Republic Insurance Company Limited - Credit Rating Agency of ...

Republic Insurance Company Limited - Credit Rating Agency of ...

Republic Insurance Company Limited - Credit Rating Agency of ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

CRAB <strong>Rating</strong>s<br />

General <strong>Insurance</strong><br />

<strong>Rating</strong> Report (Surveillance)<br />

<strong>Republic</strong> <strong>Insurance</strong> <strong>Company</strong> <strong>Limited</strong><br />

<strong>Rating</strong>s<br />

Previous <strong>Rating</strong>s<br />

Long Term : BBB 3 Long Term : BBB 3<br />

Short Term : ST-3 Short Term : ST-3<br />

Date <strong>of</strong> <strong>Rating</strong> : 31 December 2009 Date <strong>of</strong> <strong>Rating</strong> : 21 December 2008<br />

Validity : 30 June 201010<br />

Analyst<br />

Fareba Naz Shaule<br />

Financial Analyst<br />

fareba.naz@crab.com.bd<br />

1.0 RATIONALE<br />

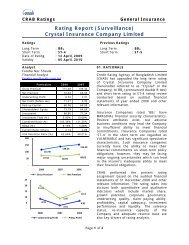

Financial Highlights<br />

BDT in million<br />

Particulars 2008 2007<br />

Gross Premium 166.68 129.57<br />

Net Premium 98.60 87.19<br />

Underwriting Pr<strong>of</strong>it 5.16 10.72<br />

Pretax Pr<strong>of</strong>it 22.21 14.12<br />

Paid up Capital 150.00 60.00<br />

Shareholders’ Equity 168.97 69.26<br />

Investment 89.58 81.56<br />

Investment Yield 26.42% 9.73%<br />

Combined Ratio 107.59% 98.68%<br />

Return on Average Assets 8.94% 8.60%<br />

Risk Retention Ratios 59.15% 67.29%<br />

Current Ratio (times) 1.96 1.53<br />

180<br />

160<br />

140<br />

120<br />

100<br />

80<br />

60<br />

40<br />

20<br />

25<br />

20<br />

15<br />

10<br />

5<br />

-<br />

0<br />

53.71%<br />

34.84%<br />

83.03%<br />

6.22%<br />

2004 2005 2006 2007 2008<br />

90%<br />

80%<br />

70%<br />

60%<br />

50%<br />

40%<br />

30%<br />

20%<br />

13.08%<br />

10%<br />

Gross Premium Net Premium Growth in Net Premium<br />

4.81<br />

5.56<br />

2.36 2.30<br />

6.38<br />

3.87<br />

14.12<br />

10.72<br />

22.21<br />

5.16<br />

2004 2005 2006 2007 2008<br />

Underwriting Pr<strong>of</strong>it Pretax Pr<strong>of</strong>it<br />

0%<br />

<strong>Credit</strong> <strong>Rating</strong> <strong>Agency</strong> <strong>of</strong> Bangladesh <strong>Limited</strong><br />

(CRAB) has retained BBB 3 (Triple B three) rating<br />

in the long term and ST-3 rating in the short<br />

term <strong>of</strong> <strong>Republic</strong> <strong>Insurance</strong> <strong>Company</strong> <strong>Limited</strong><br />

(hereinafter referred to as ‘RICL’ or ‘the<br />

<strong>Company</strong>’). The rating analysis was based on the<br />

audited financial statements for the year ended<br />

2008 and other relevant information.<br />

<strong>Insurance</strong> Companies rated ‘BBB 3 ’ have good<br />

financial security characteristics, but are more<br />

likely to be affected by adverse business<br />

conditions than higher rated insurers. <strong>Insurance</strong><br />

Companies rated ‘ST-3’ have an adequate ability<br />

to meet their financial commitments on shortterm<br />

policy obligations. However, adverse<br />

economic conditions or changing circumstances<br />

are more likely to lead to a weakened ability <strong>of</strong><br />

the insurers to meet their financial obligations.<br />

The rating takes into account both quantitative<br />

and qualitative indicators which include market<br />

share, growth potential, corporate governance,<br />

underwriting quality, claim paying ability,<br />

pr<strong>of</strong>itability, capital adequacy, investment<br />

performance and liquidity. The solvency status,<br />

re-insurance capacity <strong>of</strong> the <strong>Company</strong> and<br />

adequate reserve base are also key drivers <strong>of</strong><br />

rating analysis.<br />

RICL’s gross premium has increased by 28.63%<br />

to BDT 166.68 million from 129.57 million in<br />

2008 whereas gross claim has increased by<br />

Page 1 <strong>of</strong> 2

CRAB <strong>Rating</strong>s<br />

General <strong>Insurance</strong><br />

139.57% to BDT 46.01 million from BDT 19.20 million in 2007.<br />

In 2008 RICL’s combined ratio has increased to 107.59% from 98.68% as the loss ratio has<br />

increased to 25.24% from 8.41% due to 239.28% increase in net claim. On the other hand,<br />

RICL was able to decrease its expense ratio to 82.35% from 90.27% in 2007.<br />

In 2008 the underwriting Pr<strong>of</strong>it decreased by 51.89% to BDT 5.16 million from BDT 10.72<br />

million in 2007. For last five years the net pr<strong>of</strong>it before tax <strong>of</strong> RICL shows an increasing<br />

trend. In 2008 RICL’s net pr<strong>of</strong>it before tax increased by 57.27% to BDT 22.21 million from<br />

BDT 14.12 million in 2007. The ROAA <strong>of</strong> RICL increased to 8.94% from 8.60% in 2008 due<br />

to increase in both pr<strong>of</strong>it before tax and total asset <strong>of</strong> the <strong>Company</strong>. On the other hand, the<br />

ROAE decreased to 18.64% from 21.28% due to high growth in shareholders’ equity<br />

compare to pr<strong>of</strong>it before tax.<br />

RICL follows a conservative investment policy as 99.35% <strong>of</strong> total investment was made in<br />

national investment bond and in fixed deposits. In 2008 the investment & other income <strong>of</strong><br />

RICL increased by 198.31% to BDT 23.66 million from BDT 7.93 million in 2007. As a result<br />

<strong>of</strong> which the investment yield has increased to 26.42% from 9.73% in 2007.<br />

RICL has a strong Board <strong>of</strong> Directors who has sufficient exposure to diversify industrial<br />

sectors though the <strong>Company</strong> is yet to incorporate an independent director in the Board.<br />

During this period RICL did not bring any mentionable change in the management and<br />

management information system. Due to small structure <strong>of</strong> the <strong>Company</strong> there has been<br />

lack <strong>of</strong> standardized internal control system.<br />

In October 2008 the <strong>Company</strong> raised its paid up capital to BDT 150 million from BDT 60<br />

million through Initial Public Offering (IPO). On the other hand, the reserve for exceptional<br />

loss has increased by 105.56% to BDT 18.97 million from BDT 9 million in 2007. As a result<br />

<strong>of</strong> which the shareholders equity has increased by 143.96% to BDT 168.97 million from BDT<br />

69.26 million in 2007.<br />

In 2008 the total management expenses <strong>of</strong> RICL was BDT 81.19 million which has increased<br />

by 3.16% over that <strong>of</strong> previous year which was 34.59% excess over the allowable<br />

management expenses.<br />

In 2008 RICL settled an amount <strong>of</strong> BDT 48.30 million claims (including repudiated claims)<br />

out <strong>of</strong> BDT 68.57 million claims and BDT 20.27 million claims were outstanding. So the<br />

claim settlement ratio <strong>of</strong> the <strong>Company</strong> increased to 70.43% from 67.68% in 2008.<br />

The overall liquidity position during this period has improved. The current ratio has<br />

increased to 1.96 times from 1.53 times in 2008. On the other hand, the proportion <strong>of</strong> liquid<br />

assets to total assets was 62.48% in 2008 which was 49.20% in 2007. The net claim<br />

payable ability decreased to 11.81 times from 20.90 times in 2007. In 2008 the required<br />

solvency margin was 4.76 times <strong>of</strong> actual solvency margin which was only 1.39 times in<br />

2007.<br />

In 2008 the <strong>Company</strong> decreased its retention to 59.15% from 67.29% and to comply with<br />

the insurance act it maintains 40% <strong>of</strong> net premium as reserve for unexpired risk except for<br />

marine hull where it maintains 100%.<br />

Page 2 <strong>of</strong> 2