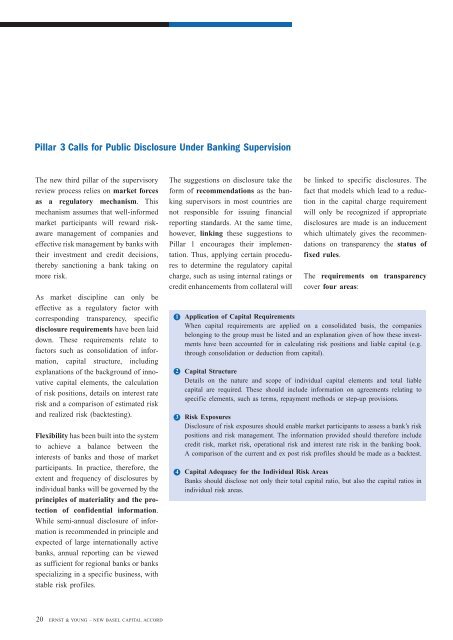

Pillar 3 Calls for Public Disclosure Under Banking SupervisionThe new third pillar of the supervisoryreview process relies on market forcesas a regulatory mechanism. Thismechanism assumes that well-informedmarket participants will reward riskawaremanagement of companies andeffective risk management by banks withtheir investment and credit decisions,thereby sanctioning a bank taking onmore risk.As market discipline can only beeffective as a regulatory factor withcorresponding transparency, specificdisclosure requirements have been laiddown. These requirements relate tofactors such as consolidation of information,capital structure, includingexplanations of the background of innovativecapital elements, the calculationof risk positions, details on interest raterisk and a comparison of estimated riskand realized risk (backtesting).Flexibility has been built into the systemto achieve a balance between theinterests of banks and those of marketparticipants. In practice, therefore, theextent and frequency of disclosures byindividual banks will be governed by theprinciples of materiality and the protectionof confidential information.While semi-annual disclosure of informationis recommended in principle andexpected of large internationally activebanks, annual reporting can be viewedas sufficient for regional banks or banksspecializing in a specific business, withstable risk profiles.The suggestions on disclosure take theform of recommendations as the bankingsupervisors in most countries arenot responsible for issuing financialreporting standards. At the same time,however, linking these suggestions toPillar 1 encourages their implementation.Thus, applying certain proceduresto determine the regulatory capitalcharge, such as using internal ratings orcredit enhancements from collateral will1234be linked to specific disclosures. Thefact that models which lead to a reductionin the capital charge requirementwill only be recognized if appropriatedisclosures are made is an inducementwhich ultimately gives the recommendationson transparency the status offixed rules.The requirements on transparencycover four areas:Application of <strong>Capital</strong> RequirementsWhen capital requirements are applied on a consolidated basis, the companiesbelonging to the group must be listed and an explanation given of how these investmentshave been accounted for in calculating risk positions and liable capital (e.g.through consolidation or deduction from capital).<strong>Capital</strong> StructureDetails on the nature and scope of individual capital elements and total liablecapital are required. These should include information on agreements relating tospecific elements, such as terms, repayment methods or step-up provisions.Risk ExposuresDisclosure of risk exposures should enable market participants to assess a bank’s riskpositions and risk management. The information provided should therefore includecredit risk, market risk, operational risk and interest rate risk in the banking book.A comparison of the current and ex post risk profiles should be made as a backtest.<strong>Capital</strong> Adequacy for the Individual Risk AreasBanks should disclose not only their total capital ratio, but also the capital ratios inindividual risk areas.20 ERNST & YOUNG – NEW BASEL CAPITAL ACCORD

Bibliography - Selected Current Literature on The <strong>New</strong> <strong>Basel</strong> <strong>Capital</strong> <strong>Accord</strong> -Author<strong>Basel</strong> Committee on Banking Supervision (1999)<strong>Basel</strong> Committee on Banking Supervision (2000)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2001)<strong>Basel</strong> Committee on Banking Supervision (2002)<strong>Basel</strong> Committee on Banking Supervision (2002)<strong>Basel</strong> Committee on Banking Supervision (2002)Secretariat of the <strong>Basel</strong> Committee on BankingSupervision (2001)ECB (2001)ECB (2001)TitleA <strong>New</strong> <strong>Capital</strong> Adequacy Framework, <strong>Basel</strong> Committee Publications No. 50, June 1999.Range of Practice in Banks’ Internal Ratings Systems, <strong>Basel</strong> Committee Publications No. 66,January 2000.Overview of The <strong>New</strong> <strong>Basel</strong> <strong>Capital</strong> <strong>Accord</strong>, Consultative Document, January 2001.The <strong>New</strong> <strong>Basel</strong> <strong>Capital</strong> <strong>Accord</strong>, Consultative Document, January 2001.The Standardised Approach to Credit Risk, Consultative Document, January 2001.The Internal Ratings-Based Approach, Consultative Document, January 2001.Criteria in Defining Exceptional Treatment of Commercial Real Estate Lending, Supplement,January 2001.Asset Securitisation, Consultative Document, January 2001.Operational Risk, Consultative Document, January 2001.Pillar 2 (Supervisory Review Process), Consultative Document, January 2001.Principles for the Management and Supervision of Interest Rate Risk, Consultative Document,January 2001.Pillar 3 (Market Discipline), Consultative Document, January 2001.IRB Treatment of Expected Losses and Future Margin Income, Working Paper No. 5, July 2001.Risk Sensitive Approaches for Equity Exposures in the Banking Book for IRB Banks, WorkingPaper No. 6, August 2001.Pillar 3 – Market Discipline, Working Paper No. 7, September 2001.Regulatory Treatment of Operational Risk, Working Paper No. 8, September 2001.Update on Work on the <strong>New</strong> <strong>Basel</strong> <strong>Capital</strong> <strong>Accord</strong>, <strong>Basel</strong> Committee <strong>New</strong>sletter No. 2, September2001.Internal Ratings-Based Approach to Specialised Lending Exposures, Working Paper No. 9, October2001.Treatment of Asset Securitisations, Working Paper No. 10, October 2001.Potential Modifications to the Committee’s Proposals, November 5, 2001.Sound Practices for the Management and Supervision of Operational Risk, <strong>Basel</strong> Committee PublicationNo. 86, December 2001.Progress Towards Completion of the <strong>New</strong> <strong>Basel</strong> <strong>Capital</strong> <strong>Accord</strong>, Press Release, December 13, 2001.Sound Practices for the Management and Supervision of Operational Risk, July 2002.Operational Risk Data Collection Exercise – 2002, June 4, 2002.Results of Quantitative Impact Study 2.5, June 25, 2002.The <strong>New</strong> <strong>Basel</strong> <strong>Capital</strong> <strong>Accord</strong>: An Explanatory Note, January 2001.The <strong>New</strong> <strong>Capital</strong> Adequacy Regime – The ECB Perspective, in: ECB Monthly Bulletin May 2001,pp. 59-74.Banking and Financial Regulation, in: ECB Annual Report 2001, pp. 140-142.References to German literature havebeen omitted.ERNST & YOUNG – NEW BASEL CAPITAL ACCORD21