here. - Koskie Minsky LLP

here. - Koskie Minsky LLP

here. - Koskie Minsky LLP

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

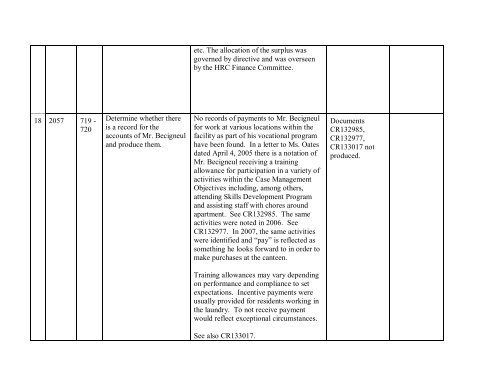

etc. The allocation of the surplus was<br />

governed by directive and was overseen<br />

by the HRC Finance Committee.<br />

18 2057 719 -<br />

720<br />

Determine whether t<strong>here</strong><br />

is a record for the<br />

accounts of Mr. Becigneul<br />

and produce them.<br />

No records of payments to Mr. Becigneul<br />

for work at various locations within the<br />

facility as part of his vocational program<br />

have been found. In a letter to Ms. Oates<br />

dated April 4, 2005 t<strong>here</strong> is a notation of<br />

Mr. Becigneul receiving a training<br />

allowance for participation in a variety of<br />

activities within the Case Management<br />

Objectives including, among others,<br />

attending Skills Development Program<br />

and assisting staff with chores around<br />

apartment. See CR132985. The same<br />

activities were noted in 2006. See<br />

CR132977. In 2007, the same activities<br />

were identified and “pay”is reflected as<br />

something he looks forward to in order to<br />

make purchases at the canteen.<br />

Documents<br />

CR132985,<br />

CR132977,<br />

CR133017 not<br />

produced.<br />

Training allowances may vary depending<br />

on performance and compliance to set<br />

expectations. Incentive payments were<br />

usually provided for residents working in<br />

the laundry. To not receive payment<br />

would reflect exceptional circumstances.<br />

See also CR133017.