0306E - Faculty of Social Sciences - Université d'Ottawa

0306E - Faculty of Social Sciences - Université d'Ottawa

0306E - Faculty of Social Sciences - Université d'Ottawa

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

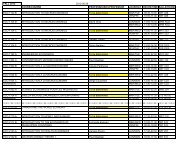

7 Appendix B<br />

In this appendix, we present the models estimated for each <strong>of</strong> the series for<br />

forecasting evaluation. All equations present the following statistics and diagnostic<br />

tests. The R 2 is the coe¢cient <strong>of</strong> determination measuring the …t<br />

<strong>of</strong> the data. The F-statistic tests the null hypothesis that all coe¢cients <strong>of</strong><br />

the regression are null (exception <strong>of</strong> the intercept). The DW is the Durbin-<br />

Watson statistic testing for the presence <strong>of</strong> …rst-order autocorrelation, see<br />

Durbin and Watson (1951). The e¾ is the estimated standard deviation <strong>of</strong><br />

the regression. The AIC is the Akaike information criteria. The BIC is<br />

the Bayesian information criteria. The LJB is the statistic testing for nonnormal<br />

residuals proposed by Doornik and Hansen (1994), which considers<br />

a small sample correction based on the original statistic proposed by Jarque<br />

and Bera (1987). The LM AR (p) is a Lagrange Multiplier statistic testing<br />

for the presence <strong>of</strong> correlation <strong>of</strong> order p in the residuals <strong>of</strong> the regression,<br />

see Harvey (1990). The F ARCH is an F-statistic testing for the presence<br />

<strong>of</strong> autoregressive conditional hereroskedasticity, see Engle (1982). The RE-<br />

SET statistic test for misspeci…cation in the estimated equation, see Ramsey<br />

(1969). In the case <strong>of</strong> the PAR models, two more statistics are presented.<br />

The F PER is an F-statistic testing for periodicity in the coe¢cients <strong>of</strong> the<br />

estimated PAR models where the null hypothesis is constancy <strong>of</strong> the coe¢cients,<br />

see Franses (1996). The LR ¿=0 statistic tests for the null hypothesis<br />

<strong>of</strong> constancy <strong>of</strong> the coe¢cients associated to the time trend. The Q(i; j)<br />

is the statistic <strong>of</strong> Ljung and Box (1978) based on the …rst i residuals autocorrelations.<br />

The value PEV is the prediction error variance <strong>of</strong> one step<br />

ahead predictor errors. Further we included seasonal dummy variables and<br />

outlier dummy variables in some <strong>of</strong> our regressions. The seasonal dummies<br />

are de…ned as D t;s = 1 if s = t and 0 otherwise. An example <strong>of</strong> an outlier<br />

dummy used for all series for obvious reason is D2001 : 09 representing<br />

September, 2001. Values in parenthesis below coe¢cient estimates are the<br />

standard errors.<br />

26