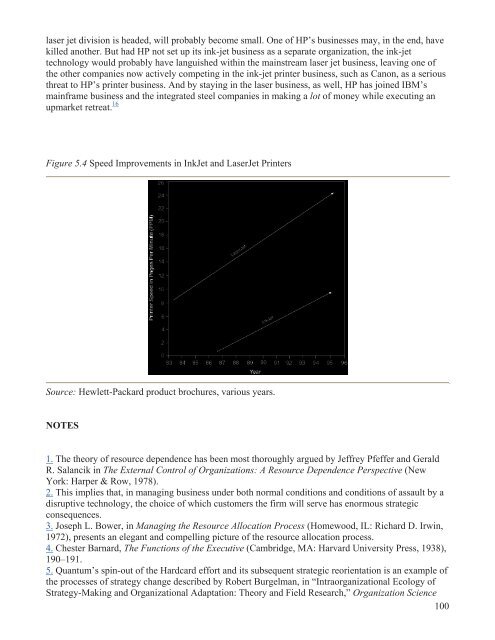

laser jet division is headed, will probably become small. One of HP’s businesses may, in the end, havekilled another. But had HP not set up its ink-jet business as a separate organization, the ink-jettechnology would probably have languished within the mainstream laser jet business, leaving one ofthe other companies now actively competing in the ink-jet printer business, such as Canon, as a seriousthreat to HP’s printer business. And by staying in the laser business, as well, HP has joined IBM’smainframe business and the integrated steel companies in making a lot of money while executing anupmarket retreat. 16Figure 5.4 Speed Improvements in InkJet and LaserJet PrintersSource: Hewlett-Packard product brochures, various years.NOTES1. The theory of resource dependence has been most thoroughly argued by Jeffrey Pfeffer and GeraldR. Salancik in The External Control of Organizations: A Resource Dependence Perspective (NewYork: Harper & Row, 1978).2. This implies that, in managing business under both normal conditions and conditions of assault by adisruptive technology, the choice of which customers the firm will serve has enormous strategicconsequences.3. Joseph L. Bower, in Managing the Resource Allocation Process (Homewood, IL: Richard D. Irwin,1972), presents an elegant and compelling picture of the resource allocation process.4. Chester Barnard, The Functions of the Executive (Cambridge, MA: Harvard University Press, 1938),190–191.5. Quantum’s spin-out of the Hardcard effort and its subsequent strategic reorientation is an example ofthe processes of strategy change described by Robert Burgelman, in “Intraorganizational Ecology ofStrategy-Making and Organizational Adaptation: Theory and Field Research,” Organization Science100

(2), 1991, 239–262, as essentially a process of natural selection through which suboptimal strategicinitiatives lose out to optimal ones in the internal competition for corporate resources.6. The failure of Micropolis to maintain simultaneous competitive commitments to both its establishedtechnology and the new 5.25-inch technology is consistent with the technological histories recountedby James Utterback, in Mastering the Dynamics of Innovation (Boston: Harvard Business School Press,1994). Utterback found that firms that attempted to develop radically new technology almost alwaystried to maintain simultaneous commitment to the old and that they almost always failed.7. A set of industries in which disruptive technologies are believed to have played a role in topplingleading firms is presented by Richard S. Rosenbloom and Clayton M. Christensen in “TechnologicalDiscontinuities, Organizational Capabilities, and Strategic Commitments,” Industrial and CorporateChange (3), 1994, 655–685.8. In the 1990s, DEC finally set up a Personal Computer Division in its attempt to build a significantpersonal computer business. It was not as autonomous from DEC’s mainstream business; however, theQuantum and Control Data spin-outs were. Although DEC set up specific performance metrics for thePC division, it was still held, de facto, to corporate standards for gross margins and revenue growth.9. “Harvard Study on Discount Shoppers,” Discount Merchandiser, September, 1963, 71.10. When this book was being written, Kmart was a crippled company, having been beaten in a gameof strategy and operational excellence by WalMart. Nonetheless, during the preceding two decades,Kmart had been a highly successful retailer, creating extraordinary value for Kresge shareholders.Kmart’s present competitive struggles are unrelated to Kresge’s strategy in meeting the originaldisruptive threat of discounting.11. A detailed contrast between the Woolworth and Kresge approaches to discount retailing can befound in the Harvard Business School teaching case. “The Discount Retailing Revolution in America,”No. 695-081.12. See Robert Drew-Bear, “S. S. Kresge’s Kmarts,” Mass Merchandising: Revolution and Evolution(New York: Fairchild Publications, 1970), 218.13. F. W. Woolworth Company Annual Report, 1981, p. 8.14. “Woolco Gets Lion’s Share of New Space,” Chain Store Age, November, 1972, E27. This was anextraordinarily elegant, rational argument for the consolidation, clearly crafted by a corporate spindoctorextraordinaire. Never mind that no Woolworth stores approached 100,000 square feet in size!15. See, for example, “The Desktop Printer Industry in 1990,” Harvard Business School, Case No. 9-390-173.16. Business historian Richard Tedlow noted that the same dilemma had confronted A&P’s executivesas they deliberated whether to adopt the disruptive supermarket retailing format:The supermarket entrepreneurs competed against A&P not by doing better what A&P was the bestcompany in the world at doing, but by doing something that A&P did not want to do at all. The greatestentrepreneurial failure in this story is Kroger. This company was second in the market, and one of itsown employees (who left to found the world’s first supermarket) knew how to make it first. Krogerexecutives did not listen. Perhaps it was lack of imagination or perhaps, like the executives at A&P,those at Kroger also had too much invested in the standard way of doing business. If the executives atA&P endorsed the supermarket revolution, they were ruining their own distribution system. That iswhy they sat by paralyzed, unable to act until it was almost too late. In the end, A&P had little choice.The company could ruin its own system, or see others do it.See Richard Tedlow, New and Improved: The Story of Mass Marketing in America (Boston: HarvardBusiness School Press, 1996).101

- Page 2 and 3:

TheInnovator’sDilemmaWhen New Tec

- Page 4 and 5:

ContentsIn GratitudeIntroductionPAR

- Page 6 and 7:

Clayton M. ChristensenHarvard Busin

- Page 8 and 9:

Digital Equipment Corporation creat

- Page 10 and 11:

they lose their positions of leader

- Page 12 and 13:

Disruptive Technologies versus Rati

- Page 14 and 15:

understand what has caused those ci

- Page 16 and 17:

Chapter 7 discusses a different app

- Page 18 and 19:

But the electric car is a disruptiv

- Page 20 and 21:

Part OneWHY GREAT COMPANIESCAN FAIL

- Page 22 and 23:

was the size of a large refrigerato

- Page 24 and 25:

To test this hypothesis, I assemble

- Page 26 and 27:

Figure 1.5 describes a sustaining t

- Page 28 and 29:

Source: Data are from various issue

- Page 30 and 31:

Between 1978 and 1980, several entr

- Page 32 and 33:

The 3.5-inch drive was first develo

- Page 34 and 35:

Figure 1.8 Leadership of Entrant Fi

- Page 36 and 37:

Rigid Disk Drive Industry: A Histor

- Page 38 and 39:

CHAPTER TWOValue Networks and theIm

- Page 40 and 41:

toward sustaining innovations and a

- Page 42 and 43:

how each value network exhibits a v

- Page 44 and 45:

structure. Research, engineering, a

- Page 46 and 47:

Figure 2.5 The Conventional Technol

- Page 48 and 49:

firms’ decision-making processes

- Page 50 and 51: annually introduced as a percentage

- Page 52 and 53: ecause they have no moving parts, t

- Page 54 and 55: Figure 2.7 Improvements in Areal De

- Page 56 and 57: IMPLICATIONS OF THE VALUE NETWORK F

- Page 58 and 59: esident in companies today result f

- Page 60 and 61: CHAPTER THREEDisruptive Technologic

- Page 62 and 63: Source: Data are from the Historica

- Page 64 and 65: Because their capacity was so small

- Page 66 and 67: was thus a hybrid of the two techno

- Page 68 and 69: Source: Data are from the Historica

- Page 70 and 71: its archives, and Toth and Haddock

- Page 72 and 73: CHAPTER FOURWhat Goes Up, Can’t G

- Page 74 and 75: challenges of their competitors. Gr

- Page 76 and 77: organization’s middle managers pl

- Page 78 and 79: Managers in disk drive companies we

- Page 80 and 81: Minimill steel making first became

- Page 82 and 83: Once their position in the market f

- Page 84 and 85: Indiana, in 1989, and constructed a

- Page 86 and 87: Part TwoMANAGING DISRUPTIVETECHNOLO

- Page 88 and 89: The sum of these studies is that wh

- Page 90 and 91: want? One option is to convince eve

- Page 92 and 93: engineering workstations, and has a

- Page 94 and 95: those laws, people flew quite succe

- Page 96 and 97: The first discount store was Korvet

- Page 98 and 99: expansion in the regular variety st

- Page 102 and 103: CHAPTER SIXMatch the Size of theOrg

- Page 104 and 105: What benefit, if any, did leadershi

- Page 106 and 107: Source: Data are from various issue

- Page 108 and 109: Finally, there is substantial evide

- Page 110 and 111: Because emerging markets are small

- Page 112 and 113: There are many success stories to t

- Page 114 and 115: This recommendation is not new, of

- Page 116 and 117: 13. “Can 3.5" Drives Displace 5.2

- Page 118 and 119: data, Disk/Trend Report, published

- Page 120 and 121: MB, and a second model, introduced

- Page 122 and 123: to make small deliveries to local c

- Page 124 and 125: Japanese semiconductor manufacturer

- Page 126 and 127: powerful deterrent to the movement

- Page 128 and 129: therefore, may view creation of new

- Page 130 and 131: ResourcesResources are the most vis

- Page 132 and 133: its Corona model—a product target

- Page 134 and 135: go public based upon a hot initial

- Page 136 and 137: such success in the minicomputer bu

- Page 138 and 139: they made these acquisitions late a

- Page 140 and 141: Figure 8.1 Fitting an Innovation’

- Page 142 and 143: structured. For Compaq, Hewlett-Pac

- Page 144 and 145: CHAPTER NINEPerformance Provided,Ma

- Page 146 and 147: Specifically, in the desktop person

- Page 148 and 149: A product becomes a commodity withi

- Page 150 and 151:

1. The Weaknesses of Disruptive Tec

- Page 152 and 153:

Scott Cook, Intuit’s founder, sur

- Page 154 and 155:

CONTROLLING THE EVOLUTION OF PRODUC

- Page 156 and 157:

Source: An earlier version of this

- Page 158 and 159:

originally developed by Venetian me

- Page 160 and 161:

The first step in making this chart

- Page 162 and 163:

Having decided that electric vehicl

- Page 164 and 165:

its braking distance longer than ot

- Page 166 and 167:

The major automakers engaged in ele

- Page 168 and 169:

customers who pay the present bills

- Page 170 and 171:

Clearly, as will be discussed below

- Page 172 and 173:

CHAPTER ELEVENThe Dilemmas of Innov

- Page 174 and 175:

Seventh, and last, the research sum

- Page 176 and 177:

develop those technologies themselv

- Page 178 and 179:

2. There is a tendency in all marke