2016 ET CARBON RANKINGS REPORT

2gIpuBS

2gIpuBS

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

26<br />

<strong>CARBON</strong> REDUCTION POTENTIAL<br />

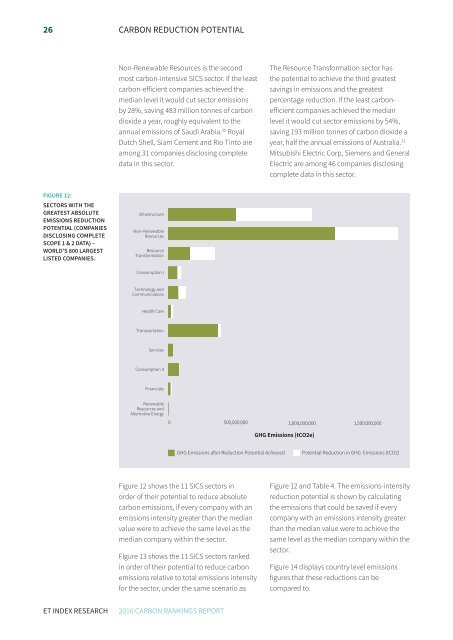

Non-Renewable Resources is the second<br />

most carbon-intensive SICS sector. If the least<br />

carbon-efficient companies achieved the<br />

median level it would cut sector emissions<br />

by 28%, saving 483 million tonnes of carbon<br />

dioxide a year, roughly equivalent to the<br />

annual emissions of Saudi Arabia. 30 Royal<br />

Dutch Shell, Siam Cement and Rio Tinto are<br />

among 31 companies disclosing complete<br />

data in this sector.<br />

The Resource Transformation sector has<br />

the potential to achieve the third greatest<br />

savings in emissions and the greatest<br />

percentage reduction. If the least carbonefficient<br />

companies achieved the median<br />

level it would cut sector emissions by 54%,<br />

saving 193 million tonnes of carbon dioxide a<br />

year, half the annual emissions of Australia. 31<br />

Mitsubishi Electric Corp, Siemens and General<br />

Electric are among 46 companies disclosing<br />

complete data in this sector.<br />

FIGURE 12:<br />

SECTORS WITH THE<br />

GREATEST ABSOLUTE<br />

EMISSIONS REDUCTION<br />

POTENTIAL (COMPANIES<br />

DISCLOSING COMPL<strong>ET</strong>E<br />

SCOPE 1 & 2 DATA) –<br />

WORLD’S 800 LARGEST<br />

LISTED COMPANIES.<br />

Infrastructure<br />

Non−Renewable<br />

Resources<br />

Resource<br />

Transformation<br />

Consumption I<br />

Technology and<br />

Communications<br />

Health Care<br />

Transportation<br />

Services<br />

Consumption II<br />

Financials<br />

Renewable<br />

Resources and<br />

Alternative Energy<br />

0 500,000,000 1,000,000,000 1,500,000,000<br />

GHG Emissions (tCO2e)<br />

GHG Emissions after Reduction Potential Achieved<br />

Potential Reduction in GHG Emissions (tCO2)<br />

Figure 12 shows the 11 SICS sectors in<br />

order of their potential to reduce absolute<br />

carbon emissions, if every company with an<br />

emissions intensity greater than the median<br />

value were to achieve the same level as the<br />

median company within the sector.<br />

FIgure 13 shows the 11 SICS sectors ranked<br />

in order of their potential to reduce carbon<br />

emissions relative to total emissions intensity<br />

for the sector, under the same scenario as<br />

Figure 12 and Table 4. The emissions-intensity<br />

reduction potential is shown by calculating<br />

the emissions that could be saved if every<br />

company with an emissions intensity greater<br />

than the median value were to achieve the<br />

same level as the median company within the<br />

sector.<br />

Figure 14 displays country level emissions<br />

figures that these reductions can be<br />

compared to.<br />

<strong>ET</strong> INDEX RESEARCH<br />

<strong>2016</strong> <strong>CARBON</strong> <strong>RANKINGS</strong> <strong>REPORT</strong>