- Page 1 and 2:

Controlling Indirect Selection unde

- Page 3 and 4:

iv ACKNOWLEDGEMENTS I am thankful f

- Page 5 and 6:

vi C. Regulatory Timing ...........

- Page 7 and 8:

viii 22. Profit = .................

- Page 9 and 10:

x MEPS P&C PBM PHI PPACA RA SES SOA

- Page 11 and 12:

I. INTRODUCTION Consultants from th

- Page 13 and 14:

3 This paper is meant to be a prime

- Page 15 and 16:

5 1970; Rothschild & Stiglitz, 1976

- Page 17 and 18:

7 the right side of the bar. With r

- Page 19 and 20:

9 limits choice for other high risk

- Page 21 and 22:

11 2. Process. Direct selection is

- Page 23 and 24:

13 just a department. This expansiv

- Page 25 and 26:

15 F. Consumers Demand Change Direc

- Page 27 and 28:

17 2. Risk adjustment (PPACA, Secti

- Page 29 and 30:

19 consumer selection. This section

- Page 31 and 32:

21 Whether the adjustment occurs vi

- Page 33 and 34:

23 risk. 43 Today’s risk adjustme

- Page 35 and 36:

25 Figure 8 Other Predictive Variab

- Page 37 and 38:

27 Genetics are also important. A d

- Page 39 and 40:

29 generally socially and economica

- Page 41 and 42:

31 of costs and very few have $50,0

- Page 43 and 44:

33 have no recent diagnoses or pres

- Page 45 and 46:

35 Unidentified Sick are unidentifi

- Page 47 and 48:

37 Figure 15 Demonstration: Financi

- Page 49 and 50:

39 The benefits of indirect selecti

- Page 51 and 52:

41 get insurance or gets it on less

- Page 53 and 54:

43 Assuming that at least some insu

- Page 55 and 56:

III. INDIRECT SELECTION UNDER HEALT

- Page 57 and 58:

47 insurers should use a Lifestyle

- Page 59 and 60:

49 Figure 19 Neighborhood-Level Dat

- Page 61 and 62:

51 This list of data elements align

- Page 63 and 64:

53 Consumer marketing databases pro

- Page 65 and 66:

55 Figure 23 New Business Predictiv

- Page 67 and 68:

57 diabetics while finding ways to

- Page 69 and 70:

59 risk insureds, “skimping” wi

- Page 71 and 72:

61 Figure 28 The model is consisten

- Page 73 and 74:

63 Insurers will rely upon predicti

- Page 75 and 76:

65 that they are related to the cha

- Page 77 and 78:

67 profitable and the second neighb

- Page 79 and 80:

69 relevant to insurers with a larg

- Page 81 and 82:

IV. PUBLIC POLICY CHALLENGES Indire

- Page 83 and 84:

73 will never be a clear line betwe

- Page 85 and 86:

75 healthcare cost variance outside

- Page 87 and 88:

77 to educate poor children. Althou

- Page 89 and 90:

79 Figure 30 Dynamic System: The ke

- Page 91 and 92:

81 regulators. If regulators don’

- Page 93 and 94:

83 regulatory front, while struggli

- Page 95 and 96:

85 in Chapter 3. The discussion wil

- Page 97 and 98:

87 1A: Include family income in ris

- Page 99 and 100:

89 example, assigning a risk premiu

- Page 101 and 102:

91 2. Market Entry Regulators desig

- Page 103 and 104:

93 2A: Individual insurance only fr

- Page 105 and 106:

95 “restricting choices”. It is

- Page 107 and 108:

97 adverse consumer selection. Whil

- Page 109 and 110:

99 3B: Fixed benefit designs. It is

- Page 111 and 112:

101 There is general consensus in t

- Page 113 and 114:

103 4D: Agent restrictions. At a mi

- Page 115 and 116:

105 Figure 35 Regulatory Options 5

- Page 117 and 118:

107 6. Post-Enrollment Consumer sel

- Page 119 and 120:

109 6E: Disenrollment per head pena

- Page 121 and 122:

111 While insurers cannot directly

- Page 123 and 124:

113 the insureds who have a diagnos

- Page 125 and 126:

115 E. Monitoring If regulations ar

- Page 127 and 128:

117 enrollment and disenrollment ra

- Page 129 and 130:

119 publicly discussed. Discussing

- Page 131 and 132:

121 Such a strategy is dependent up

- Page 133 and 134: REFERENCES AAA. (2009). Issue Brief

- Page 135 and 136: 125 Byrne, S. K. (2008). Healthcare

- Page 137 and 138: 127 Gallo, L. C., Penedo, F. J., Ex

- Page 139 and 140: 129 Lewin Group. (2010). Individual

- Page 141 and 142: 131 Riley, T. (2010). Reform has a

- Page 143 and 144: 133 van Barneveld, E., van Vliet, R

- Page 145 and 146: APPENDIX Health Insurance Risk Adju

- Page 147 and 148: Appendix 137 ABSTRACT The U.S. Pati

- Page 149 and 150: Appendix 139 BACKGROUND As expresse

- Page 151 and 152: Appendix 141 not eligible for subsi

- Page 153 and 154: Appendix 143 Starting in 2011 insur

- Page 155 and 156: Appendix 145 1) Current conditions

- Page 157 and 158: Appendix 147 First consider the lin

- Page 159 and 160: Appendix 149 counter this argument.

- Page 161 and 162: Appendix 151 Current Risk Adjustmen

- Page 163 and 164: Appendix 153 Model 4 fits the risk

- Page 165 and 166: Appendix 155 An examination of the

- Page 167 and 168: Appendix 157 ANALYSIS Data Descript

- Page 169 and 170: Appendix 159 Specifically, the anal

- Page 171 and 172: Appendix 161 Equation 1 Proxy Expen

- Page 173 and 174: Appendix 163 Expenditures have been

- Page 175 and 176: Appendix 165 Equation 3 Normalized

- Page 177 and 178: Appendix 167 The technical difficul

- Page 179 and 180: Appendix 169 prediction residuals?

- Page 181 and 182: Appendix 171 The lower income and h

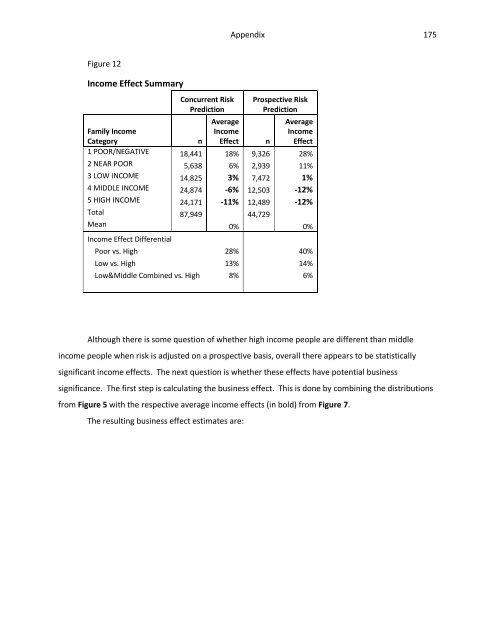

- Page 183: Appendix 173 RESULTS The results ar

- Page 187 and 188: Appendix 177 LIMITATIONS The analys

- Page 189 and 190: Appendix 179 Likewise, due to healt

- Page 191 and 192: Appendix 181 DISCUSSION Even with t

- Page 193 and 194: Appendix 183 Much of Jost’s timel

- Page 195 and 196: Appendix 185 RECOMMENDATIONS Based

- Page 197 and 198: Appendix 187 TABLES

- Page 199 and 200: Appendix 189

- Page 201 and 202: Appendix 191

- Page 203 and 204: Appendix 193 REFERENCES AAA. (2010)

- Page 205 and 206: Appendix 195 Diez Roux, A. A. (2001

- Page 207 and 208: Appendix 197 McKinsey & Company. (2

- Page 209 and 210: Appendix 199 WHO. (2005). Facing th

- Page 211 and 212: TIA GOSS SAWHNEY Vita 201 Directo

- Page 213 and 214: TIA GOSS SAWHNEY Vita 203 “Busine