Annual report 2008-OK-B-up.qxp - Canadia Bank Plc.

Annual report 2008-OK-B-up.qxp - Canadia Bank Plc.

Annual report 2008-OK-B-up.qxp - Canadia Bank Plc.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

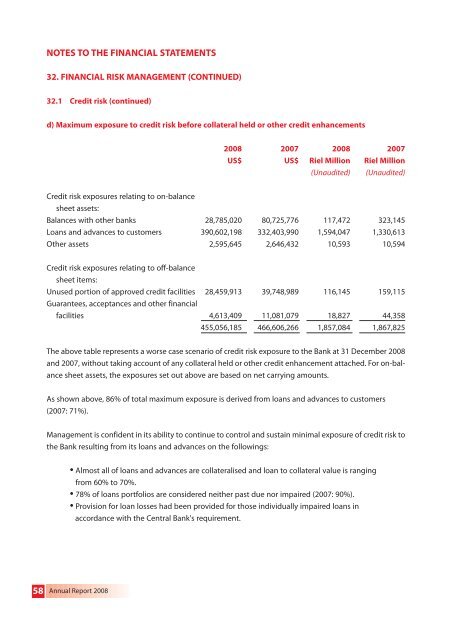

NOTES TO THE FINANCIAL STATEMENTS<br />

32. FINANCIAL RISK MANAGEMENT (CONTINUED)<br />

32.1 Credit risk (continued)<br />

d) Maximum exposure to credit risk before collateral held or other credit enhancements<br />

<strong>2008</strong> 2007 <strong>2008</strong> 2007<br />

US$ US$ Riel Million Riel Million<br />

(Unaudited) (Unaudited)<br />

Credit risk exposures relating to on-balance<br />

sheet assets:<br />

Balances with other banks 28,785,020 80,725,776 117,472 323,145<br />

Loans and advances to customers 390,602,198 332,403,990 1,594,047 1,330,613<br />

Other assets 2,595,645 2,646,432 10,593 10,594<br />

Credit risk exposures relating to off-balance<br />

sheet items:<br />

Unused portion of approved credit facilities 28,459,913 39,748,989 116,145 159,115<br />

Guarantees, acceptances and other financial<br />

facilities 4,613,409 11,081,079 18,827 44,358<br />

455,056,185 466,606,266 1,857,084 1,867,825<br />

The above table represents a worse case scenario of credit risk exposure to the <strong>Bank</strong> at 31 December <strong>2008</strong><br />

and 2007, without taking account of any collateral held or other credit enhancement attached. For on-balance<br />

sheet assets, the exposures set out above are based on net carrying amounts.<br />

As shown above, 86% of total maximum exposure is derived from loans and advances to customers<br />

(2007: 71%).<br />

Management is confident in its ability to continue to control and sustain minimal exposure of credit risk to<br />

the <strong>Bank</strong> resulting from its loans and advances on the followings:<br />

• Almost all of loans and advances are collateralised and loan to collateral value is ranging<br />

from 60% to 70%.<br />

• 78% of loans portfolios are considered neither past due nor impaired (2007: 90%).<br />

• Provision for loan losses had been provided for those individually impaired loans in<br />

accordance with the Central <strong>Bank</strong>'s requirement.<br />

58<br />

<strong>Annual</strong> Report <strong>2008</strong>