2014/15 Annual Report

pzog4zx

pzog4zx

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

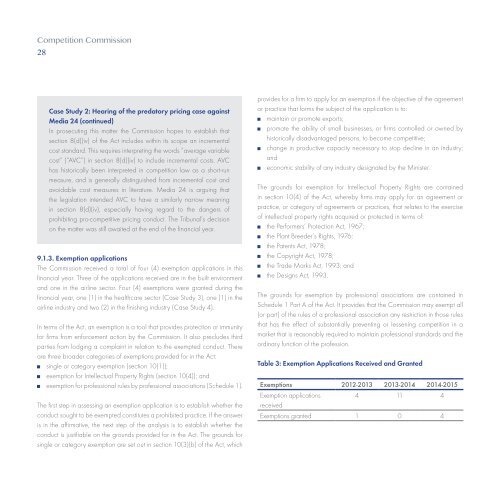

Competition Commission<br />

28<br />

Case Study 2: Hearing of the predatory pricing case against<br />

Media 24 (continued)<br />

In prosecuting this matter the Commission hopes to establish that<br />

section 8(d)(iv) of the Act includes within its scope an incremental<br />

cost standard. This requires interpreting the words “average variable<br />

cost” (“AVC”) in section 8(d)(iv) to include incremental costs. AVC<br />

has historically been interpreted in competition law as a short-run<br />

measure, and is generally distinguished from incremental cost and<br />

avoidable cost measures in literature. Media 24 is arguing that<br />

the legislation intended AVC to have a similarly narrow meaning<br />

in section 8(d)(iv), especially having regard to the dangers of<br />

prohibiting pro-competitive pricing conduct. The Tribunal’s decision<br />

on the matter was still awaited at the end of the financial year.<br />

9.1.3. Exemption applications<br />

The Commission received a total of four (4) exemption applications in this<br />

financial year. Three of the applications received are in the built environment<br />

and one in the airline sector. Four (4) exemptions were granted during the<br />

financial year, one (1) in the healthcare sector (Case Study 3), one (1) in the<br />

airline industry and two (2) in the finishing industry (Case Study 4).<br />

In terms of the Act, an exemption is a tool that provides protection or immunity<br />

for firms from enforcement action by the Commission. It also precludes third<br />

parties from lodging a complaint in relation to the exempted conduct. There<br />

are three broader categories of exemptions provided for in the Act:<br />

single or category exemption (section 10(1));<br />

exemption for Intellectual Property Rights (section 10(4)); and<br />

exemption for professional rules by professional associations (Schedule 1).<br />

The first step in assessing an exemption application is to establish whether the<br />

conduct sought to be exempted constitutes a prohibited practice. If the answer<br />

is in the affirmative, the next step of the analysis is to establish whether the<br />

conduct is justifiable on the grounds provided for in the Act. The grounds for<br />

single or category exemption are set out in section 10(3)(b) of the Act, which<br />

provides for a firm to apply for an exemption if the objective of the agreement<br />

or practice that forms the subject of the application is to:<br />

maintain or promote exports;<br />

promote the ability of small businesses, or firms controlled or owned by<br />

historically disadvantaged persons, to become competitive;<br />

change in productive capacity necessary to stop decline in an industry;<br />

and<br />

economic stability of any industry designated by the Minister.<br />

The grounds for exemption for Intellectual Property Rights are contained<br />

in section 10(4) of the Act, whereby firms may apply for an agreement or<br />

practice, or category of agreements or practices, that relates to the exercise<br />

of intellectual property rights acquired or protected in terms of:<br />

the Performers’ Protection Act, 1967;<br />

the Plant Breeder’s Rights, 1976;<br />

the Patents Act, 1978;<br />

the Copyright Act, 1978;<br />

the Trade Marks Act, 1993; and<br />

the Designs Act, 1993.<br />

The grounds for exemption by professional associations are contained in<br />

Schedule 1 Part A of the Act. It provides that the Commission may exempt all<br />

(or part) of the rules of a professional association any restriction in those rules<br />

that has the effect of substantially preventing or lessening competition in a<br />

market that is reasonably required to maintain professional standards and the<br />

ordinary function of the profession.<br />

Table 3: Exemption Applications Received and Granted<br />

Exemptions 2012-2013 2013-<strong>2014</strong> <strong>2014</strong>-20<strong>15</strong><br />

Exemption applications 4 11 4<br />

received<br />

Exemptions granted 1 0 4