BOB_2017_SMALL

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

NOTES TO THE FINANCIAL STATEMENTS<br />

ANNUAL REPORT AND<br />

FINANCIAL STATMENTS <strong>2017</strong><br />

38. Comparative figures<br />

Previous year’s figures have been regrouped / rearranged wherever necessary in order to make them comparable with that of<br />

current financial period.<br />

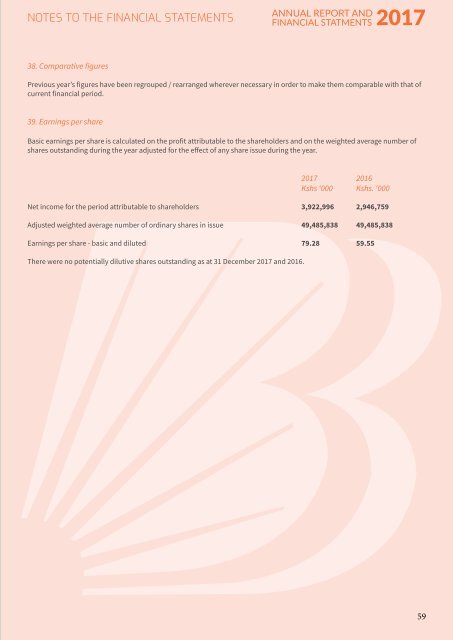

39. Earnings per share<br />

Basic earnings per share is calculated on the profit attributable to the shareholders and on the weighted average number of<br />

shares outstanding during the year adjusted for the effect of any share issue during the year.<br />

<strong>2017</strong> 2016<br />

Kshs ‘000 Kshs. ‘000<br />

Net income for the period attributable to shareholders 3,922,996 2,946,759<br />

Adjusted weighted average number of ordinary shares in issue 49,485,838 49,485,838<br />

Earnings per share - basic and diluted 79.28 59.55<br />

There were no potentially dilutive shares outstanding as at 31 December <strong>2017</strong> and 2016.<br />

59