Life cycle costing (LCC) as a contribution to sustainable construction ...

Life cycle costing (LCC) as a contribution to sustainable construction ...

Life cycle costing (LCC) as a contribution to sustainable construction ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Towards a common European methodology for <strong>Life</strong> Cycle Costing (<strong>LCC</strong>) – Guidance Document<br />

48<br />

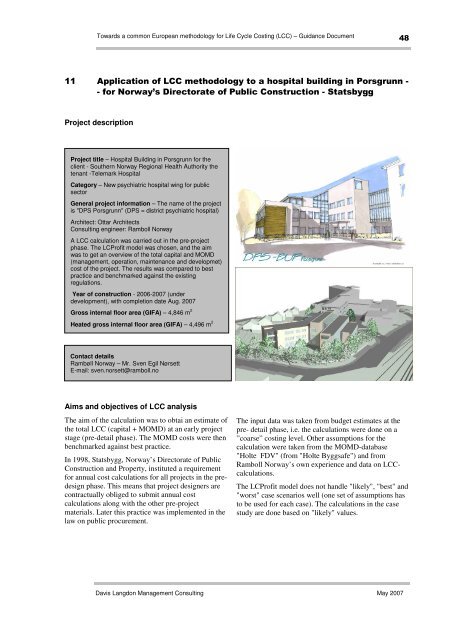

11 Application of <strong>LCC</strong> methodology <strong>to</strong> a hospital building in Porsgrunn -<br />

- for Norway’s Direc<strong>to</strong>rate of Public Construction - Statsbygg<br />

Project description<br />

Project title – Hospital Building in Porsgrunn for the<br />

client - Southern Norway Regional Health Authority the<br />

tenant -Telemark Hospital<br />

Category – New psychiatric hospital wing for public<br />

sec<strong>to</strong>r<br />

General project information – The name of the project<br />

is "DPS Porsgrunn" (DPS = district psychiatric hospital)<br />

Architect: Ottar Architects<br />

Consulting engineer: Ramboll Norway<br />

A <strong>LCC</strong> calculation w<strong>as</strong> carried out in the pre-project<br />

ph<strong>as</strong>e. The LCProfit model w<strong>as</strong> chosen, and the aim<br />

w<strong>as</strong> <strong>to</strong> get an overview of the <strong>to</strong>tal capital and MOMD<br />

(management, operation, maintenance and developmet)<br />

cost of the project. The results w<strong>as</strong> compared <strong>to</strong> best<br />

practice and benchmarked against the existing<br />

regulations.<br />

Year of <strong>construction</strong> - 2006-2007 (under<br />

development), with completion date Aug. 2007<br />

Gross internal floor area (GIFA) – 4,846 m 2<br />

Heated gross internal floor area (GIFA) – 4,496 m 2<br />

Contact details<br />

Rambøll Norway – Mr. Sven Egil Nørsett<br />

E-mail: sven.norsett@ramboll.no<br />

Aims and objectives of <strong>LCC</strong> analysis<br />

The aim of the calculation w<strong>as</strong> <strong>to</strong> obtai an estimate of<br />

the <strong>to</strong>tal <strong>LCC</strong> (capital + MOMD) at an early project<br />

stage (pre-detail ph<strong>as</strong>e). The MOMD costs were then<br />

benchmarked against best practice.<br />

In 1998, Statsbygg, Norway’s Direc<strong>to</strong>rate of Public<br />

Construction and Property, instituted a requirement<br />

for annual cost calculations for all projects in the predesign<br />

ph<strong>as</strong>e. This means that project designers are<br />

contractually obliged <strong>to</strong> submit annual cost<br />

calculations along with the other pre-project<br />

materials. Later this practice w<strong>as</strong> implemented in the<br />

law on public procurement.<br />

The input data w<strong>as</strong> taken from budget estimates at the<br />

pre- detail ph<strong>as</strong>e, i.e. the calculations were done on a<br />

”coarse” <strong>costing</strong> level. Other <strong>as</strong>sumptions for the<br />

calculation were taken from the MOMD-datab<strong>as</strong>e<br />

"Holte FDV" (from "Holte Byggsafe") and from<br />

Ramboll Norway’s own experience and data on <strong>LCC</strong>calculations.<br />

The LCProfit model does not handle "likely", "best" and<br />

"worst" c<strong>as</strong>e scenarios well (one set of <strong>as</strong>sumptions h<strong>as</strong><br />

<strong>to</strong> be used for each c<strong>as</strong>e). The calculations in the c<strong>as</strong>e<br />

study are done b<strong>as</strong>ed on "likely" values.<br />

Davis Langdon Management Consulting May 2007