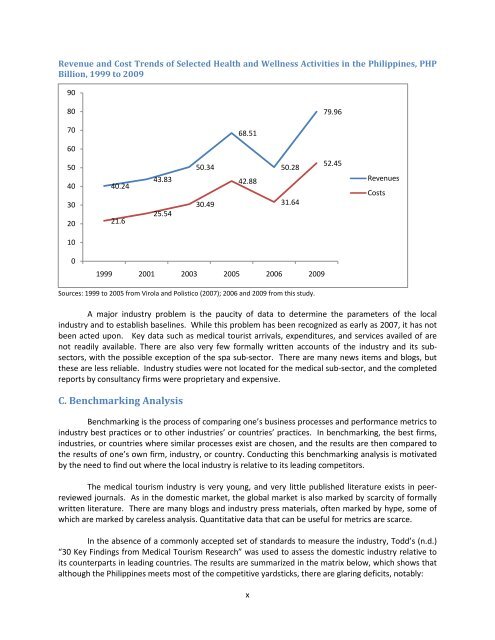

B. The Domestic Industry<strong>Medical</strong> tourism gravitates around 21 premier hospitals <strong>in</strong>cluded under <strong>the</strong> Philipp<strong>in</strong>e <strong>Medical</strong><strong>Tourism</strong> Program (PMTP). The table below shows <strong>the</strong>ir location, ownership, and total number of beds.Hospitals Under <strong>the</strong> Philipp<strong>in</strong>e <strong>Medical</strong> <strong>Tourism</strong> Program, 2013Location Private Public TotalNumber Beds Number Beds Number BedsMetro Manila 11 4,371 5 2,107 16 6,478Batangas Prov<strong>in</strong>ce 1 220 - - 1 220Cebu 3 1,210 - - 3 1,210Davao 1 250 - 1 250Total 16 6,051 5 2,107 21 8,158Source: This studyThe domestic <strong>in</strong>dustry is very price-competitive relative to <strong>the</strong> orig<strong>in</strong>-countries of medicaltourists and relative to its lead<strong>in</strong>g competitors <strong>in</strong> Asia. This is shown <strong>in</strong> <strong>the</strong> table below which comparesPhilipp<strong>in</strong>e prices <strong>for</strong> a sample of procedures with those obta<strong>in</strong><strong>in</strong>g <strong>in</strong> <strong>the</strong> U.S. and Thailand.Comparison of Price Range <strong>for</strong> Sample Procedures <strong>in</strong> <strong>the</strong> Philipp<strong>in</strong>es and <strong>in</strong> <strong>the</strong> U.S. andThailand, <strong>in</strong> US$, Early 2010sProcedures Philipp<strong>in</strong>es U.S. ThailandDental bridge 360 – 600 5,500 290 – 430Lasik eye surgery 1,000 – 1,500 3,000 650 – 900Heart bypass 11,000 – 25,000 90,000 – 144,300 23,000 – 25,000Nose lift 400 – 1,000 4,000 – 12,000 600 – 2,500Spa services 11 - 100 100 - 200 45 - 100Source: HealthCORE (2011)The <strong>in</strong>dustry has also been grow<strong>in</strong>g <strong>for</strong> over a decade, as shown <strong>in</strong> <strong>the</strong> figure below. Except <strong>for</strong>a dip <strong>in</strong> 2006, which probably reflects stalled demand aris<strong>in</strong>g from <strong>the</strong> impend<strong>in</strong>g recession 1 <strong>in</strong> mostWestern countries, health and wellness activities (<strong>in</strong>clusive of domestic and tourist-oriented services)have expanded apace. Specifically, revenues have consistently outpaced costs. The <strong>in</strong>dustry had grossrevenues of about PHP 80 billion <strong>in</strong> 2009, compared to gross costs of about PHP 53 billion.1 It would seem from this observation that medical tourist arrivals and expenses are a lead<strong>in</strong>g economic <strong>in</strong>dicator as householdbehavior signals that <strong>the</strong> economy is go<strong>in</strong>g down. It was not until 2008 that <strong>the</strong> recession <strong>in</strong> <strong>the</strong> U.S. actually hit. Note,however, that <strong>the</strong> <strong>in</strong>dustry bounced quickly back <strong>the</strong> follow<strong>in</strong>g year.ix

Revenue and Cost Trends of Selected Health and Wellness Activities <strong>in</strong> <strong>the</strong> Philipp<strong>in</strong>es, PHPBillion, 1999 to 2009908079.967068.51605040302040.2421.643.8325.5450.3430.4942.8850.2831.6452.45RevenuesCosts1001999 2001 2003 2005 2006 2009Sources: 1999 to 2005 from Virola and Polistico (2007); 2006 and 2009 from this study.A major <strong>in</strong>dustry problem is <strong>the</strong> paucity of data to determ<strong>in</strong>e <strong>the</strong> parameters of <strong>the</strong> local<strong>in</strong>dustry and to establish basel<strong>in</strong>es. While this problem has been recognized as early as 2007, it has notbeen acted upon. Key data such as medical tourist arrivals, expenditures, and services availed of arenot readily available. There are also very few <strong>for</strong>mally written accounts of <strong>the</strong> <strong>in</strong>dustry and its subsectors,with <strong>the</strong> possible exception of <strong>the</strong> spa sub-sector. There are many news items and blogs, but<strong>the</strong>se are less reliable. Industry studies were not located <strong>for</strong> <strong>the</strong> medical sub-sector, and <strong>the</strong> completedreports by consultancy firms were proprietary and expensive.C. Benchmark<strong>in</strong>g AnalysisBenchmark<strong>in</strong>g is <strong>the</strong> process of compar<strong>in</strong>g one’s bus<strong>in</strong>ess processes and per<strong>for</strong>mance metrics to<strong>in</strong>dustry best practices or to o<strong>the</strong>r <strong>in</strong>dustries’ or countries’ practices. In benchmark<strong>in</strong>g, <strong>the</strong> best firms,<strong>in</strong>dustries, or countries where similar processes exist are chosen, and <strong>the</strong> results are <strong>the</strong>n compared to<strong>the</strong> results of one’s own firm, <strong>in</strong>dustry, or country. Conduct<strong>in</strong>g this benchmark<strong>in</strong>g analysis is motivatedby <strong>the</strong> need to f<strong>in</strong>d out where <strong>the</strong> local <strong>in</strong>dustry is relative to its lead<strong>in</strong>g competitors.The medical tourism <strong>in</strong>dustry is very young, and very little published literature exists <strong>in</strong> peerreviewedjournals. As <strong>in</strong> <strong>the</strong> domestic market, <strong>the</strong> global market is also marked by scarcity of <strong>for</strong>mallywritten literature. There are many blogs and <strong>in</strong>dustry press materials, often marked by hype, some ofwhich are marked by careless analysis. Quantitative data that can be useful <strong>for</strong> metrics are scarce.In <strong>the</strong> absence of a commonly accepted set of standards to measure <strong>the</strong> <strong>in</strong>dustry, Todd’s (n.d.)“30 Key F<strong>in</strong>d<strong>in</strong>gs from <strong>Medical</strong> <strong>Tourism</strong> Research” was used to assess <strong>the</strong> domestic <strong>in</strong>dustry relative toits counterparts <strong>in</strong> lead<strong>in</strong>g countries. The results are summarized <strong>in</strong> <strong>the</strong> matrix below, which shows thatalthough <strong>the</strong> Philipp<strong>in</strong>es meets most of <strong>the</strong> competitive yardsticks, <strong>the</strong>re are glar<strong>in</strong>g deficits, notably:x

- Page 3: AbstractMedical Tourism in the Phil

- Page 6 and 7: Table of ContentsAbbreviations and

- Page 8 and 9: List of TablesTable 1. WTO’s Mode

- Page 11: c. Epidemiologically, the disease b

- Page 15 and 16: BenchmarksStatus10 Adoption of “h

- Page 17 and 18: S.W.O.T. Analysis of the Philippine

- Page 19 and 20: Chapter I. Background“Once your t

- Page 21 and 22: Chapter II. The Global Market for M

- Page 23 and 24: A major industry weakness is the ab

- Page 25 and 26: B. Demand, Revenues, and Market Opp

- Page 27 and 28: dermatology, 6.8 weeks; and cardiol

- Page 29 and 30: trends globally since 1990 15 : (1)

- Page 31: Table 5. Top 20 Medical Tourist Des

- Page 34 and 35: Chapter III. Philippine Medical Tou

- Page 36 and 37: f. HealthCORE’s (2011) estimate o

- Page 38 and 39: seek better health care, 15 percent

- Page 40 and 41: Cardinal Santos San Juan City P 197

- Page 42 and 43: sources, bone marrow and peripheral

- Page 44 and 45: found between siblings, but even th

- Page 46 and 47: Zen Institute (medicalspa)Bonifacio

- Page 48 and 49: control the dangers of poorly regul

- Page 50 and 51: American Eye CenterAsian Eye Instit

- Page 52 and 53: Medical andDental PracticesRate (ov

- Page 54 and 55: The benchmarking exercise did not b

- Page 56 and 57: d. Providence Hospital Inc., in Wes

- Page 58 and 59: Patients/Consumers”) with 41 year

- Page 60 and 61: Benchmark #14: Advancement in techn

- Page 62 and 63:

society for Quality in Healthcare a

- Page 64 and 65:

H. Travel and Accommodation Benchma

- Page 66 and 67:

Figure 3. Price Variation Among Sel

- Page 68 and 69:

Chapter VI. S.W.O.T. Analysis“Dev

- Page 70 and 71:

insider noted, “You cannot play i

- Page 72 and 73:

Continued high-cost care in advance

- Page 74 and 75:

“medical complication” (Medical

- Page 76 and 77:

Chapter VII. Conclusions and Next S

- Page 78 and 79:

ReferencesABS-CBN News (2013). Medi

- Page 80 and 81:

De la Cruz, Stef (2012). Is Stem Ce

- Page 82 and 83:

Marsek, P.W. and F. Sharpe (2009).

- Page 84 and 85:

Trade Daegu (2013). Daegu Global Me

- Page 86 and 87:

what have failed, and the means to

- Page 88:

Annex 3: Comments on the Draft Sena