PDF, 3464 KB - Roland Berger

PDF, 3464 KB - Roland Berger

PDF, 3464 KB - Roland Berger

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

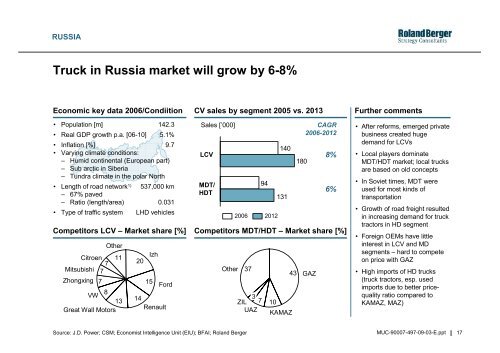

RUSSIA<br />

Truck in Russia market will grow by 6-8%<br />

Economic key data 2006/Condiition<br />

• Population [m] 142.3<br />

• Real GDP growth p.a. [06-10] 5.1%<br />

• Inflation [%] 9.7<br />

• Varying climate conditions:<br />

– Humid continental (European part)<br />

– Sub arctic in Siberia<br />

– Tundra climate in the polar North<br />

• Length of road network 1) 537,000 km<br />

– 67% paved<br />

– Ratio (length/area) 0.031<br />

• Type of traffic system LHD vehicles<br />

Competitors LCV – Market share [%]<br />

Citroen<br />

7<br />

Mitsubishi 7<br />

Zhongxing 7<br />

Other<br />

11<br />

8<br />

VW<br />

13<br />

Great Wall Motors<br />

20<br />

Izh<br />

15 Ford<br />

14<br />

Renault<br />

CV sales by segment 2005 vs. 2013<br />

Sales [’000]<br />

LCV<br />

MDT/<br />

HDT<br />

Other<br />

94<br />

2006 2012<br />

37<br />

3<br />

ZIL 7<br />

UAZ<br />

10<br />

140<br />

131<br />

KAMAZ<br />

180<br />

43 GAZ<br />

CAGR<br />

2006-2012<br />

8%<br />

6%<br />

Competitors MDT/HDT – Market share [%]<br />

Further comments<br />

• After reforms, emerged private<br />

business created huge<br />

demand for LCVs<br />

• Local players dominate<br />

MDT/HDT market; local trucks<br />

are based on old concepts<br />

• In Soviet times, MDT were<br />

used for most kinds of<br />

transportation<br />

• Growth of road freight resulted<br />

in increasing demand for truck<br />

tractors in HD segment<br />

• Foreign OEMs have little<br />

interest in LCV and MD<br />

segments – hard to compete<br />

on price with GAZ<br />

• High imports of HD trucks<br />

(truck tractors, esp. used<br />

imports due to better pricequality<br />

ratio compared to<br />

KAMAZ, MAZ)<br />

Source: J.D. Power; CSM; Economist Intelligence Unit (EIU); BFAI; <strong>Roland</strong> <strong>Berger</strong><br />

MUC-90007-497-09-03-E.ppt 17