Slides - IEA

Slides - IEA

Slides - IEA

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

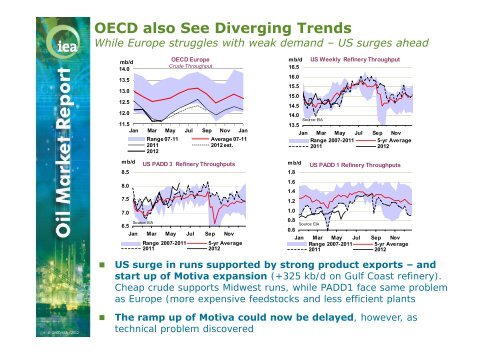

OECD also See Diverging Trends<br />

While Europe struggles with weak demand – US surges ahead<br />

mb/d<br />

14.0<br />

13.5<br />

13.0<br />

12.5<br />

12.0<br />

OECD Europe<br />

Crude Throughput<br />

11.5<br />

Jan Mar May Jul Sep Nov Jan<br />

mb/d<br />

8.5<br />

8.0<br />

7.5<br />

7.0<br />

6.5<br />

Range 07-11 Average 07-11<br />

2011 2012 est.<br />

2012<br />

US PADD 3 Refinery Throughputs<br />

Source: EIA<br />

Jan Mar May Jul Sep Nov<br />

Range 2007-2011 5-yr Average<br />

2011 2012<br />

mb/d US Weekly Refinery Throughput<br />

16.5<br />

16.0<br />

15.5<br />

15.0<br />

14.5<br />

14.0<br />

Source: EIA<br />

13.5<br />

Jan Mar May Jul Sep Nov<br />

Range 2007-2011 5-yr Average<br />

2011 2012<br />

mb/d<br />

US PADD 1 Refinery Throughputs<br />

1.8<br />

1.6<br />

1.4<br />

1.2<br />

1.0<br />

0.8<br />

0.6<br />

Source: EIA<br />

Jan Mar May Jul Sep Nov<br />

Range 2007-2011 5-yr Average<br />

2011 2012<br />

• US surge in runs supported by strong product exports – and<br />

start up of Motiva expansion (+325 kb/d on Gulf Coast refinery).<br />

Cheap crude supports Midwest runs, while PADD1 face same problem<br />

as Europe (more expensive feedstocks and less efficient plants<br />

© OECD/<strong>IEA</strong> - 2012<br />

• The ramp up of Motiva could now be delayed, however, as<br />

technical problem discovered