Is inflation targeting dead? Central Banking After the Crisis - Vox

Is inflation targeting dead? Central Banking After the Crisis - Vox

Is inflation targeting dead? Central Banking After the Crisis - Vox

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

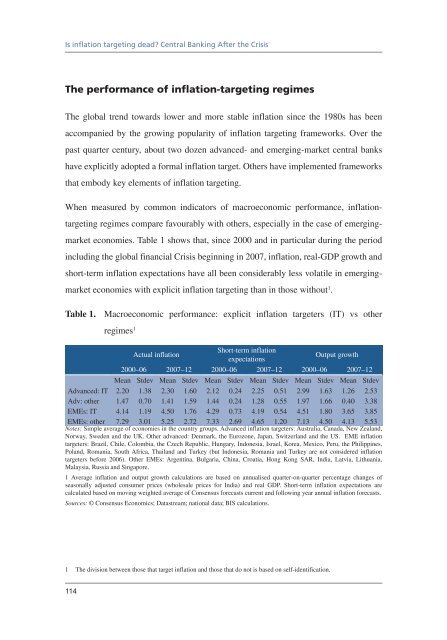

<strong>Is</strong> <strong>inflation</strong> <strong>targeting</strong> <strong>dead</strong>? <strong>Central</strong> <strong>Banking</strong> <strong>After</strong> <strong>the</strong> <strong>Crisis</strong>The performance of <strong>inflation</strong>-<strong>targeting</strong> regimesThe global trend towards lower and more stable <strong>inflation</strong> since <strong>the</strong> 1980s has beenaccompanied by <strong>the</strong> growing popularity of <strong>inflation</strong> <strong>targeting</strong> frameworks. Over <strong>the</strong>past quarter century, about two dozen advanced- and emerging-market central bankshave explicitly adopted a formal <strong>inflation</strong> target. O<strong>the</strong>rs have implemented frameworksthat embody key elements of <strong>inflation</strong> <strong>targeting</strong>.When measured by common indicators of macroeconomic performance, <strong>inflation</strong><strong>targeting</strong>regimes compare favourably with o<strong>the</strong>rs, especially in <strong>the</strong> case of emergingmarketeconomies. Table 1 shows that, since 2000 and in particular during <strong>the</strong> periodincluding <strong>the</strong> global financial <strong>Crisis</strong> beginning in 2007, <strong>inflation</strong>, real-GDP growth andshort-term <strong>inflation</strong> expectations have all been considerably less volatile in emergingmarketeconomies with explicit <strong>inflation</strong> <strong>targeting</strong> than in those without 1 .Table 1. Macroeconomic performance: explicit <strong>inflation</strong> targeters (IT) vs o<strong>the</strong>rregimes 1 Short-term <strong>inflation</strong>Actual <strong>inflation</strong>Output grow<strong>the</strong>xpectations2000–06 2007–12 2000–06 2007–12 2000–06 2007–12Mean Stdev Mean Stdev Mean Stdev Mean Stdev Mean Stdev Mean StdevAdvanced: IT 2.20 1.38 2.30 1.60 2.12 0.24 2.25 0.51 2.99 1.63 1.26 2.53Adv: o<strong>the</strong>r 1.47 0.70 1.41 1.59 1.44 0.24 1.28 0.55 1.97 1.66 0.40 3.38EMEs: IT 4.14 1.19 4.50 1.76 4.29 0.73 4.19 0.54 4.51 1.80 3.65 3.85EMEs: o<strong>the</strong>r 7.29 3.01 5.25 2.72 7.33 2.69 4.65 1.20 7.13 4.50 4.13 5.53Notes: Simple average of economies in <strong>the</strong> country groups. Advanced <strong>inflation</strong> targeters: Australia, Canada, New Zealand,Norway, Sweden and <strong>the</strong> UK. O<strong>the</strong>r advanced: Denmark, <strong>the</strong> Eurozone, Japan, Switzerland and <strong>the</strong> US. EME <strong>inflation</strong>targeters: Brazil, Chile, Colombia, <strong>the</strong> Czech Republic, Hungary, Indonesia, <strong>Is</strong>rael, Korea, Mexico, Peru, <strong>the</strong> Philippines,Poland, Romania, South Africa, Thailand and Turkey (but Indonesia, Romania and Turkey are not considered <strong>inflation</strong>targeters before 2006). O<strong>the</strong>r EMEs: Argentina, Bulgaria, China, Croatia, Hong Kong SAR, India, Latvia, Lithuania,Malaysia, Russia and Singapore.1 Average <strong>inflation</strong> and output growth calculations are based on annualised quarter-on-quarter percentage changes ofseasonally adjusted consumer prices (wholesale prices for India) and real GDP. Short-term <strong>inflation</strong> expectations arecalculated based on moving weighted average of Consensus forecasts current and following year annual <strong>inflation</strong> forecasts.Sources: © Consensus Economics; Datastream; national data; BIS calculations.1 The division between those that target <strong>inflation</strong> and those that do not is based on self-identification.114