Women’s economic opportunityA new global index and ranking9. “Financial Access 2009:Measuring access to financialservices around the world”,Consultative Group to Assist thePoor, 2009.10. M Bruhn and I Love, “The<strong>Economic</strong> Impact of Bankingthe Unbanked: Evidence fromMexico”, World Bank PolicyResearch Working Paper No.4981, World Bank: WashingtonDC, 2009.11. M Pickens, D Porteousand S Rotman, “Scenarios forBranchless Banking in 2020”,Consultative Group to Assist thePoor: Washington DC, 2009.12. ibid.Malaysia launched a joint programme—a “Portfolio Guarantee Scheme”—that aims to give womenentrepreneurs fast access to finance. In addition, the government has allocated M$46.3m to a WomenEntrepreneurs Scheme, which consists of soft loans and grants. Vietnam has formal initiatives toprovide financial accounts to women. Sacombank operates special branches for women entrepreneurs,and Agribank runs a programme to open savings and other accounts in rural areas that target women.Moreover, the Vietnam Women’s Union collaborates with banks to provide financing for women forhousehold economic activities and entrepreneurial activities. Only around 10% of Vietnamese, however,have a bank account, meaning that the scope of these programmes is currently limited.The delivering financial services indicator assesses bank initiatives to provide financial services intwo areas: the provision of basic, low-fee accounts for low-income clients, and whether private operatorscan provide financial services at post offices. The former captures accounts that either do not have feesor ones that are very low, that offer a small number of free automatic teller machine (ATM) transactions,and that have no minimum balance requirements. Of 139 countries surveyed by the Consultative Group toAssist the Poor (CGAP), 9 20 had financial regulations that mandated the provision of these accounts. Fromthe developing countries covered in the Women’s <strong>Economic</strong> <strong>Opportunity</strong> <strong>Index</strong>, only Argentina, Chile,Colombia, Hungary, India, Iran, Malaysia, Mexico, Morocco and Pakistan had such provisions.For example, in Mexico (which has a low-fee bank account policy in place), the opening in 2002 of anew bank targeting Mexico’s middle and working classes was not only a major commercial success butalso resulted in increased entrepreneurial activity, employment and income for its customers. Startingin 2002, Banco Azteca opened 815 branches in 250 Mexican cities in short succession. Results from animpact evaluation showed that after a bank branch opened, more informal businesses owned by menopened, and more women became employed as wage-earners. 10 The evaluation hypothesises that with thenew bank, the increased availability of credit allowed men to start or expand their informal businesses,which then in turn employed women as wage-earners. Banco Azteca has since expanded to other Centraland South American countries, including Brazil and Peru.Even so, this sort of policy may only be effective if banks are within reach and if potential clients arefinancially literate—access to banks is an issue in rural areas in many developing countries. Obtaining aloan or opening a bank account typically involves a visit to a bank branch in most countries. The provisionof financial services at post offices is one way to reach underserved markets: according to CGAP, about70% of the countries it surveyed delivered financial services through post offices. Banking at post officesis just one aspect of so-called branchless banking, for which there has been a growing demand, especiallyin developing countries. Financial service providers are keen to meet that demand by supplying innovativenew services such as banking over mobile phones. In Kenya, more than 7m people have signed up for amobile payment service called M-PESA, offered by Safaricom, Kenya’s largest mobile network operator,since its commercial launch in 2007. Partly as a result of M-PESA’s success, the proportion of Kenyansconsidered to be formally financially included has almost doubled, to 41% in just three years. 11 A differentapproach to branchless banking that has been successful in Brazil has been to combine mobile bankingwith point-of-sale devices that are operated by agents such as small convenience stores. 12 Future updatesof this model may explore the increasing take-up of branchless banking approaches.25© <strong>Economist</strong> <strong>Intelligence</strong> <strong>Unit</strong> Limited 2010

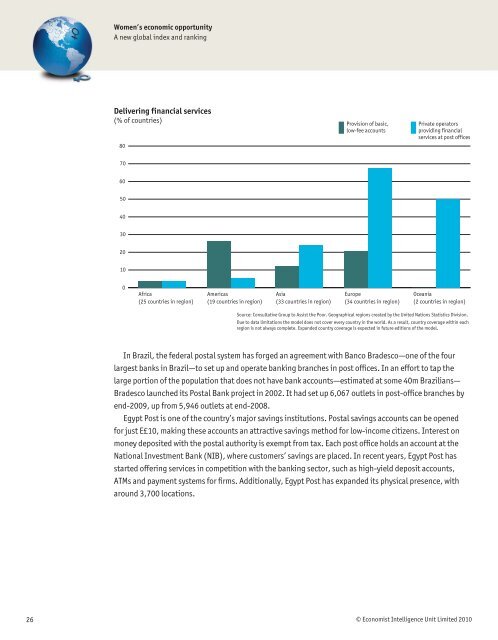

Women’s economic opportunityA new global index and rankingDelivering financial services(% of countries)80Provision of basic,low-fee accountsPrivate operatorsproviding financialservices at post offices706050403020100Africa(25 countries in region)Americas(19 countries in region)Asia(33 countries in region)Europe(34 countries in region)Oceania(2 countries in region)Source: Consultative Group to Assist the Poor. Geographical regions created by the <strong>Unit</strong>ed Nations Statistics Division.Due to data limitations the model does not cover every country in the world. As a result, country coverage within eachregion is not always complete. Expanded country coverage is expected in future editions of the model.In Brazil, the federal postal system has forged an agreement with Banco Bradesco—one of the fourlargest banks in Brazil—to set up and operate banking branches in post offices. In an effort to tap thelarge portion of the population that does not have bank accounts—estimated at some 40m Brazilians—Bradesco launched its Postal Bank project in 2002. It had set up 6,067 outlets in post-office branches byend-2009, up from 5,946 outlets at end-2008.Egypt Post is one of the country’s major savings institutions. Postal savings accounts can be openedfor just E£10, making these accounts an attractive savings method for low-income citizens. Interest onmoney deposited with the postal authority is exempt from tax. Each post office holds an account at theNational Investment Bank (NIB), where customers’ savings are placed. In recent years, Egypt Post hasstarted offering services in competition with the banking sector, such as high-yield deposit accounts,ATMs and payment systems for firms. Additionally, Egypt Post has expanded its physical presence, witharound 3,700 locations.26© <strong>Economist</strong> <strong>Intelligence</strong> <strong>Unit</strong> Limited 2010