Service Department Cost Allocation - Anna Lee

Service Department Cost Allocation - Anna Lee

Service Department Cost Allocation - Anna Lee

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

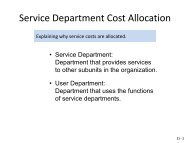

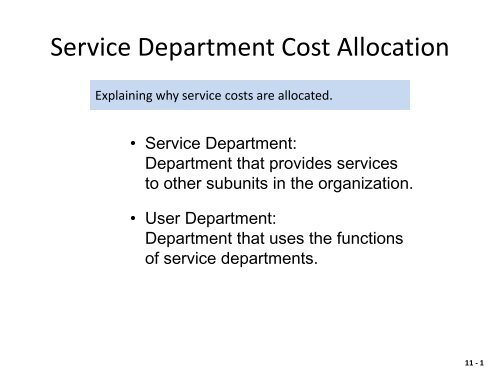

<strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> <strong>Allocation</strong><br />

Explaining why service costs are allocated.<br />

• <strong>Service</strong> <strong>Department</strong>:<br />

<strong>Department</strong> that provides services<br />

to other subunits in the organization.<br />

• User <strong>Department</strong>:<br />

<strong>Department</strong> that uses the functions<br />

of service departments.<br />

11 - 1

LO1<br />

<strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> <strong>Allocation</strong><br />

• Intermediate cost center:<br />

<strong>Cost</strong> center whose costs are charged<br />

to other departments in the organization.<br />

• Final cost center:<br />

<strong>Cost</strong> center, such as a production or<br />

marketing department, whose costs<br />

are not allocated to another cost center.<br />

11 - 2

LO1<br />

<strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> <strong>Allocation</strong><br />

<strong>Service</strong> and User <strong>Department</strong>s – Carlyle Coal Company<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Information Systems<br />

(S1)<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Administration<br />

(S2)<br />

User <strong>Department</strong>:<br />

Hilltop Mine<br />

(P1)<br />

User <strong>Department</strong>:<br />

Pacific Mine<br />

(P2)<br />

11 - 3

LO1<br />

<strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> <strong>Allocation</strong><br />

Basic Data for <strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> Association<br />

Carlyle Coal Company<br />

Information<br />

Systems (S1) a<br />

<strong>Service</strong> <strong>Department</strong><br />

Administration<br />

(S2) b<br />

<strong>Department</strong>s:<br />

Administration (S2)<br />

Information Systems (S1)<br />

Hilltop Mine (P1)<br />

Pacific Mine (P2)<br />

Total (to be distributed)<br />

hours<br />

100,000<br />

-0-<br />

20,000<br />

80,000<br />

200,000<br />

50%<br />

0<br />

10<br />

40<br />

100%<br />

employees)<br />

-0-<br />

2,000<br />

5,000<br />

3,000<br />

10,000<br />

0%<br />

20<br />

50<br />

30<br />

100%<br />

a<br />

<strong>Allocation</strong> base for S1: Computer hours; <strong>Cost</strong> to be allocated: $800,000<br />

b<br />

<strong>Allocation</strong> base for S2: Number of employees; <strong>Cost</strong> to be allocated: $5,000,000<br />

11 - 4

<strong>Cost</strong> <strong>Allocation</strong>: Direct Method<br />

• Direct method:<br />

Charges costs of service departments to user departments<br />

without making allocations among service departments.<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Information Systems<br />

(S1)<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Administration<br />

(S2)<br />

User <strong>Department</strong>:<br />

Hilltop Mine<br />

(P1)<br />

User <strong>Department</strong>:<br />

Pacific Mine<br />

(P2)<br />

11 - 5

LO2<br />

<strong>Cost</strong> <strong>Allocation</strong>: Direct Method<br />

<strong>Service</strong> <strong>Department</strong><br />

<strong>Cost</strong> <strong>Allocation</strong><br />

Direct<br />

<strong>Cost</strong><br />

Hilltop Mine<br />

(P1)<br />

Percent Applicable to<br />

Pacific Mine<br />

(P2)<br />

Total<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Information Systems (S1)<br />

Administration (S2)<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Information Systems (S1)<br />

Administration (S2)<br />

Total allocated<br />

$ 800,000<br />

5,000,000<br />

Direct<br />

<strong>Cost</strong><br />

$ 800,000<br />

5,000,000<br />

$5,800,000<br />

Note: Under this method, S1 costs doesn’t allocate to S2.<br />

20.0% a<br />

62.5% b<br />

Hilltop Mine<br />

(P1)<br />

$ 160,000 c<br />

3,125,000 d<br />

$3,285,000<br />

a<br />

20.0% = 20,000 hours ÷ (20,000 hours + 80,000 hours)<br />

b<br />

62.5% = 5,000 employees ÷ (5,000 employees + 3,000 employees)<br />

c<br />

$160,000 = 20% × $800,000<br />

d<br />

$3,125,000 = 62.5% × $5,000,000<br />

80.0%<br />

37.5%<br />

Amount Applicable to<br />

Pacific Mine<br />

(P2)<br />

$ 640,000<br />

1,875,000<br />

$2,515,000<br />

100.0%<br />

100.0%<br />

Total<br />

$ 800,000<br />

5,000,000<br />

$5,800,000<br />

11 - 6

<strong>Cost</strong> <strong>Allocation</strong>: Step Method<br />

• The step method allocates some service<br />

department costs to other service departments.<br />

• Once an allocation is made from a service<br />

department no further allocations are made<br />

back to that service department.<br />

• Generally, allocate in order of proportion of<br />

services provided to other service departments.<br />

11 - 7

LO3<br />

<strong>Cost</strong> <strong>Allocation</strong>: Step Method<br />

<strong>Cost</strong> Flow Diagram: Step Method – Carlyle Coal Company<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Information Systems<br />

(S1)<br />

Computerhours<br />

User <strong>Department</strong>:<br />

Hilltop Mine<br />

(P1)<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Administration<br />

(S2)<br />

Employees<br />

User <strong>Department</strong>:<br />

Pacific Mine<br />

(P2)<br />

11 - 8

LO3<br />

<strong>Cost</strong> <strong>Allocation</strong>: Step Method<br />

<strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> <strong>Allocation</strong><br />

Direct<br />

<strong>Cost</strong><br />

(S1)<br />

Percent Applicable to<br />

(S2)<br />

(P1)<br />

(P2)<br />

Total<br />

<strong>Service</strong> Dept.:<br />

(S1)<br />

(S2)<br />

$ 800,000<br />

5,000,000<br />

0.0%<br />

0.0%<br />

50.0% a<br />

0.0%<br />

10.0% b<br />

62.5% d<br />

40.0% c<br />

37.5% e<br />

100.0%<br />

100.0%<br />

a<br />

50.0% = 100,000 hours ÷ (100,000 hours + 20,000 hours + 80,000 hours)<br />

b<br />

10.0% = 20,000 hours ÷ (100,000 hours + 20,000 hours + 80,000 hours)<br />

c<br />

40.0% = 80,000 hours ÷ (100,000 hours + 20,000 hours + 80,000 hours<br />

d<br />

62.5% = 5,000 employees ÷ (5,000 employees + 3,000 employees)<br />

e<br />

37.5% = 3,000 employees ÷ (5,000 employees + 3,000 employees)<br />

11 - 9

LO3<br />

<strong>Cost</strong> <strong>Allocation</strong>: Step Method<br />

<strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> <strong>Allocation</strong><br />

To<br />

From<br />

(S1)<br />

(S2)<br />

(P1)<br />

(P2)<br />

Total<br />

Dept. costs<br />

(S1)<br />

(S2)<br />

$800,000<br />

(800,000)<br />

-0-<br />

$ -0-<br />

$5,000,000<br />

400,000 f<br />

(5,400,000)<br />

$ -0-<br />

Note: Under Step method, S1 costs does allocate to S2<br />

.<br />

f<br />

50.0% × $800,000<br />

g<br />

10.0% × $800,000<br />

h<br />

40.0% × $800,000<br />

I<br />

62.5% × $5,400,000<br />

j<br />

37.5% × $5,400,000<br />

k<br />

$5,800,000 of service department costs were<br />

ultimately allocated to production departments.<br />

$ -0-<br />

80,000 g<br />

3,375,000 i<br />

$3,455,000<br />

$ -0-<br />

320,000 h<br />

2,025,000 j<br />

$2,345,000<br />

$5,800,000 k<br />

$5,800,000 k<br />

11 - 10

<strong>Cost</strong> <strong>Allocation</strong>: Reciprocal Method<br />

• The reciprocal method recognizes all services<br />

provided by any service department, including<br />

services provided to other service departments.<br />

• It accounts for cost flows among service<br />

departments providing services to each other.<br />

• It requires a simultaneous equation solution.<br />

11 - 11

LO4<br />

<strong>Cost</strong> <strong>Allocation</strong>: Reciprocal Method<br />

<strong>Cost</strong> Flow Diagram: Reciprocal Method – Carlyle Coal Company<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Information Systems<br />

(S1)<br />

Computerhours<br />

User <strong>Department</strong>:<br />

Hilltop Mine<br />

(P1)<br />

<strong>Service</strong> <strong>Department</strong>:<br />

Administration<br />

(S2)<br />

Employees<br />

User <strong>Department</strong>:<br />

Pacific Mine<br />

(P2)<br />

11 - 12

LO4<br />

<strong>Cost</strong> <strong>Allocation</strong>: Reciprocal Method<br />

1. Write the costs of each service department<br />

in equation form.<br />

Total <strong>Service</strong><br />

<strong>Department</strong> costs<br />

Direct costs of the<br />

= +<br />

<strong>Service</strong> <strong>Department</strong><br />

<strong>Cost</strong>s allocated to the<br />

<strong>Service</strong> <strong>Department</strong><br />

2. Solve equations simultaneously using<br />

matrix algebra.<br />

11 - 13

LO4<br />

<strong>Cost</strong> <strong>Allocation</strong>: Reciprocal Method<br />

Total <strong>Service</strong><br />

<strong>Department</strong> costs<br />

Direct cost of the<br />

= +<br />

<strong>Service</strong> <strong>Department</strong><br />

<strong>Cost</strong>s allocated to the<br />

<strong>Service</strong> <strong>Department</strong><br />

S1 = $ 800,000 + 0.20 S2<br />

S2 = $5,000,000 + 0.50 S1<br />

Substituting the first equation into the second yields:<br />

S2 = $5,000,000 + 0.50($800,000 + 0.20 S2)<br />

S2 = $5,000,000 + $400,000 + 0.10 S2<br />

0.9 S2 = $5,400,000 S2 = $6,000,000<br />

Substituting the value of S2 back into the first equation gives:<br />

S1 = $800,000 + 0.20($6,000,000)<br />

S1 = $2,000,000<br />

11 - 14

LO4<br />

<strong>Cost</strong> <strong>Allocation</strong>: Reciprocal Method<br />

<strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> <strong>Allocation</strong><br />

Total<br />

<strong>Cost</strong><br />

(S1)<br />

Percent Applicable to<br />

(S2)<br />

(P1)<br />

(P2)<br />

Total<br />

<strong>Service</strong> Dept.:<br />

(S1)<br />

(S2)<br />

$2,000,000<br />

6,000,000<br />

0.0%<br />

20.0% d<br />

50.0% a<br />

0.0%<br />

10.0% b<br />

50.0% e<br />

40.0% c<br />

30.0% f<br />

100.0%<br />

100.0%<br />

a<br />

50.0% = 100,000 hours ÷ (100,000 hours + 20,000 hours + 80,000 hours)<br />

b<br />

10.0% = 20,000 hours ÷ (100,000 hours + 20,000 hours + 80,000 hours)<br />

c<br />

40.0% = 80,000 hours ÷ (100,000 hours + 20,000 hours + 80,000 hours<br />

d<br />

20.0% = 2,000 employees ÷ (2,000 employees + 5,000 employees + 3,000 employees)<br />

e<br />

50.0% = 5,000 employees ÷ (2,000 employees + 5,000 employees + 3,000 employees)<br />

f<br />

30.0% = 3,000 employees ÷ (2,000 employees + 5,000 employees + 3,000 employees<br />

11 - 15

LO4<br />

<strong>Cost</strong> <strong>Allocation</strong>: Reciprocal Method<br />

<strong>Service</strong> <strong>Department</strong> <strong>Cost</strong> <strong>Allocation</strong><br />

To<br />

From<br />

(S1)<br />

(S2)<br />

(P1)<br />

(P2)<br />

Total<br />

Direct costs<br />

(S1)<br />

(S2)<br />

$ 800,000<br />

(2,000,000) a<br />

1,200,000 e<br />

$ -0-<br />

$5,000,000<br />

1,000,000 b<br />

(6,000,000) f<br />

$ -0-<br />

$ -0-<br />

200,000 c<br />

3,000,000 g<br />

$3,200,000<br />

$ -0-<br />

800,000 d<br />

1,800,000 h<br />

$2,600,000<br />

$5,800,000 i<br />

$5,800,000 i<br />

a<br />

Total costs of S1<br />

b<br />

<strong>Cost</strong>s allocated from S1 (50% × $2,000,000)<br />

c<br />

10.0% × $2,000,000<br />

d<br />

40.0% × $2,000,000<br />

e<br />

<strong>Cost</strong>s allocated from S2 (20% × $6,000,000)<br />

f<br />

Total costs of S2<br />

g<br />

50% × $6,000,000<br />

h<br />

30% × $6,000,000<br />

I<br />

$5,800,000 of service department costs were ultimately<br />

allocated to production departments.<br />

11 - 16

LO4<br />

<strong>Cost</strong> <strong>Allocation</strong>: Reciprocal Method<br />

Comparison of Direct, Step, and Reciprocal Methods<br />

Method Hilltop Mine Pacific Mine Total<br />

Direct<br />

Step<br />

Reciprocal<br />

$3,285,000<br />

3,455,000<br />

3,200,000<br />

$2,515,000<br />

2,345,000<br />

2,600,000<br />

$5,800,000<br />

5,800,000<br />

5,800,000<br />

11 - 17

The Reciprocal Method<br />

and Decision Making<br />

L.O. 5 Use the reciprocal method for decisions.<br />

• Suppose that the variable cost in Information <strong>Service</strong>s (S1)<br />

is $200,000 (out of the total of $800,000) and the variable<br />

cost in Administration (S2) is $3,500,000 (out of $5,000,000).<br />

• Let's repeat the reciprocal cost analysis substituting<br />

the variable costs from the total costs.<br />

11 - 18

LO5<br />

The Reciprocal Method<br />

and Decision Making<br />

Total <strong>Service</strong><br />

<strong>Department</strong> costs<br />

Direct cost of the<br />

= +<br />

<strong>Service</strong> <strong>Department</strong><br />

<strong>Cost</strong>s allocated to the<br />

<strong>Service</strong> <strong>Department</strong><br />

S1 = $ 200,000 + 0.20 S2<br />

S2 = $3,500,000 + 0.50 S1<br />

Substituting the first equation into the second yields:<br />

S2 = $3,500,000 + 0.50($200,000 + 0.20 S2)<br />

S2 = $3,500,000 + $100,000 + 0.10 S2<br />

0.9 S2 = $3,600,000 S2 = $4,000,000<br />

Substituting the value of S2 back into the first equation gives:<br />

S1 = $200,000 + 0.20($4,000,000)<br />

S1 = $1,000,000<br />

11 - 19

The Reciprocal Method<br />

and Decision Making<br />

• The total variable cost of Information <strong>Service</strong>s, when you<br />

consider the use of Administration by Information <strong>Service</strong>s<br />

is $1,000,000.<br />

• The total cost savings that would come from eliminating<br />

Information <strong>Service</strong>s are the $1,000,000 variable costs<br />

plus any avoidable fixed costs.<br />

11 - 20

<strong>Allocation</strong> of Joint <strong>Cost</strong>s<br />

Joint cost is the cost of a manufacturing process with two or more<br />

outputs produced together up to a split-off point.<br />

Split-off<br />

point<br />

Hi-grade coal: 15,000 units<br />

Sales value: $300,000<br />

Mining costs<br />

$270,000<br />

(Joint <strong>Cost</strong>s)<br />

Lo-grade coal: 30,000 units<br />

Sales value: $450,000<br />

(Separable <strong>Cost</strong>s)<br />

11 - 21

<strong>Allocation</strong> of Joint <strong>Cost</strong>s<br />

2 Methods of <strong>Allocation</strong>:<br />

Net realizable value method<br />

Physical quantities method<br />

• Net realizable value method:<br />

Joint cost allocation based on the proportional<br />

values of the products at the split-off point.<br />

• Net realizable value (NRV):<br />

Sales value of each product at the split-off point.<br />

• Estimated net realizable value:<br />

If the sales value at split-off is not available, use the<br />

estimated NRV method. That is sales price of a final product<br />

minus additional processing costs necessary to prepare<br />

a product for sale.<br />

11 - 22

Net Realizable Value Method<br />

Final sales value<br />

Less: Additional processing costs<br />

Net realizable value at split-off point<br />

Proportionate share:<br />

= $300,000 ÷ $750,000<br />

= $450,000 ÷ $750,000<br />

Allocated joint costs:<br />

= $270,000 × 40%<br />

= $270,000 × 60%<br />

Example<br />

Carlyle Coal Company<br />

Joint <strong>Allocation</strong> – NRV Method<br />

(no additional processing costs)<br />

Hi-Grade Lo-Grade Total<br />

$300,000<br />

-0-<br />

$300,000<br />

40%<br />

$108,000<br />

$450,000<br />

-0-<br />

$450,000<br />

60%<br />

$162,000<br />

$750,000<br />

-0-<br />

$750,000<br />

11 - 23

Net Realizable Value Method<br />

Carlyle Coal Company<br />

For the Month of March<br />

Sales value<br />

Less: Allocated joint costs<br />

Gross margin<br />

Gross margin as a percent of sales<br />

Hi-Grade Lo-Grade Total<br />

$300,000<br />

108,000<br />

$192,000<br />

64%<br />

$450,000<br />

162,000<br />

$288,000<br />

64%<br />

$750,000<br />

270,000<br />

$480,000<br />

64%<br />

11 - 24

Estimating NRV<br />

• When no sales value exists for outputs at the split-off point,<br />

the estimated NRV should be determined.<br />

Further Processing of Coal:<br />

<strong>Cost</strong> Flows –<br />

Carlyle Coal Company<br />

Split-off<br />

point<br />

Hi-grade coal: 15,000 units<br />

Sales value: $300,000<br />

Mining costs<br />

$270,000<br />

Lo- to Mid-grade coal:<br />

30,000 units<br />

$50,000 processing cost<br />

Sales value: $550,000<br />

11 - 25

Estimating NRV<br />

Carlyle Coal Company<br />

For the Month of March<br />

Sales value<br />

Less: Additional cost to process<br />

Estimated NRV at split-off<br />

<strong>Allocation</strong> of joint costs<br />

Gross margin<br />

Gross margin as a percent of sales<br />

Hi-Grade Mid-Grade Total<br />

$300,000 $550,000<br />

to mid-grade — coal 50,000<br />

$300,000 $500,000<br />

101,250 a —<br />

— 168,750 b<br />

$198,750 $331,250<br />

66% 60%<br />

$850,000<br />

50,000<br />

$800,000<br />

101,250<br />

168,750<br />

$530,000<br />

62%<br />

a<br />

($300,000 ÷ $800,000) × $270,000<br />

b<br />

($500,000 ÷ $800,000) × $270,000<br />

11 - 26

Physical Quantities Method<br />

• Joint cost allocation is based on measurement of<br />

the volume, weight, or other physical measure of<br />

the joint products at the split-off point.<br />

When to use:<br />

1. Output product prices are volatile.<br />

2. Significant processing occurs between the<br />

split-off point and the first point of marketability.<br />

3. Product prices are not set by the market.<br />

11 - 27

Physical Quantities Method<br />

Carlyle Coal Company<br />

For the Month of March<br />

Quantity (tons)<br />

Sales value<br />

<strong>Allocation</strong> of joint costs<br />

Gross margin<br />

Gross margin as a percent of sales<br />

Hi-Grade Lo-Grade Total<br />

15,000<br />

$300,000<br />

90,000 a<br />

$210,000<br />

70%<br />

30,000<br />

$450,000<br />

180,000 b<br />

$270,000<br />

60%<br />

45,000<br />

$750,000<br />

270,000<br />

$480,000<br />

64%<br />

a<br />

(15,000 tons ÷ 45,000 tons) × $270,000<br />

b<br />

(30,000 tons ÷ 45,000 tons) × $270,000<br />

11 - 28

By-products<br />

• By-products are outputs of joint production processes<br />

that are relatively minor in quantity or value. Joint costs<br />

are usually not allocated to a by-product, instead,<br />

market value of by-product is reported as follows:<br />

• Method 1:<br />

The net realizable value from sale of the by-products<br />

is deducted from the joint costs (as a contra production<br />

cost) before allocation to the main products.<br />

• Method 2:<br />

The proceeds from sale of the by-product are treated<br />

as other revenue (other income).<br />

11 - 29

By-products – Method 1<br />

Carlyle Coal Company<br />

For the Month of March<br />

Hi-Grade<br />

Lo-Grade<br />

Dust<br />

by-product<br />

Total<br />

Sales value<br />

Less: Additional processing costs<br />

Net realizable value at split-off point<br />

Deduct: Sales value of by-product a<br />

Allocated remaining joint costs a<br />

Gross margin<br />

Gross margin as a percent of sales<br />

$300,000<br />

-0-<br />

$300,000<br />

-0-<br />

102,000 b<br />

$198,000<br />

66%<br />

$450,000<br />

-0-<br />

$450,000<br />

-0-<br />

153,000 c<br />

$297,000<br />

66%<br />

$15,000<br />

-0-<br />

$15,000<br />

15,000<br />

-0-<br />

-0-<br />

0%<br />

$765,000<br />

-0-<br />

$765,000<br />

15,000<br />

255,000<br />

$495,000<br />

65%<br />

a Note: Joint costs adjusted for sales value of by-product (dust) (765,000 – 15,000 = 750,000)<br />

b<br />

($300,000 ÷ $750,000) or 40% × ($270,000 Joint cost – $15,000)<br />

c<br />

($450,000 ÷ $750,000) or 60% × ($270,000 – $15,000)<br />

11 - 30

Carlyle Coal Company<br />

For the Month of March<br />

Quantity (tons)<br />

Sales value<br />

<strong>Allocation</strong> of joint costs<br />

Gross margin<br />

Gross margin as a percent of sales<br />

15,000<br />

$300,000<br />

108,000<br />

$192,000<br />

64%<br />

30,000<br />

$450,000<br />

162,000<br />

$288,000<br />

64%<br />

45,000<br />

$750,000<br />

270,000<br />

$480,000<br />

64%<br />

(300,000÷ 750,000) = 40% 270,000 x 40% = 108,000<br />

(450,000÷ 750,000) = 60% 270,000 x 60% = 162,000

By-products – Method 2<br />

Carlyle Coal Company<br />

For the Month of March<br />

Hi-Grade<br />

Lo-Grade<br />

Dust<br />

Total<br />

Sales value<br />

Less: Additional processing costs<br />

Net realizable value at split-off point<br />

Allocated joint costs a<br />

Gross margin<br />

Gross margin as a percent of sales<br />

$300,000<br />

-0-<br />

$300,000<br />

108,000 b<br />

$192,000<br />

64%<br />

$450,000<br />

-0-<br />

$450,000<br />

162,000 c<br />

$288,000<br />

64%<br />

$15,000<br />

-0-<br />

$15,000<br />

-0-<br />

$15,000<br />

100%<br />

$765,000<br />

-0-<br />

$765,000<br />

270,000<br />

$495,000<br />

65%<br />

a<br />

Joint costs adjusted for sales value of by-product (dust)<br />

b<br />

($300,000 ÷ $750,000) or 40% × $270,000 joint cost = 108,000. 15,000 is not deducted<br />

from joint cost, instead, it is reported as other income.<br />

c<br />

($450,000 ÷ $750,000) or 60% × $270,000 = 162,000<br />

11 - 32

Sell or Process Further<br />

• Suppose CCC can sell Lo-grade coal for $450,000<br />

at the split-off point or process it further to make<br />

mid-grade coal.<br />

• Mid-grade coal would sell for $550,000 and<br />

additional processing costs would be $50,000.<br />

Additional revenue: $100,000<br />

?<br />

Additional cost: $ 50,000<br />

11 - 33

Sell or Process Further<br />

Differential Analysis<br />

Carlyle Coal Company<br />

Sell<br />

Lo-Grade<br />

Coal<br />

Process<br />

Further<br />

(Mid-Grade)<br />

Differential<br />

Revenue/<br />

<strong>Cost</strong>s<br />

Revenues<br />

Less: Separate processing costs<br />

Margin<br />

$450,000<br />

-0-<br />

$450,000<br />

$550,000<br />

50,000<br />

$500,000<br />

$100,000<br />

50,000<br />

$ 50,000<br />

Net gain from<br />

processing<br />

further<br />

11 - 34