had no free liquid funds at their disposal in 1973, in- creased their share frorn 19% (DM 3.5 bn.) to 51% (DM 14.5 bn.). By contrast, non-bank customers' share of to- tal purchases of fixed-interest paper fell frorn rouyhly 81% (DM 15.3 bn.) in 1973 to only 48% (DM 13.8 bn.) in 1974. Investment funds: more returns than purchases The drawn-out depression on the share markets also affected the sales perforrnance of German investment cornpanies. Not until the last few weeks of the year were good sales results achieved again, hand in hand with the general recovery. For the first time, Gerrnan public funds had to take back more certificates than they sold. Whilst there had been an inflow of rnonies totalling DM 1.8 bn. in 1973, 1974 closed with a net outflow of DM 133 m. However, the performance of individual groups of funds varied from this overall developrnent. Share-holding funds as a whole recorded a net inflow of monies, albeit sharply reduced, with internationally operating share- holdirig funds faririg worse than funds holding mainly German securities. Fixed-interest security funds suffered an unexpectedly sharp set-back. The outflow of rnonies totalling DM 359 m. was due primarily to returns frorn abroad. The fund cornpanies tried to switch their low-interest bearing ti- tles into high-interest bearing ones. In the case of real property investment funds, sales al- most balanced out returns. Weak Euroloan market In 1974, issuing activity in the market for long-terrn Eu- roloans came to a complete standstill on several occa- sions. Taken in total, not even 50% of the previous year's volume was achieved. Investors reacted to the in- tensified inflationary trends throughout the world with great reticence towards longer-term loans, whilst poten- tial issuers hesitated in view of the high interest rates since a good number of alternative possibilities were available on the Eurocredit markets. Not until interest rates began to fall in November did demand pick up again on the Eurocapital market in the expectation that interest rates would continue to fall, whereby the inter- est of buyers - bearing in mind the strength of the D- Mark on the foreign exchange rnarkets - was directed particularly towards international DM-loans. Until November, on the other hand, with one exception, no foreign DM-loans werc issued. When the market re- covered quickly at the beginning of 1975, it was gradual- ly possible to lead investors back to maturities of up to 10 years. This developrnent, supported to a certain ex- tent by OPEC purchases, is gratifying above all because it inakes it possible again to secure for numerous invest- ments throughout the world, healthier financing and more closely matching rnaturities, than are available on the Eurocredit markets via the predominant roll-over procedure. The total value of new loans was equivalent to roughly US-$ 2.4 bn., cornpared with a corresponding figure of roughly US-$ 5 bn. in 1973 and US-$6.5 bn. in the record year of 1972. Dollar titles with 35% of total issues and DM-loans with 23% had smaller Shares than in the pre- vious year, whilst the share of loans denominated in Swiss Francs was unchanged at roughly 15%. The share of Guil<strong>der</strong>-loans increased to 13%. The share of loans denominated in units of account (UA) also rose. The srnall number of convertible loans (3), cornpared with previous years, can be cxplained by the general fall in prices on the international share rnarkets. However, statistics for the Eurocapital market are no longer all that informative because they do not include larger-sized private placements - mainly denominated in US-$ - placed en bloc by individual issuing banks in the OPEC countries. In isolated cases, Arab currencies were also used for such issues. lnterest rates reached a new high on the Eurocapital market in the Course of 1974. In autumn, the issue yield on 5 to 7-year foreign DM-loans stood at 10% or more; towards the year-end, it fell to about 93/4% and then, by February, to about 9% for first-class borrowers. In the secondary market for outstanding Euroloans with longer maturities, buyers were able to earn even higher yields. Eurodollar business Comes to its senses - better judgement prevails In the first few months of 1974, developments on the Eurocredit rnarket were distinctly stormy. They were de- terrnined to a large extent by the investment-seeking ex-

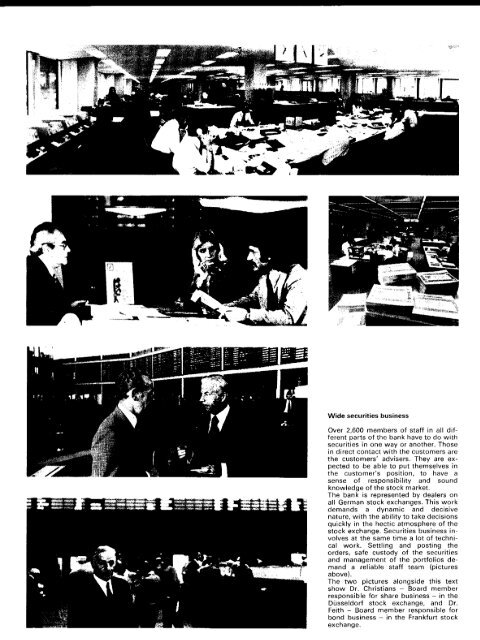

Wide securities business Over 2,600 members of staff in all dif- ferent parts of thc bank have to do with securities in one way or another. Those in direct contact with the ciistomers are the customers' advisers. They are ex- pected to be able to put themselves in the customer's position, to have a sense of responsibility and sourid knowledue of the stock market

- Page 1 and 2: Report for the Year 1974 Deutsche B

- Page 3 and 4: Agenda for the Ordinary General Mee

- Page 5 and 6: von Siemens Meysenburg vari den Bri

- Page 7 and 8: Board of Managing Directors Horst B

- Page 9 and 10: Deutsche Bank at a glance Balance s

- Page 11 and 12: Partners begin to react to the fall

- Page 13 and 14: This is clearly illustrated hy reta

- Page 16 and 17: This darnage was revealed all the r

- Page 18 and 19: a marked recovery in the interest s

- Page 22 and 23: Port revenues of the oil-producing

- Page 24: New channels needed The above facts

- Page 27 and 28: W Our Bank's Business Interest rnar

- Page 29 and 30: Wider liquidlty margin In the secon

- Page 31 and 32: line with market requirements. The

- Page 33 and 34: issues, particularly in December. T

- Page 35 and 36: 1974 Foreign representative confere

- Page 37 and 38: Our bank in Luxembourg Since the en

- Page 39 and 40: US business on a broader basis The

- Page 41 and 42: Deutsche Bank 1 ~ 1 AKTlENCESELLSUi

- Page 43 and 44: women even more strongly in their c

- Page 45 and 46: A day in the Kronberg training cent

- Page 47 and 48: ie courirer rosrer psrsoriai curila

- Page 49 and 50: It is with deep regret that we repo

- Page 51 and 52: Liquidity Securities The bank's liq

- Page 53 and 54: diagram below in accordance with th

- Page 55 and 56: Other asset items Equalisation and

- Page 57 and 58: Other liability items The item sund

- Page 59 and 60: Other receipts efforts to expand it

- Page 61 and 62: Growth of Capital and Reserves Janu

- Page 63 and 64: Annual Balance Sheet as of Decem be

- Page 65: Balance Sheet as of December 31,197

- Page 68 and 69: The Growth of the Balance Sheet unt

- Page 70 and 71:

Report of the Group for 1974 Deutsc

- Page 72 and 73:

Hochhaus und Hotel Riesenfürstenho

- Page 74 and 75:

of the situation atid scope for sma

- Page 76 and 77:

& Trust Cornpany, New York (norn. U

- Page 78 and 79:

Funds from outside sources End of 1

- Page 80 and 81:

Outside shareholders of Deutsche Ce

- Page 82 and 83:

Assets - Cash in hand .. .. .. .. .

- Page 84:

Assets Consolidated Balance Sheet c

- Page 87 and 88:

for the period from January 1 to De

- Page 89 and 90:

Corporacion Financiera Colombiana,

- Page 91 and 92:

Security lssuing and other Syndicat

- Page 93 and 94:

Hessen-Nassauischc Gas-Aktiengesell

- Page 95 and 96:

Rudolf Stelbrink, General Manager,

- Page 97 and 98:

Dieter Prym, Partner and Managing D

- Page 99 and 100:

Advisory Council of Essen Josef Fis

- Page 101 and 102:

Heribert Kohlhaas, Managing Directo

- Page 103 and 104:

Dr. Gerhard Wiebe, Partner in Augus

- Page 105 and 106:

Ulrich Jorgens, Partner in Messrs.

- Page 107 and 108:

Kurt Beckh, Managing Director of F.

- Page 109 and 110:

F.-F. Herzog, General Manager and M

- Page 111 and 112:

Helmut Leuze, Partner in Leuze Text

- Page 113 and 114:

It is our sad duty to announce the

- Page 115 and 116:

Freiburg (Breisgau) with 7 Sub-Bran

- Page 117 and 118:

Leonberg (Württ) Lethmathe (Sauerl

- Page 119 and 120:

Holdings in German Banks Berliner D