Debtfree Magazine March 2017

The March 2017 issue of Debtfree Magazine. We discuss if it is possible to have fun while under debt review. We also have articles, news, advice, tips and more.

The March 2017 issue of Debtfree Magazine. We discuss if it is possible to have fun while under debt review. We also have articles, news, advice, tips and more.

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

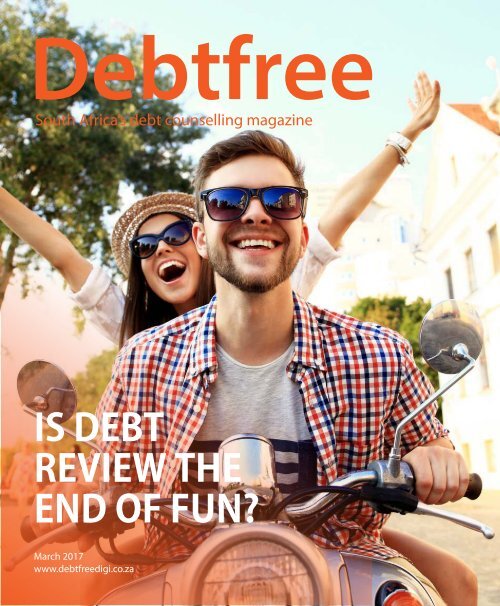

South Africa’s debt counselling magazine<br />

IS DEBT<br />

REVIEW THE<br />

END OF FUN?<br />

<strong>March</strong> <strong>2017</strong><br />

www.debtfreedigi.co.za

What you can expect from Hyphen PDA:<br />

• Increased Debt Counsellor Profitability<br />

• Flawless Systems<br />

• Meaningful Reporting<br />

• Contented Consumers!<br />

www.hyphenpda.co.za<br />

Chris van der Straaten,<br />

Head: PDA<br />

082 557 0437<br />

Malcom Povey,<br />

Head: Operations PDA<br />

082 445 5604

Don’t expect to hear an endless amount<br />

of “spin” around why things failed!.<br />

DEBT<br />

REVIEW<br />

AWARDS<br />

WINNER<br />

PAYMENT<br />

DISTRIBUTION<br />

CUSTOMER<br />

SERVICE<br />

INDUSTRY<br />

SUPPORT<br />

SOFTWARE<br />

INTEgraTION

Debt Review Explained<br />

Let’s be honest. We all spend a little too much occasionally. Maybe<br />

we go a few bucks over the grocery budget or something unexpected<br />

happens that we didn’t plan to pay for. Life happens. But when oncein-a-while<br />

becomes almost-every-time, we end up over-indebted.<br />

How to tell if you’re over indebted?<br />

1. The money you have coming in, simply<br />

isn’t enough to cover all the payments<br />

going out. So you start missing<br />

installments here and there.<br />

2. You’ve probably had one or two calls<br />

from creditors demanding payment.<br />

3. You get that empty pit in your stomach<br />

every time you have to look at your bank<br />

balance.<br />

4. You’re either thinking about or have<br />

already tried going the consolidated<br />

loan root, but that only made your debt<br />

worse, because it didn’t address the core<br />

issue of spending too much.<br />

5. You’re more snappy, because you’re<br />

constantly stressed.<br />

6. Payday can never come too early,<br />

because your bank account is empty<br />

within the first week of the month.<br />

It’s safe to say that if you are experiencing the<br />

above symptoms, you are over-indebted and<br />

a candidate for Debt Counselling.<br />

Debt Counselling! Say what?<br />

Debt counselling or debt review as it’s also<br />

known, is a medium to long-term process<br />

(depending on your level of debt) that<br />

aims to clear your bad debt. This process<br />

can only be done through a qualified<br />

Debt Counsellor. After applying to a Debt<br />

Counselling firm, such as DebtCare, you are<br />

assigned a dedicated Debt Counsellor who<br />

reviews your debt to see how to best assist.<br />

Your DC then looks at your income and<br />

expenses to determine what you can afford<br />

to pay every month. This single minimum<br />

amount covers all your debt repayments.<br />

After this has been determined, your DC<br />

contacts your creditors, informs them that<br />

you are under Debt Review and negotiates<br />

lower payments and interest. Once your<br />

creditors agree, your DC will inform you to<br />

pay the single minimum amount, which<br />

your creditors share amongst each other.<br />

Once your Debt Counselling process is<br />

completed, life goes back to normal. Well<br />

almost. Better spending habits and tighter<br />

reigns on your budget will keep you out of<br />

debt for good!<br />

Watch video at www.debtcare.co.za

EDITOR’S NOTE<br />

All work and no play makes Jack a dull<br />

boy. So the saying goes and this month<br />

we consider if there is any space within<br />

debt review for consumers undergoing<br />

debt counselling to have a little fun. We<br />

know girls just want to have it, we’ve been<br />

welcomed to the house of fun but how can<br />

that work if you are on a tight budget and<br />

paying all your available funds to your<br />

creditors to get out of debt?<br />

We also have some great articles about<br />

going paperless in a digital world. It should<br />

be easy. Right? Well, maybe not that easy, as<br />

you will see in the article. We also get some<br />

good advice in the Nutshell article this<br />

month looking at sticking to good habits<br />

during the Easter season. Interestingly,<br />

this time of year is traditionally a period<br />

where many consumers skip or short pay<br />

their court ordered debt review payments<br />

and fall out of the process. This then puts<br />

them in a worse off financial position. What<br />

a shame. So much wasted time and effort.<br />

If you are having any financial difficulties<br />

please talk to your Debt Counsellor as soon<br />

as you can to get some advice.<br />

We also have a large selection of the<br />

latest news in the industry and a look at<br />

the upcoming industry events. We have<br />

some exciting news from both Consumer<br />

Friend and DC Partner so be sure to look<br />

out for those stories. We also get some<br />

more information about the Annual Debt<br />

Review Awards peer review process which<br />

ramps up in April this year. As our readers<br />

will know the whole <strong>Debtfree</strong> team tries to<br />

help out with the organizing of the process<br />

each year along with other volunteers. So,<br />

we have the inside scoop for you. With<br />

just over 2 months to go until the Debt<br />

Review Awards gala, things are getting<br />

interesting. If you are a credit provider or<br />

Debt Counsellor you will also see how you<br />

can take part this year.<br />

So don’t be a dull boy. Take a few minutes<br />

to have a little fun and read this issue. Why<br />

not have a quick break and a cup of tea or<br />

coffee while you give it a read? We hope this<br />

issue helps you look at debt review in a new<br />

way and to allow yourself to have a little fun<br />

over all the upcoming long weekends and<br />

short weeks. Short weeks make for short<br />

months and before you know it between<br />

all the work, fun and paying off your debts<br />

you could soon be debt free.

don’t be a twit<br />

http://twitter.com/<strong>Debtfree</strong>_DIGI<br />

DISCLAIMER<br />

<strong>Debtfree</strong> <strong>Magazine</strong> considers its sources reliable and verifies as<br />

much information as possible. However, reporting inaccuracies<br />

can occur, consequently readers using this information do so<br />

at their own risk. <strong>Debtfree</strong> <strong>Magazine</strong> makes content available<br />

with the understanding that the publisher is not rendering legal<br />

services or financial advice. Although persons and companies<br />

mentioned herein are believed to be reputable, neither<br />

<strong>Debtfree</strong> <strong>Magazine</strong> nor any of its employees, sales executives<br />

or contributors accept any responsibility whatsoever for their<br />

activities. <strong>Debtfree</strong> <strong>Magazine</strong> contains material supplied to<br />

us by advertisers which does not necessarily reflect the views<br />

and opinions of the <strong>Debtfree</strong> <strong>Magazine</strong> team. No person,<br />

organization or party can copy or re-produce the content<br />

on this site and/or magazine or any part of this publication<br />

without a written consent from the editors’ panel and the<br />

author of the content, as applicable. <strong>Debtfree</strong> <strong>Magazine</strong>,<br />

authors and contributors reserve their rights with regards to<br />

copyright of their work.

CONTENTS<br />

NO MORE FUN?<br />

THE BIG LIE<br />

DEBT REVIEW<br />

AWARDS<br />

NEWS<br />

DEBT OR<br />

WEALTH<br />

SERVICE<br />

DIRECTORY

HAVE SOME FUN<br />

No Money – No Fun<br />

We all enjoy the holidays. Why? Because we get to relax and<br />

have a little fun. One of the things that gets squeezed out,<br />

when we are having financial difficulty is all those fun things<br />

we used to be able to do.<br />

Suddenly, as the cash dries up, so too<br />

does the fun. The worst part is that<br />

when the money dries up and the stress<br />

levels increase this is exactly when a<br />

little fun might help more than ever.<br />

So many of the things we enjoy doing<br />

for fun cost money and when there is no<br />

money for anything then those things<br />

have to fall away. It makes no sense to<br />

head off to the movies with the whole<br />

family and spend hundreds of rand<br />

when there is not enough food on our<br />

plates. Cutting back on unnecessary<br />

things is how we try deal with mounting<br />

debt. Of course, sometimes the debt<br />

simply grows out of control and we<br />

need to get professional help. This is<br />

wise and why the debt review process<br />

was created.<br />

So, what happens when a consumer<br />

who is going through financial strain<br />

approaches a Debt Counsellor for<br />

advice? Is it the end of fun?

Credit ProteCtion – debt review<br />

SuRe SuRe<br />

Applied to go under debt review?<br />

Restructuring your monthly expenses?<br />

why not insure all your accounts on the one Credit Protection?<br />

Credit ProteCtion Credit ProteCtion – debt review – debt review<br />

Applied we will to go contribute under Applied debt towards to review? go under your debt accounts review? in the event of the following:<br />

Restructuring your Restructuring monthly expenses? your monthly expenses?<br />

why • not death insure – why all we your settle not accounts insure the account all on your the accounts one Credit on the Protection? one Credit Protection?<br />

• temporary disability – we pay the Debt Review payment<br />

we will contribute for 6 months we towards will contribute your accounts towards in your the event accounts of the in following: the event of the following:<br />

• Permanent disability – we settle the account<br />

• death • Critical – we settle • illness the death account –– we settle the account<br />

• temporary • retrenchment disability • temporary – we we pay pay disability the the Debt Debt – Review we pay payment the Debt Review payment<br />

for 6 months for 6 months<br />

Review payment for up to 9 months<br />

• Permanent disability • Permanent – we settle disability the account – we settle the account<br />

• Critical illness • – we Critical settle illness the account – we settle the account<br />

• retrenchment At a rate of R • – 2.95 we retrenchment pay per the R1000, Debt – our we pay the Debt<br />

Review rates are payment among for Review up the to best 9 payment months and our for up to 9 months<br />

benefit structure is the best in the<br />

At a rate market. of R 2.95 At per a R1000, rate of R our 2.95 per R1000, our<br />

rates are among the rates best are and among our the best and our<br />

benefit structure is benefit the best structure in the is the best in the<br />

market. market.<br />

ContACt one oR youR<br />

debt Counsellor!<br />

ContACt 0861 one 266 562 oR ContACt youR one oR youR<br />

debt www.one.za.com<br />

Counsellor! debt Counsellor!<br />

0861 266 562 0861 266 562<br />

www.one.za.com<br />

sam Haasbroek: www.one.za.com<br />

082 550 7294<br />

sam Haasbroek: sam Haasbroek:<br />

sam.h@one.za.com<br />

082 550 7294 082 550 7294<br />

sam.h@one.za.com sam.h@one.za.com<br />

marijke wessels:<br />

marijke 082 729 wessels: 3833 marijke wessels:<br />

082 729 marijke.w@one.za.com<br />

3833 082 729 3833<br />

marijke.w@one.za.com marijke.w@one.za.com<br />

terms & Conditions aPPly<br />

terms & Conditions terms aPPly & Conditions aPPly<br />

ONE Insurance ONE Insurance Underwriting Underwriting Managers ONE Insurance (PTY) Managers LTD Underwriting Reg (PTY) No. 1996/008987/07<br />

LTD Managers Reg No. (PTY) 1996/008987/07<br />

LTD Reg No. 1996/008987/07<br />

Underwritten by:<br />

Authorised Financial Services Provider Authorised FSP8783 Financial VAT No. Services 4370160501 Provider FSP8783 VAT No. 4370160501<br />

Authorised Financial Services Provider FSP8783 VAT No. 4370160501<br />

Underwritten Underwritten by: by:<br />

A Member of A Member of A member of the A member of Group the Group<br />

A Member of A member of the Group

HAVE SOME FUN<br />

We Need To Have Fun<br />

Employers will know that happy employees are more productive<br />

and innovative in dealing with challenges that come their way.<br />

Happy employees make for happy clients, which in turn makes<br />

for a better, more profitable business. Parents will know that<br />

their kids are more manageable when they get a chance to<br />

‘let off steam’ and play. Kids love to play and it helps them<br />

to learn and express themselves both of which are greatly<br />

advantageous.<br />

The bottom line is that humans have a<br />

capacity to have fun. It is a built in desire<br />

and ability. While we all enjoy many of<br />

the same activities, each person has<br />

things they particularly like to do for fun.<br />

Obviously, fun needs to be kept in it’s<br />

proper place or it can become addictive<br />

and lead to a totally unproductive<br />

existence. For those who find the<br />

balance, having a little fun can help<br />

greatly reduce stress and improve one’s<br />

overall quality of life. their PDA. Some<br />

consumers even think that the Debt<br />

Counsellor handles their money and<br />

sends them a statement. This is not<br />

true. Either a PDA handles the payment<br />

side of things or the consumer does it<br />

themselves. Debt Counsellors are not<br />

able to take funds from consumers<br />

due to certain Terms & Conditions of<br />

Registration* with the National Credit<br />

Regulator (NCR).

South Africa’s<br />

leading Debt Counsellors<br />

Click through to<br />

www.creditmatters.co.za<br />

or call our national call centre on<br />

086 111 6197

HAVE SOME FUN<br />

THE BIG LIE<br />

Fun Costs Money<br />

We live in a very commercialized world which focuses on<br />

moving money out of your wallet into the hands of business<br />

owners. In fact, we may ourselves, spend all day, every day<br />

convincing others they need our services and should pay for<br />

them. As a result, much of what is considered “fun” these days<br />

costs money.<br />

Speak to an older person and they will tell<br />

you silly stories about how they used to<br />

play with a tyre and stick or homemade<br />

doll and that was all they had growing<br />

up. When compared to the demand for<br />

Playstations, Xbox, the Cartoon Network,<br />

a mini drone or the latest mobile phone,<br />

those things seem archaic and simple.<br />

Worst of all, they may seem boring.<br />

However the reality is that many fun<br />

activities cost very little if you can<br />

drag your head out of the commercial<br />

propaganda all around us. Most will<br />

agree that it is often who you do some<br />

fun activity with that can make or break<br />

the occasion.<br />

This shows us that we enjoy being with<br />

people and friends won’t charge you for<br />

their time. The fact that older ones who<br />

played with simpler items and lived a<br />

less technological life and still had fun<br />

teaches us that gadgets are not needed<br />

to have fun.<br />

Many older ones long back to the days<br />

of their childhood for the simplicity and<br />

fun they were able to have. Watch a<br />

young boy climbing a tree, pretending<br />

to be Spiderman and having fun with his<br />

friends and you will wish you could find<br />

pleasure in such simple fun. The truth is<br />

you can. Having fun does not have to<br />

cost money or a lot of money.

HAVE SOME FUN<br />

Is Debt Review the End of Fun?<br />

Entering Debt Review is admittedly a<br />

big change. A good one but a big one<br />

as it influences so many aspects of your<br />

life not just your debt repayments.<br />

Primarily it is a change from an instant<br />

gratification lifestyle to a more thought<br />

out, planned way of living.<br />

Budgeting is central to the whole<br />

debt review process and when a Debt<br />

Counsellor helps a consumer reevaluate<br />

their monthly spending habits it can be<br />

a little tough at first.<br />

At the same time the Debt Counsellor<br />

strives to be realistic which is an area<br />

some of us struggle with when planning<br />

our monthly finances. They may see<br />

gaps where we are not spending<br />

money like we should. Perhaps they<br />

see a consumer has a vehicle financed<br />

but has neglected to have insurance as<br />

required by the terms and conditions of<br />

their contract with the bank. They may<br />

see we spend lots of money on snacks<br />

at work but have not set money aside<br />

for our kid’s school clothes and books in<br />

January next year.<br />

A good Debt Counsellor balances the<br />

needs of both creditors and consumer.<br />

So, he may cut some of the money we<br />

previously used for fun out of the budget.<br />

Here it is important to remember though<br />

that fun does not have to cost lots of<br />

money. We may simply need to think a<br />

little differently about the topic.

HAVE SOME FUN<br />

Have Some Fun<br />

If you are under debt review or experiencing debt stress then<br />

you might want to consider some ways to have fun that don’t<br />

cost and arm and a leg. Alternatively you may want to slowly<br />

save up funds each month to do something that costs a little.

HAVE SOME FUN<br />

Free Stuff<br />

Many stores hand out loyalty cards<br />

which can be filled for free over time IF<br />

you are sneaky and patient.<br />

Does your company send you out for<br />

lunch? Does the shop you visit give you<br />

stickers or stamps when you go there?<br />

Can you ask your friends for their stickers,<br />

points or stamps?<br />

You will find that getting the stamps<br />

will soon be half the fun and the free<br />

smoothy or coffee is just the cherry on<br />

top.<br />

Many companies like Vida e Café and<br />

the Table Mountain Cable Car will also<br />

give you free stuff on your birthday.<br />

Head over to the library and enjoy<br />

online access or a good read (a small<br />

membership fee may apply).<br />

Things like soccer, frisbee or cricket<br />

can be enjoyed as long as one of your<br />

friends has a ball and bat or similar items.<br />

Getting the team together once a week<br />

on the weekend can be a great stress<br />

reliever and a lot of fun.

HAVE SOME FUN<br />

Free Stuff Online<br />

Free Stuff<br />

If you have access to the internet and<br />

have budgeted for it with your Debt<br />

Counsellor, you can also find many free<br />

things online. Many have enjoyed the<br />

numerous free resources of books that<br />

can be read, music that can be listened<br />

to or games that can be played. Often<br />

they are slightly older which is normally<br />

convenient since you will not need the<br />

latest and most expensive technology<br />

to enjoy them.<br />

A lot of parents panic at the prospect of<br />

perhaps having to cancel their satelite<br />

TV in an effort to save funds. Well if<br />

you have web access you will find that<br />

children enjoy watching Youtube videos<br />

as much as they would a pay tv cartoon<br />

channel. Many of the shows are also<br />

educational like Pancake Manor.

MELIORLEAF WON’T<br />

LOAD YOUR PREMIUMS<br />

OR REPUDIATE A<br />

LEGITIMATE CLAIM<br />

Specialist insurance for people in debt<br />

review. Ask your debt counsellor.<br />

CALL US NOW 0861 635 467<br />

www.meliorleaf.co.za

HAVE SOME FUN<br />

Get Fit<br />

Being fit and healthy is a great form of<br />

having fun. Sure it takes a little sweat<br />

but it is worth it. You see people across<br />

the country streaming to gyms. These<br />

facilities offer convenience and the<br />

latest equipment at a cost.<br />

It is important to realize though, that<br />

many forms of exercise can be engaged<br />

in for free (or very little expense). A lot of<br />

the time, you just need a safe place to<br />

work out. Why not ask a group of your<br />

friends if they would like to go for a jog,<br />

as a group or a cycle together. Ask the<br />

girls to come around to try those Kayla<br />

exercises or a pilates session.<br />

The guys can dig in the back of the<br />

cupboard or their friend’s garage to find<br />

some old free weights that were starting<br />

to rust. It might be time to finally use<br />

those workout gadgets you couldn’t<br />

help yourself from buying a few years<br />

back. Who knows? They may even work.<br />

Cross fit has become a popular form of<br />

exercise recently but if you think about<br />

it, it seems to revolve around working<br />

out without all that fancy equipment.<br />

No, you don’t need to go buy a tractor<br />

tyre to do cross fit and you don’t need<br />

to spend lots of money to get in shape.

HAVE SOME FUN<br />

Nature<br />

There is a wide world out there.<br />

Sometimes we just get so busy we<br />

never get to see it. There are beautiful<br />

mountains, forests, rivers, waterfalls and<br />

even some of the world’s best beachs.<br />

Why not get a group of friends together<br />

and explore nature. Some areas have<br />

fantastic day hikes which can be enjoyed<br />

even in your old takkies (don’t fall into<br />

the “I need to shop for new boots” pitfall).<br />

Season dependent you may be able to<br />

head to the ocean for a swim or perhaps<br />

your local swimming pool. A little fresh<br />

and and sunshine can go a long way to<br />

putting you in a good mood.

HAVE SOME FUN<br />

Spend Wisely<br />

Not all fun can be had without spending.<br />

Some activities are just too expensive.<br />

This means that some things will not<br />

be possible. Goodbye helicopter-ridebungee-jumping.<br />

However with some<br />

saving you may find you have a little<br />

cash on hand which might be used for<br />

something fun. You may find that there<br />

are other less extravagant options that<br />

you can engage in with a minimum<br />

spend. With some careful budgeting and<br />

shopping each month you may be able<br />

to set some funds aside for something<br />

special. You may want to occasionally<br />

spoil yourself, your partner or your kids<br />

without going over the top.<br />

Some restaurants offer two burgers for<br />

the price of one or a wacky special on<br />

certain foods on certain days. With some<br />

saving and good planning you can take<br />

advantage of these specials and not go<br />

overboard when you do what to splash<br />

out a little. The key here is restraint.<br />

Certain restaurants offer such large<br />

portions that two people can share on<br />

meal (try Eastern Food Bizarre in the<br />

Cape Town CBD). It takes keeping an eye<br />

out and watching your spend.

The Aquarium<br />

Some cities, like Cape Town, have<br />

an aquarium which is both fun and<br />

educational for kids and adults alike.<br />

Let’s be honest who does love Nemo<br />

and his friend? Fish are our Friends. The<br />

Two Oceans Aquarium offers a 10%<br />

discount to those who book online.<br />

Pensioners qualify for discounts as well.<br />

If you plan to take your kids regularly<br />

throughout the year, you could explore<br />

their membership option. For the price<br />

of 3 visits members get unlimited access<br />

through the year. IF you have saved for<br />

it and if this will be one of your main<br />

activities then it is worth investigating.<br />

Movie Night<br />

While it is certainly cheaper to enjoy TV or<br />

a movie at home, you may occasionally<br />

want to head out on date night to the<br />

movies or catch that ‘must be seen<br />

on the big screen’ movie. Well, if you<br />

belong to certain insurance providers or<br />

other loyalty programmes you probably<br />

can also get discounted movie tickets<br />

for those movies which just have to be<br />

seen on the big screen. This takes good<br />

planning and self control as they might<br />

give you a cheap ticket hoping you will<br />

blow your money on the snack. You<br />

have been warned!

Is Debt Review the End of Fun?<br />

Yoda dog says:<br />

NO<br />

Debt Review does force us to re-evaluate<br />

how much money we spend to do some<br />

fun activities. But with a little saving and<br />

cunning there is a world of fun out there.<br />

From chilling by the fire and reading a<br />

book to just getting together with your<br />

friends with some popcorn and a movie<br />

(they bring the movie) you can have a<br />

good time without spending lots of<br />

money. In fact, saving money while still<br />

having fun can be very satisfying. So go<br />

get fit, go play some sport and get out<br />

there for some fresh air. Take the kids to<br />

the park to play or to the beach to build<br />

sandcastles. Blow off some steam. Have<br />

some fun.<br />

Have some fun.<br />

You deserve it.

CALL FOR SOUTH AFRICANS<br />

TO CONTROL THEIR DEBT AND<br />

STICK TO A BUDGET<br />

South Africans are more cash-strapped than ever. A slumping<br />

local economy, paired with a downturn on the global commodity<br />

price cycle; a vicious drought; and increasing interventionist<br />

economic policies are just a few of the issues that have<br />

contributed to growing high household debt burdens and rising<br />

debt service costs. Statistics from the National Credit Regulator<br />

show that up to 10 million South Africans are severely<br />

in arrears on their debt and would greatly benefit from debt<br />

counselling.<br />

“According to a World Bank report in<br />

2015, we live in the most indebted<br />

country on the planet. And it doesn’t<br />

look like things are going to turn<br />

around any time soon. Millions of people<br />

are at the end of their rope. Enough<br />

is enough. As a nation, we are drowning<br />

in debt,” explained Ian Wason, CEO<br />

of DebtBusters.<br />

“It is very easy to get into debt on your<br />

own, but almost impossible to get out<br />

of debt on your own. We know that<br />

many South African consumers often<br />

have little understanding of how they<br />

got into this situation and how to get<br />

out. We see that the majority of searches<br />

on Google are for consolidation<br />

loans, not for debt counselling. People<br />

need to know that there are ways to<br />

get out of their debt. We are reaching<br />

out to South Africans to help them do<br />

something before it gets out of control,”<br />

he continued.<br />

DebtBusters’ new TV ad shows how<br />

easy it is to fall into debt, which can feel<br />

overwhelming, but that it is possible

to take control of the situation and get<br />

back on track. The ad portrays the burden<br />

of debt and the anxiety it invokes<br />

in people, and follows a man living with<br />

the constant stress felt by the indebted<br />

while maintaining the semblance of<br />

normality. It shows a number of different<br />

kinds of people that are suffering<br />

from out-of-control debt. It shows that<br />

everyone, to some extent, suffers from<br />

debt, and that many people have debt<br />

that they hide from others. However,<br />

those that are smart about it, can manage<br />

it.<br />

“We wanted to look at the real stories<br />

of real people and how they have been<br />

affected by debt. We want people to<br />

know that there is a way out. We are<br />

here to help,” finished Wason.<br />

Wason believes firmly in giving people<br />

a second chance at a brighter financial<br />

future: “Over the course of the past<br />

five to ten years, rising food and petrol<br />

prices, a weakened Rand and rising<br />

interest rates have hit consumers’<br />

pockets so hard that entering into a<br />

personal loan agreement has become<br />

a commonplace solution to making<br />

ends meet. Unfortunately, this has led<br />

to a crippling debt spiral. But it doesn’t<br />

need to be like this, which is why we<br />

are determined to do everything we<br />

can to help,” says Wason.<br />

DebtBusters believes in giving South<br />

African consumers a second chance to<br />

build a brighter financial future - there<br />

is life after debt. In order to achieve<br />

financial freedom after debt review,<br />

successful planning and budgeting is<br />

required. Millions of South Africans are<br />

battling to stick to a budget, and at<br />

month end consumers often resort to<br />

taking out more debt to supplement<br />

their income, even using expensive<br />

short-term debt to pay for basic living<br />

expenses. To ensure that you do<br />

not find yourself in this financial stress<br />

you need to set up a monthly budget,<br />

which is closely monitored and followed.<br />

Drawing up a budget requires<br />

a lot of discipline, and even more discipline<br />

is needed to adhere to it. Sticking<br />

to your budget will assist in tracking<br />

spending, planning and debt management,<br />

and will enable you to enjoy a<br />

debt free life.<br />

Managing debt is an essential skill in<br />

today’s financial world. We all have a<br />

responsibility to ensure that we do not<br />

become part of the problem but rather<br />

part of the solution. In an age where<br />

economic conditions are deteriorating,<br />

responsible debt management is essential<br />

for a brighter financial future.<br />

To see DebtBusters’ TV ad: https://www.youtube.com/watch?v=ClbSdtsWxiM

INDUSTRY<br />

CONSUMER<br />

NEWS FLASH<br />

For daily debt counselling news in 3 minutes or less visit www.debtfreedigi.co.za<br />

NCR Takes Wesbank to<br />

the National Consumer<br />

Tribunal<br />

The National Credit Regulator (NCR)<br />

has referred Wesbank to the National<br />

Consumer Tribunal (NCT) for what it<br />

sees as breaches of the National Credit<br />

Act (NCA). The case revolves around<br />

collections practices by Wesbank’s<br />

agents who the NCR say have been<br />

sneakily coercing consumers into<br />

handing over their car keys when in<br />

arrears.<br />

The case followed an NCR investigation<br />

into Wesbank’s debt collection practices.<br />

While it is totally legal for a consumer<br />

to decide to surrender goods that they<br />

have purchased and for these goods to<br />

then be sold (or stored and later once<br />

the arrears are paid up returned) this<br />

needs to be the consumer’s decision.<br />

Jacqueline Peters, NCR manager<br />

investigations and enforcement<br />

says that this right is usually used in<br />

connection with “motor vehicles that<br />

are bought under installment sale<br />

agreements which can be returned<br />

voluntarily by defaulting consumers to<br />

credit providers”. Alternatively, where<br />

consumers do not wish to hand over the<br />

vehicle, credit providers are able take<br />

legal action to enforce their rights.<br />

When this happens the credit provider<br />

can eventually send the dreaded sheriff<br />

of the court to repossess the goods. They<br />

are only able to do this after certain legal<br />

steps have first been taken. Such steps<br />

include the bank sending a Section<br />

129 letter suggesting debt review or<br />

settling the arrears, after some time a<br />

summons, then getting a court order<br />

and a ultimately warrant. After that they<br />

need to send out the sheriff to serve the<br />

warrant. This takes time and needs to<br />

follow a precise order of events.<br />

Peters says that: “The investigation…<br />

revealed that Wesbank, through its debt<br />

collection agents, coaxed defaulting<br />

consumers into relinquishing possession<br />

of their motor vehicles”. It seems,<br />

that they got consumers to surrender<br />

their vehicles in a way that made the<br />

consumers think they absolutely had<br />

to hand over the vehicle to collections<br />

agents when, in fact, they had a choice<br />

not to. Pointing to the issue Peters<br />

continues: “This procedure undermines<br />

the voluntary nature of the surrender

NEWS CONTINUED<br />

process”. It also keeps consumers from<br />

exercising their other rights under the<br />

National Credit Act.<br />

The NCR remind consumers that when<br />

they default on their vehicle payments<br />

they should consider the suggestion<br />

made in the Section 129 demand letter.<br />

Mz Peters says: “The consumer also has<br />

the right to apply for debt review” and<br />

that consumers should be aware that<br />

“a credit provider can only repossess<br />

a motor vehicle from the consumer if<br />

there is a court order authorising the<br />

credit provider to do so”. Consumers<br />

should not believe just anyone who<br />

comes along, claiming to be from a<br />

credit provider, saying they “have” to<br />

give their car back because they have<br />

some mysterious papers showing the<br />

consumer is in arrears even if they look<br />

like legal documents. Consumers in<br />

this situation should feel free to take<br />

video on their phone of these so called<br />

collections agents and send them away,<br />

if they wish. They should then be swift to<br />

contact their creditor to make payment<br />

arrangements or contact their local Debt<br />

Counsellor.<br />

NCT Hand out R180 00 fines<br />

to Two Debt Counselling<br />

Firms<br />

Many years ago, when a credit provider<br />

took advantage of a paperwork mixup<br />

between two Debt Counsellors, the<br />

consumer involved came under a lot<br />

of pressure and made some decisions<br />

which later left them unhappy. This lead<br />

to the consumer eventually complaining<br />

to the National Credit Regulator (NCR).<br />

The cause of many of the problems in the<br />

matter began with how Debt Counsellors<br />

used to try transfer consumers from<br />

one Debt Counsellor to another Debt<br />

Counsellor, back in the day, using the<br />

17.4 form. This was the norm many<br />

years ago when debt review was in it’s<br />

infancy. The entire transfer process only<br />

recently became more defined with<br />

some additional industry-created forms<br />

now being commonly used (a 17.4 is no<br />

longer one of them) but admittedly the<br />

transfer process still remains somewhat<br />

problematic. Seeing a gap, caused by<br />

how the paperwork was handled, the<br />

credit provider decided to go after the<br />

consumer rather than continue to help<br />

through debt review.<br />

After looking over the complaint, the<br />

NCR took the matter to the NCT asking<br />

for fines and that the Debt Counsellors<br />

be deregistered. The NCT did not feel<br />

that deregistration was an option but<br />

did hand down fines to three individuals.<br />

The fines totaled R180 000 between<br />

the three individuals involved - two<br />

of whom are Debt Counsellors. Two<br />

issues came to light in the case. Firstly,<br />

that it is important for a consumer to

NEWS CONTINUED<br />

know exactly who their registered Debt<br />

Counsellor is even when they deal with<br />

multiple Debt Counsellors at the same<br />

firm. They should also not be confused<br />

about the status of anyone just assisting<br />

Debt Counsellors. The second issue<br />

raised, is that Debt Counsellors must be<br />

careful not to allow others to act on their<br />

behalf and should ensure they only sign<br />

forms they are fully aware of.<br />

DC Partner Announce<br />

Exciting Event<br />

Payment Distribution Agency DC Partner<br />

will be hosting a full day seminar for<br />

Debt Counsellors and related industry<br />

members on the 11th of May <strong>2017</strong>, in the<br />

Western Cape. The seminar will feature<br />

several speakers and presentations on<br />

industry related matters during the full<br />

day event which will be hosted at the<br />

Stellenrust Wine Estate in Stellenbosch,<br />

Cape Town. For more info, head over to<br />

their website.<br />

year, had handed in retrenchment letters<br />

as supporting documents along with<br />

their request. Consumers in this situation<br />

can also often claim fromt heir credit<br />

insurance which will cover minimum<br />

monthly repayments for several months<br />

while they search for new work. It has<br />

been a hard year for most consumers in<br />

the country and many businesses have<br />

suffered. Capitec however, took on an<br />

amazing 1.3 million new clients this past<br />

financial year and opened another 76<br />

new stores.<br />

Consumer Friend<br />

Announce Roadshow<br />

Consumer Friend represents multiple<br />

credit providers in the debt review<br />

space. They work closely with Debt<br />

Counsellors each day to facilitate debt<br />

restructuring for consumers. Consumer<br />

Friend have been active in the industry<br />

for a long time and have taken a<br />

number of awards over the years at the<br />

Annual Debt Review Awards. Recently,<br />

Capitec Clients Feeling<br />

the Pinch<br />

A depressed economy is hitting clients<br />

of Capitec hard as the bank reports that<br />

the number of their clients applying for<br />

debt review during the past financial<br />

year increased by 20%. Capitec report<br />

that 15% more clients than the previous<br />

For daily debt<br />

counselling news in 3<br />

minutes or less visit<br />

www.debtfreedigi.co.za

NEWS CONTINUED<br />

Consumer Friend announced that they<br />

will be traveling the country with a<br />

roadshow aimed at Debt Counsellors.<br />

The roadshow will start on the 11th of<br />

May in Bloemfontein, before heading to<br />

Stellenbosch on the 15th &16th. Next<br />

they are off to PE on the 18th &19th<br />

before heading to Jo’burg for the 22nd &<br />

23rd. Their country tour ends in Durban<br />

on the 25th of May. They are currently<br />

inviting all Debt Counsellors to let them<br />

know if they would like to attend. There<br />

are rumors of an exciting launch that<br />

could change the way debt review is<br />

done.<br />

FNB Launch Campaign To<br />

Educate 11 000 Branch<br />

Staff<br />

Debt Counsellors and consumers<br />

often find that when they talk to bank<br />

staff at a branch level they are not as<br />

knowledgeable about the debt review<br />

process as the specialized debt review<br />

departments within the banks. This is one<br />

of the reasons why FNB have launched a<br />

campaign to educate over 11000 branch<br />

staff about how debt review works and<br />

what to do when dealing with a client<br />

who is undergoing debt review. At a<br />

recent workshop with FNB in Gauteng,<br />

Debt Counsellors asked that the training<br />

also cover the often contentious issue of<br />

debit order cancellation.<br />

NCR Transfers Backlog<br />

At the recent NCR workshop the NCR<br />

discussed the challenges surrounding<br />

the long time it takes for consumers to<br />

be transferred from one Debt Counsellor<br />

on their website data base to another.<br />

The reported that due to high amounts<br />

of backlog in 2016 many in the office<br />

had to stop doing their regular work<br />

and assist with transfers. This drive<br />

apparently lowered the backlog from<br />

9000 requests to only 2000. However,<br />

after the drive, once things went back to<br />

normal, so the number of request began<br />

to grow again. Currently the request<br />

list is somewhere back up around 9000<br />

names long.<br />

ABSA Debt Review Centre<br />

Begin New Training<br />

As of <strong>March</strong>, the ABSA debt review centre<br />

will be holding weekly training sessions<br />

with staff on Monday afternoons. As a<br />

result they are closing their call center<br />

slightly early on Mondays at 3:30pm.<br />

They ask that Debt Counsellors keep it<br />

in mind when trying to make contact.<br />

Eagle Cash Loans Shut<br />

Down<br />

After an NCR investigation into claims<br />

of reckless lending and contraventions<br />

of the National credit Act, the National

All professionals have professional indemnity if the unforeseen<br />

happens. Do you as a professional Debt Counselor have<br />

professional indemnity as stipulated by the ethical code?<br />

contact us today for more information<br />

086 111 2882<br />

Telephone 0861 112 882 Facsimile 086 605 9751 Mobile 082 449 6856 EMAIL andre@in2insurance.co.za<br />

www.in2insurance.co.za<br />

don’t be a twit<br />

http://twitter.com/<strong>Debtfree</strong>_DIGI

NEWS CONTINUED<br />

Consumer Tribunal (NCT) has ordered<br />

the deregistration of Eagle Cash Loans.<br />

The NCR investigation found that not<br />

only was the creditor recklessly lending<br />

to those who could not afford to repay<br />

the loans, they were also taking peoples<br />

IDs and Bank cards. This is illegal. As a<br />

result the NCT also handed down a R250<br />

000 fine.<br />

Loan Sharks Ordered To<br />

Register<br />

The NCR recently took 6 unregistered<br />

credit providers to task for lending<br />

money for profit without having<br />

registered with them as required by law.<br />

Changes to the National Credit Act now<br />

mean that there is no minimum amount<br />

that one has to loan or minimum amount<br />

of clients before a person or business<br />

needs to register as a credit provider,<br />

if they charge fees or interest on loans.<br />

The 6 unregistered credit providers have<br />

been given a short time to comply and<br />

register.<br />

Relief For Some In R699<br />

Scheme<br />

When the R699/Satinsky car advertising<br />

deal fell through, thousands of consumers<br />

were affected. When their monthly<br />

car repayment premiums suddenly<br />

shot up and they could not afford to<br />

make payments, the creditors began<br />

to contemplate repossessing vehicles.<br />

At the same time Debt Counsellors,<br />

Politicians, consumer rights activists<br />

and those affected began to ask if they<br />

had been victims of reckless lending.<br />

The NCR launched an investigation into<br />

some of the cases (it seems around 70 of<br />

the thousands of matters) and recently<br />

came to an agreement with ABSA. ABSA<br />

have agreed to pay a R10 Million fine<br />

and to come to an arrangement with<br />

the affected consumers, which will<br />

enable them to retain their vehicles and<br />

make manageable repayments each<br />

month. Though this is a small victory<br />

and will greatly assist these consumers,<br />

the public are asking is the fine enough,<br />

what happens to the other creditors and<br />

consumers? The NCR have said that they<br />

intend to lodge a case against Satinsky.<br />

Debt Review Awards Gala<br />

Date Announced<br />

The date of the <strong>2017</strong> annual Debt Review<br />

Awards gala has been announced by<br />

the organisers. This year the event will<br />

happen in Gauteng on the evening<br />

of the 10th of June <strong>2017</strong>. Attendance<br />

at the red carpet event is by invitation<br />

only. The event sees the results of the<br />

industry peer review announced and<br />

Golden Piggy banks awarded to Debt<br />

Counsellors, Credit Providers and PDAs.

SIGN UP TO BE CONSIDERED FOR THE<br />

<strong>2017</strong> Debt Review Awards<br />

CLICK HERE TO REGISTER

Debt Review Awards<br />

Peer Review<br />

The annual Debt Review Awards peer review process has been<br />

underway for a little while and ramps up drastically during<br />

April and May. During this time, many credit providers and<br />

Debt Counsellors will get to review how the other side of the<br />

industry is doing.<br />

This involves clicking on a few buttons online regarding various facets of the debt<br />

review process and the recent performance of various industry role players. By<br />

getting many different individual firms to participate, a global opinion is formed<br />

as information from all those who participate is collected on the backend database<br />

attached to the peer review. Every peer review matters and we are inviting all<br />

Debt Counsellors and Credit Providers to participate. Why not help promote good<br />

business practice through the peer review process?<br />

Be A Winner<br />

We also invite you to be eligible to win Awards by registering:<br />

If you do not register participants may still review you but you may not be eligible<br />

for an award at the Awards Gala which will be held on the 10th of June <strong>2017</strong><br />

CLICK HERE TO REGISTER

IN A NUTSHELL<br />

Increasing Debt or<br />

Building Wealth<br />

during the holidays?<br />

The months of <strong>March</strong> and April are characterised by the number of<br />

public holidays. This is something to look forward to if you’ve planned<br />

to take leave over this period and take advantage of this benefit.<br />

However, during holiday periods consumers tend to ignore their debt<br />

obligations, aggravating their financial burden.<br />

As a Debt Counsellor, it may be<br />

worthwhile to remind your consumers<br />

to exercise caution during these months.<br />

Holiday periods tend to illicit ‘false<br />

bubbles’ of consumer confidence, which<br />

lead to overspending. Overindebted<br />

consumers need to develop good<br />

money management habits, which will<br />

ultimately shift them from the state of<br />

overindebtedness into a state of wealth<br />

building.<br />

Stick with your good habits<br />

The challenge with holiday periods

is that good habits, particularly those<br />

associated with money management<br />

can change. The Merriam-Webster<br />

dictionary defines a ‘habit’ as “a usual way<br />

of behaving: something that a person<br />

does often in a regular and repeated<br />

way.” Changing your habits during the<br />

holidays not only affects behaviour at<br />

that time, but the risk is that it continues<br />

long after the holidays are over.<br />

Plan ahead, this may seem obvious, but<br />

are you planning for what you can afford<br />

rather than what is desirable?<br />

Plan ahead<br />

Get your kids involved and make handmade<br />

gifts during this time of year,<br />

for example, your own hand-made<br />

chocolate gifts for Easter. Commit to<br />

only ‘spoiling the children’.<br />

Prepare homemade meals and limit the<br />

high cost of ‘eating out’. If you planning<br />

day trips pack some snacks or a family<br />

lunch box. Picnics can be cost effective<br />

family fun filled days.<br />

The holidays and Easter period are a good<br />

opportunity to get the family together.<br />

Share the financial responsibility and<br />

ask people to help contribute towards<br />

the meal, either drinks or a dessert.<br />

Avoid the malls over this time of year. If<br />

you have to shop, go with a list and a<br />

defined budget and don’t get swayed by<br />

all the tempting specials and advertising.<br />

Leave your credit cards at home, take enough cash to get you through the day.<br />

This will eliminate the temptation to overspend. The process of planning, being<br />

creative, and making good memories, is a wise approach to the upcoming holiday<br />

period.<br />

IN A NUTSHELL is brought you by the DCM Business Partnership Programme, designed to<br />

support debt counsellors and consumers during the debt review process, in collaboration with<br />

the National Payment Distribution Agency (NPDA). For help, contact the NPDA on 0861 628 628.<br />

If you have suggestions for topics that you would like covered in future, please email info@dcmgroup.co.za<br />

Debt Review Awards Winner 2014 and 2015:<br />

NPDA: Payment Distribution; Client & Customer Service; Industry Support & Engagement<br />

Care Premier: Debt Counselling Software

AND THE<br />

WINNER IS...<br />

Announcing the Winners<br />

of DCM’s annual DC competition<br />

Debt Counsellors were selected<br />

based on their achievement across<br />

the following three categories<br />

relative to their business size:<br />

1. Number of new applications<br />

2. Conversion rate of new applications<br />

3. Churn rate<br />

Congratulations to the three<br />

winners of an exotic holiday:<br />

Zerodebt: Chris Craven<br />

NCDS & Solutions T/A Debtcare: Cadle Odendaal<br />

Help U Debt Counsellors CC: Belinda Driskel

Professional Debt<br />

Counselling Attorneys<br />

Tel: 021 872 1968<br />

11 MARKET STREET, PAARL<br />

www.steyncoetzee.co.za

The cost of<br />

printing and paper<br />

The cost of printing and paper is a major part of most Debt<br />

Counselling firms’ overheads and the smaller the firm the bigger<br />

the overhead.<br />

In 1999 Bill Gates said “The paperless office, like artificial intelligence, is one of those ‘any<br />

day now’ phenomena that somehow never seem to actually arrive.” 18 years later in <strong>2017</strong><br />

this is still largely true and we have to ask ourselves why. There are two reasons – human<br />

and technological.<br />

HUMAN<br />

Here’s the truth. I have owned a tablet for nearly six years now. I confidently use it to<br />

get stuff off the internet and even to do my banking and yet I still get my Sunday Times<br />

delivered every week and I still go to the bookshop to buy books. The reason? Well actually<br />

I like spreading the paper out and I like the smell and feel of the book in my hand. It is<br />

familiar and it is comfortable, so why would I want to read on a piece of technology even<br />

if it is better?<br />

This is called resistance to change, the natural instinct to stay with what is comfortable<br />

and is the number one stumbling block to getting rid of the paper.<br />

Technology<br />

There are a number of technical issues that have stood in the way of the realisation of<br />

digital offices. These centre around the quality of the document image of a scanned<br />

document, the concern about the ease at which am electronic document can be

tampered with and the storage space required to hold the documents, as well as<br />

the security of the documents themselves. And how do you get a signature onto an<br />

electronic document?<br />

The Paperless<br />

Debt Counselling Practice<br />

In order to implement the paperless office a Debt Counsellor needs to make a firm<br />

commitment to getting rid of the paper. Look at the office and see where paper is been<br />

produced unnecessarily and then seek ways to eliminate it. Staff can be offered incentives<br />

for not printing documents and in time the comfortable habits will break.<br />

Needless to say, the technology needs to be right to support the paperless office and this<br />

is where Maximus comes in. Maximus produces and stores all documents necessary to do<br />

the Debt Review. These documents need never be printed except for the Courts. Good<br />

news is that Maximus will also cater for digital signatures pretty soon.<br />

This means that consumers will be able to sign docuemnts without them ever having<br />

been printed – and that signature is admissible in Court! A digitally signed document<br />

cannot be tampered with and the signature is as good if not better than an ink on paper<br />

one. Storage is not a problem as Maximus stores all documents automatically and securely<br />

in the cloud.<br />

Maximus always stays on the forefront of technology to help<br />

Debt Counsellors work quicker, smatter and better.<br />

Till next time<br />

Max<br />

Next month we look at the information<br />

you need to run a successful practice.<br />

Contact Maximus on 011 451 0041

Die Republiek van<br />

SKYT AFRICA<br />

‘N maand is verby en danksy julle ondersteuning en positiewe<br />

kommentaar is ons nog steeds aan die gang. As daar spel foute<br />

was blameer die redakteur, ek werk nog aan sy Afrikaans – sorry<br />

Zak!<br />

Nou ja ek het laas verkondig dat daar altyd<br />

n humoristiese aspek in die meeste dinge<br />

in die lewe is maar die politieke woeling<br />

rondom onse Minister van Finansies sal<br />

enige regdenkende persoon skyt bang<br />

maak. Ons normale mense verdien nie<br />

geld in $ nie en ons het ook niks om uit te<br />

voer om $ te verdien nie so dit is moeilik<br />

om iets snaaks in hierdie situasie te sien.<br />

Dit is mos nie snaaks om kaalvoet in nat<br />

hondebollie te trap nie behalwe vir die<br />

person wat dit waarneem. Ai, Afrika is<br />

mos nie vir sissies nie maar dit voel of ek<br />

aan ‘n bang babelaas ly.<br />

Die eerste langnaweek is verby en vir die<br />

van ons wat met Jantuisbly se karretjie<br />

gereis het weens finansies, of ‘n gebrek<br />

daaraan, moes maar toe kyk hoe die<br />

ander helfde met 4X4’s gepak met<br />

bergfietse, quads, karavane, motorbote<br />

en wat nog al verby ons flits. Ons oppad<br />

werktoe, hulle oppad na waar ookal<br />

hulle vet beursies hulle kon neem. Is ek<br />

suurgat? Nee maar dit voel net bleddie<br />

onregverdig, miskien doen hulle dit op<br />

hul kredietkaarte, pasop, is al wat ek<br />

kan vermaan, moenie dat jou volgende<br />

opdraande skuldbult is nie!

Komende April het nog vakansiedae<br />

en in baie huishoudings gaan daar<br />

kinders wees wat moan dat Jannie , die<br />

skoolvriend, weg is met vakansie en ons<br />

moet verveeld by die huis sit, daar is nie<br />

n maatjie om mee te speel nie, dis nie fair<br />

nie. Is daar n kits oplossing? Ongelukkig<br />

nie maar as die son skyn en daar is nog<br />

‘n geldjie om ‘n braai te hou is die Kaap<br />

nog Hollands. Al het die braai gekrimp<br />

na hamburger patties dan noem ons<br />

dit maar n barbeque en verbeel ons<br />

dat ons in die US of A is, miskien nie<br />

perfek nie maar dit is nie nodig dat ons<br />

‘n doodskleed oor ons gemoedere trek<br />

nie. As vleis nie op die spyskaart is nie<br />

kry n ou pan en laat die kinders help om<br />

pannekoek te maak, ja sommer op ‘n<br />

vuurtjie.Luister musiek, vertel die kinders<br />

van die ou dae en deel jou drome.<br />

Groete van die Republiek van Skyt Akfrika. Ons gesels met<br />

julle ondersteuning volgende maand weer.<br />

Christo Hattingh<br />

Kyk gerus my LinkedIn profile:<br />

https://www.linkedin.com/in/christo-hattingh-351a52130/<br />

* Seriously please do let us know if you found this article to be<br />

funny/offensive/amusing/interesting feedback@debtfreedigi.co.za

Debt Counsellors Associations<br />

Announcement Board<br />

Regional Meetings<br />

Kwa-Zulu Natal: 19/05/17<br />

Western Cape: 23/05/17<br />

Gauteng: 23/05/17<br />

Freestate: 12/05/17<br />

Eastern Cape: 21/07/17<br />

The Date of the DCASA Annual Conference is<br />

Wednesday the 16th August <strong>2017</strong><br />

Check out this huge banner that someone<br />

draped over the N1 highway in Joburg:<br />

http://ewn.co.za/<strong>2017</strong>/01/09/fnb-customertakes-fight-with-bank-to-the-streets<br />

www.dcasa.co.za<br />

www.newera.org.za<br />

1. The Executive committee will hold its first<br />

meeting by end of <strong>March</strong> <strong>2017</strong><br />

2. The main focus in <strong>2017</strong> is on ensuring that all<br />

BDCF members comply with all legislation,<br />

regulations and conditions of registration.<br />

3. Our communication channels will be<br />

strengthened to enhance accessibility by<br />

members.<br />

4. Special projects will be launched around April<br />

in areas such as Incapacitation or death of DCs,<br />

usage of PDAs by consumers, as well as fees.<br />

5. Members and supporters will be fully engaged<br />

when the projects are launched to ensure<br />

maximum input and participation.<br />

www.bdcf.co.za<br />

Want to attend an AllProDC meeting<br />

in your area next month? We will be<br />

discussing professionalism, new DC fees<br />

and possible amendments to the Act.<br />

Let us know:<br />

bernidene@csdebtcounselling.co.za<br />

www.allprodc.org

march<br />

NEWSLETTER<br />

Regional Meetings<br />

At the recent AGM it was highlighted how important it is for our members to get to meet<br />

face to face (in addition to meeting online and chatting on Facebook). It allows for an<br />

exchange of experience and offers the chance for members to discuss regional issues that<br />

are particular to their area. We invite members to offer to host a regional meeting at their<br />

facilities. Those wishing to host a meeting can email: bernidene@csdebtcounselling.co.za<br />

who will then be able to notify local members and find a convenient date.<br />

DC Fees and Amendments to the NCA<br />

As yet it seems that the NCR still intend to find an Actuary to review the 3 possible fee<br />

structures that were proposed after their recent research. AS yet the possible fee structure<br />

has not been made available for comment. We invite members to discuss this topic on<br />

the facebook page and at their regional meetings. We also ask that members continue to<br />

discuss possible amendments to the NCA which will improve the debt review process or<br />

bring clarity to the process. We would like to compile all the suggestions from our members<br />

to present to the relevant parties in the near future.<br />

Membership<br />

Debt Counselling is a very complicated professional process that needs to be well<br />

managed. The Alliance of Professional Debt Counsellors want to ensure that members<br />

are up to standard and offer professional services as our name reflects. This topic will be<br />

on the agenda for regional meetings. We urge all members to maintain a high level of<br />

customer service and professionalism. If you are a professional Debt Counsellor who would<br />

like representation and the benefit of resource sharing then please contact our association<br />

secretary on bernidene@csdebtcounselling.co.za<br />

www.allprodc.org<br />

FACEBOOK: www.facebook.com/AllProDC / TWITTER: www.twitter.com/AllProDC

FINWISE - Innovative Debt Management Program<br />

No monthly program fees!<br />

Accessible on PC or Desktop<br />

• Excellent audit trail<br />

• Workflow management<br />

• Easy to navigate functions<br />

• Quick data capturing<br />

• DCRS and standard proposals<br />

accommodated.<br />

‘’ I was pleasantly surprised by our experience and changeover to Finwise. The<br />

new system is intuitive and easy to understand.‘’<br />

Debt Counsellor Eastern Cape<br />

‘’ I’ve found the Finwise system to be very useful. I’m new in the debt counselling<br />

field, I managed to find my way around the system as it is very user-friendly. The<br />

training manuals provided are also helpful and informative.’’<br />

Debt Counsellor Gauteng

BUSINESS SUCCESS - THE “GO-GETTER” APPROACH<br />

Various things like good financial management and quality products are vital to run a<br />

successful business. Human capital, however, is the driving force in any business and<br />

can make or break a business. Looking at successful businesses, they are high energy<br />

and the staff are passionate, motivated and believe in the business objectives. The<br />

‘’go-getters’’ see opportunities in every situation and when interacting with clients,<br />

they instill trust with the positive image they deliver about the organizations they work<br />

for. Persons with a ‘’can do’’ attitude are needed in all walks of life, the ones who say<br />

yes to change because change means growth. What kind of business leader or person<br />

are you? Challenge yourself to be a go-getter with a can do attitude and align your<br />

company with businesses practicing the same good conduct.<br />

Some Qualities of the ‘’Go-Getter’’<br />

• The go-getter attitude does not hesitate; he/she thinks, when do I start?<br />

• The go-getter attitude does not ponder whether he/she can, they know they can<br />

get it done with collaboration and action.<br />

• The go-getter believes in him/herself, and the company. He/she believes in the<br />

times ahead and wants to be a key part of it.<br />

• The go-getter sees continual change as a recurrent opportunity.<br />

• The go-getter only knows one way of doing and living: with bravery,<br />

self-assurance, passion and integrity.<br />

Why settle for less? DC Partner is positively orientated towards change, growth, industry<br />

development, product enhancement and delivering high quality customer service.<br />

Article by: Petro de Beer<br />

Say yes to change, say yes to a company with a<br />

‘’Can do Approach ‘’ and a ‘’Go-Getter team’’!<br />

Head Office 59 Victoria Street, George<br />

Telephone 044 873 4530 Fax 086 246 2450<br />

www.dcpartner.co.za

JOBS<br />

apply for your dream job now<br />

Join the<br />

Meerkat Team<br />

An exciting place to work!<br />

Meerkat are looking for:<br />

Frontline Sales Agents<br />

to join our energetic team.<br />

This is a great opportunity to become part of a fast-paced, high growth<br />

and professional debt counselling environment.<br />

We offer a consistent hot lead flow as well as an aggressive remuneration model.<br />

If you are looking for a company with an entrepreneurial spirit at its heart,<br />

and are keen to join a dynamic, hardworking but fun team contact us.<br />

We would love to hear from you!<br />

Mail us on info@meerkat.co.za<br />

www.meerkat.co.za/careers/<br />

MyMeerkat (PTY) Ltd. Meerkat is an authorised financial services provider (FSP 46535)

DEBT COUNSELLING<br />

COMMUNITY SUPPORT<br />

Debt Review Is A Marathon Not A Sprint<br />

Would you sponsor R100 if our DCCS runner could finish the Two Oceans Marathon?<br />

We put in the blood, sweat and tears and you put in R100 but ONLY IF OUR RUNNER MAKES IT.<br />

DEBT COUNSELLING<br />

COMMUNITY SUPPORT<br />

We then use those funds to support DCCS projects and help those vulnerable debt review<br />

clients who are in desperate need of assistance to stay in the process.<br />

To sponsor contact:<br />

bernidene@dccsupport.co.za<br />

Check out our website for pictures, stories and more and as always if you would like to get<br />

involved in one of our projects (like our back to school project for Jan) then we ask that you<br />

simply email admin@dccsupport.co.za

click the c<br />

Service D<br />

Debt CounsellORS<br />

Support<br />

services<br />

TRAINING<br />

FINANCIAL<br />

FINANCIAL<br />

PLANNING

irectory<br />

aTEGORY<br />

DO YOU WANT TO LIST<br />

YOUR COMPANY?<br />

directory@debtfreedigi.co.za<br />

LEGAL<br />

CREDIT BUREAUS<br />

PAYMENT<br />

DISTRIBUTION<br />

AGENCIES<br />

CREDIT PROVIDER CONTACT<br />

DETAILS & ESCALATION PROCESS

Debt CounsellORS<br />

Gauteng<br />

KwaZulu-<br />

Natal<br />

Free State

Limpopo North West Eastern CapE<br />

Mpumalanga Northern Cape Western Cape

Gauteng<br />

PENNY WISE<br />

Cathy Foster<br />

Debt Counsellor – NCRDC1977<br />

Penny Wise Debt Counselling<br />

Tel: (011) 679 1540<br />

Fax: 086 719 3378<br />

Mobile: 083 298 4467<br />

Email: cathy@pennywise.co.za<br />

www.pennywise.co.za<br />

Credit Matters<br />

South Africa’s Leading<br />

Debt Counsellors<br />

14th Floor, The Pinnacle<br />

Cnr Strand & Burg St<br />

Cape Town<br />

Tel: 086 111 6197<br />

Fax: 021 425 6292<br />

info@creditmatters.co.za<br />

MV Business Empowerment<br />

9 River Road<br />

Morning Hill<br />

Bedfordview<br />

(next to Eastgate mall)<br />

Tel: 083 490 3339<br />

velaphi@infitech.co.za<br />

Armani Debt Counselling<br />

Take the First Step<br />

to Financial Freedom<br />

Tania Dekker<br />

Tel: 011 849 3654 / 7659<br />

www.armanigroup.co.za<br />

Dynamix Debt Counselling TLC<br />

Alida Christie NCRDC2324<br />

Office 1, 34 Beefwoodstreet,<br />

Vanderbijlpark, 1911<br />

Tel: 079 520 4369<br />

Tel: 016 100 8020<br />

tlcdebt@mweb.co.za

Specialist Debt Management Centre<br />

Beverley Ludick, NCRDC948<br />

Pretoria<br />

Tel: 012 377-3557<br />

Email: obligco@gmail.com<br />

Email: dc@obligco.co.za<br />

www.obligco.co.za Tel: 0861 123 644<br />

Email: info@debtrescue.co.za<br />

Creators In Financial Wellbeing<br />

NCRDC677<br />

You Are Not Alone<br />

We’ll handle your creditors so you<br />

don’t have to!<br />

1 Dingler Street, Rynfield, Benoni<br />

0861 10 11 00<br />

info@debtmend.co.za<br />

www.debtmend.co.za<br />

NCRDC197<br />

Tel: 011 660 9970<br />

Fax: 086 540 5017<br />

KRUGERSDORP<br />

e-mail: nicky@nvdmdc.co.za<br />

www.nvdmdc.co.za<br />

All Debt Solutions<br />

Fast tracking your financial freedom<br />

Tel: 0861 255 3328 / 021-557 9981<br />

Email: info@allds.co.za<br />

www.alldebtsolutions.co.za<br />

https://www.facebook.com/<br />

alldebtsolutions<br />

CCDC<br />

Consumer Care Is our Priority.<br />

Tel: 018 462 4263 / 073 624 6949<br />

Email: info@ccdc.co.za<br />

www.ccdc.co.za

Debt Review Specialists<br />

23 Coronation Road<br />

Mithanagar<br />

Tongaat<br />

4399<br />

Tel: 071 222 9481<br />

Tel: 032 944 3446<br />

admin@kmadebt.co.za<br />

www.kmadebt.co.za<br />

Credit Matters<br />

South Africa’s Leading<br />

Debt Counsellors<br />

14th Floor, The Pinnacle<br />

Cnr Strand & Burg St<br />

Cape Town<br />

Tel: 086 111 6197<br />

Fax: 021 425 6292<br />

info@creditmatters.co.za<br />

KwaZulu-<br />

Natal<br />

Restore your<br />

financial wellness<br />

Our Debt Management<br />

Process is Easy!<br />

DEBT<br />

REVIEW<br />

AWARDS<br />

Telephone<br />

031 303 2448 / 084 250 2356<br />

www.debtfinesse.co.za

Helping you to get back on your<br />

feet and on the road to recovery<br />

The Square<br />

250 Umhlanga Rocks Drive<br />

Umhlanga<br />

Durban<br />

4319<br />

Tel: 031 566 2029<br />

Tel: 071 902 4445<br />

info@mnmdebtrecovery.co.za<br />

www.mnmdebtrecovery.co.za<br />

Tel: 0861 123 644<br />

Email: info@debtrescue.co.za<br />

National Debt Advisors<br />

Fighting For Consumer Justice<br />

Tel: 021 007 1688<br />

www.nationaldebtadvisors.co.za

National Debt Advisors<br />

Fighting For Consumer Justice<br />

Tel: 021 007 1688<br />

www.nationaldebtadvisors.co.za<br />

Credit Matters<br />

South Africa’s Leading<br />

Debt Counsellors<br />

14th Floor, The Pinnacle<br />

Cnr Strand & Burg St<br />

Cape Town<br />

Tel: 086 111 6197<br />

Fax: 021 425 6292<br />

info@creditmatters.co.za<br />

Free State<br />

Tel: 0861 123 644<br />

Email: info@debtrescue.co.za

Limpopo<br />

National Debt Advisors<br />

Fighting For Consumer Justice<br />

Tel: 021 007 1688<br />

www.nationaldebtadvisors.co.za<br />

Credit Matters<br />

South Africa’s Leading<br />

Debt Counsellors<br />

14th Floor, The Pinnacle<br />

Cnr Strand & Burg St<br />

Cape Town<br />

Tel: 086 111 6197<br />

Fax: 021 425 6292<br />

info@creditmatters.co.za<br />

Depopulating a generation of over<br />

indebted and populating a debt free<br />

generation.<br />

Office no 2, 5 A Schoeman Street,<br />

Polokwane<br />

Tel: 0152912731<br />

Tel: 0877028518<br />

Email: admaau66@gmail.com<br />

www.maaudebts.co.za<br />

SMS Salary Management Services<br />

Annerien de Jager<br />

Registered Debt Counsellor<br />

NCRDC0075<br />

015 307 2772<br />

info@smslimpopo.co.za<br />

Tel: 0861 123 644<br />

Email: info@debtrescue.co.za

National Debt Advisors<br />

Fighting For Consumer Justice<br />

Tel: 021 007 1688<br />

www.nationaldebtadvisors.co.za<br />

Tel: 0861 123 644<br />

Email: info@debtrescue.co.za<br />

Mpumalanga<br />

Credit Matters<br />

South Africa’s Leading<br />

Debt Counsellors<br />

14th Floor, The Pinnacle<br />

Cnr Strand & Burg St<br />

Cape Town<br />

Tel: 086 111 6197<br />

Fax: 021 425 6292<br />

info@creditmatters.co.za

National Debt Advisors<br />

Fighting For Consumer Justice<br />

Tel: 021 007 1688<br />

www.nationaldebtadvisors.co.za<br />

Credit Matters<br />

South Africa’s Leading<br />

Debt Counsellors<br />

14th Floor, The Pinnacle<br />

Cnr Strand & Burg St<br />

Cape Town<br />

Tel: 086 111 6197<br />

Fax: 021 425 6292<br />

info@creditmatters.co.za<br />

North West<br />

Depopulating a generation of over<br />

indebted and populating a debt free<br />

generation.<br />

Tel: 0861 123 644<br />

Email: info@debtrescue.co.za<br />

Office No. 6, Prime Pharm Building,<br />

36 Dr Nelson Mandela Drive<br />

Tel: 0186320053<br />

Tel: 0877026744<br />

Email: papi@maaudebts.co.za<br />

www.maaudebts.co.za

National Debt Advisors<br />

Fighting For Consumer Justice<br />

Tel: 021 007 1688<br />

www.nationaldebtadvisors.co.za<br />

Credit Matters<br />

South Africa’s Leading<br />

Debt Counsellors<br />

14th Floor, The Pinnacle<br />

Cnr Strand & Burg St<br />

Cape Town<br />

Tel: 086 111 6197<br />

Fax: 021 425 6292<br />

info@creditmatters.co.za<br />

Northern Cape<br />

Tel: 0861 123 644<br />

Email: info@debtrescue.co.za

National Debt Advisors<br />

Fighting For Consumer Justice<br />

Tel: 021 007 1688<br />

www.nationaldebtadvisors.co.za<br />

Credit Matters<br />

South Africa’s Leading<br />

Debt Counsellors<br />

14th Floor, The Pinnacle<br />

Cnr Strand & Burg St<br />

Cape Town<br />

Tel: 086 111 6197<br />

Fax: 021 425 6292<br />

info@creditmatters.co.za<br />

Eastern CapE<br />

Tel: 0861 123 644<br />

Email: info@debtrescue.co.za

WEBSITE | www.debt-therapy.co.za<br />

debt therapy<br />

integrity guaranteed<br />

debt therapy is registered with NCR | NCRDC49<br />

National Debt Advisors<br />

Fighting For Consumer Justice<br />

Tel: 021 007 1688<br />

www.nationaldebtadvisors.co.za<br />

Drastically reduce your monthly<br />

debt repayments<br />

Let US help 0861111863<br />

Regain control of your finances<br />