to the conversion of<br />

the Warrants1 into ordinary shares at<br />

an exercise price of RM1.55 per<br />

share.<br />

01.09.2000 47,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

14.09.2000 10,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

26.09.2000 12,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

29.09.2000 5,000 Issued pursuant to the conversion of<br />

the Warrants1 into ordinary shares at<br />

an exercise price of RM1.55 per<br />

share.<br />

20.10.2000 4,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

27.10.2000 6,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share.<br />

10.11.2000 7,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share<br />

15.11.2000 205,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share<br />

25<br />

Cumulative<br />

Issued And<br />

Paid-Up Share<br />

Capital<br />

58,468,751<br />

58,590,751<br />

58,795,751<br />

58,915,751<br />

58,917,251<br />

58,964,251<br />

58,974,251<br />

58,986,251<br />

58,991,251<br />

58,995,251<br />

59,001,251<br />

59,008,251<br />

59,213,251

Date of<br />

Allotment<br />

No. of Ordinary<br />

Shares of<br />

RM1.00<br />

Each Allotted<br />

Consideration<br />

17.11.2000 3,000 Issued pursuant to the exercise of the<br />

ESOS at an exercise price of RM1.21<br />

per share<br />

22.11.2000 1,000 Issued pursuant to the exercise of the<br />

Warrants1 at an exercise price of<br />

RM1.55 per share<br />

30.11.2000 79,200 Issued pursuant to the exercise of the<br />

Warrants1 at an exercise price of<br />

RM1.55 per share<br />

11.12.2000 35,577,871 Issued pursuant to a Bonus Issue on<br />

the basis of three (3) new ordinary<br />

shares for every five (5) existing<br />

ordinary shares of RM1.00 each<br />

13.02.2001 23,718,581 Issued pursuant to a Rights Issue at<br />

an issue price of RM1.30 per share on<br />

the basis of two (2) new ordinary<br />

shares for every five (5) existing<br />

ordinary shares of RM1.00 each held<br />

before Bonus Issue<br />

3. Substantial Shareholders<br />

26<br />

Cumulative<br />

Issued And<br />

Paid-Up Share<br />

Capital<br />

59,216,251<br />

59,217,251<br />

59,296,451<br />

94,874,322<br />

118,592,903<br />

The substantial shareholders (holding 2% or more of the issued and paid-up capital of MHB)<br />

according to the Register of Substantial Shareholders and Record of Depositors as at 19 March<br />

2001 are as follows:-<br />

No. of Shares<br />

Held Direct<br />

%<br />

No. of Shares held<br />

Indirect<br />

Tan Eng Piow 5,018,060 4.23 *32,780,000 27.64<br />

NRB Holdings Limited - - **22,400,000 18.89<br />

SMG Holdings Limited - - #22,400,000 18.89<br />

Dato’ Samsudin bin Abu<br />

Hassan<br />

- - @22,400,000 18.89<br />

Ong Teck Chong 4,029,785 3.40 @@6,346,633 5.35<br />

* Held via the pledged securities account as follows:<br />

No. of ordinary shares<br />

1. Arab-Malaysian Finance Berhad 9,580,000<br />