RA BRS 2003 GB >pdf

RA BRS 2003 GB >pdf

RA BRS 2003 GB >pdf

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

26<br />

year (with the Dardenelles transit only permitted in<br />

daylight hours) these add at least another two<br />

days to voyage times. With an ever-increasing rise<br />

in traffic, there are real jams, which can double the<br />

theoretical transit time. This simple measure naturally<br />

affects tonnage availability and helps push<br />

rates higher.<br />

As already mentioned, West Africa is in the process<br />

of losing its position as a driving force, even<br />

though it still represents an important share of the<br />

global traffic, especially towards the U.S.. On this<br />

route the average rate experienced this year was<br />

around WS 78,5 compared to an average in 2001<br />

close to WS 110.<br />

During the first nine months of the year, with the<br />

exception of a slight hike in June, returns remained<br />

below $15,000 per day. Proof of the predominant<br />

influence of economic events on rates, this<br />

size of tankers has remained globally balanced in<br />

terms of numbers for many years. Thus since<br />

1998, 106 new units (15,9 million dwt) have been<br />

delivered while 107 (14,7 million dwt) have been<br />

scrapped.<br />

2002 however differed slightly from preceding years<br />

with 25 units delivered as compared to only 15 ships<br />

withdrawn from the fleet. Another important phenomena<br />

in relation to previous years was the<br />

conversion of units destined to the offshore market<br />

being more favourable to VLCC than to Suezmax.<br />

Consequently only 2 old Suezmax were converted in<br />

2002 as compared to half a dozen VLCCs.<br />

US$/day<br />

80,000<br />

70,000<br />

60,000<br />

50,000<br />

40,000<br />

30,000<br />

20,000<br />

10,000<br />

Shipping and Shipbuilding Markets <strong>2003</strong><br />

0<br />

Jan 00<br />

Feb 00<br />

Mar 00<br />

May 00<br />

June 00<br />

July 00<br />

Sep 00<br />

Oct 00<br />

Dec 00<br />

Jan 01<br />

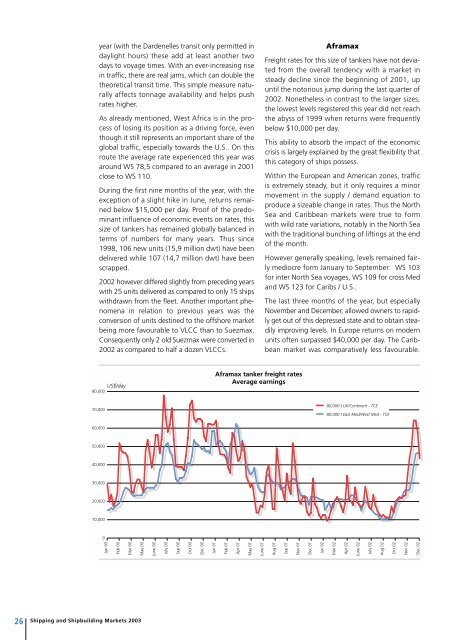

Aframax tanker freight rates<br />

Average earnings<br />

Feb 01<br />

Apr 01<br />

May 01<br />

June 01<br />

Aframax<br />

Freight rates for this size of tankers have not deviated<br />

from the overall tendency with a market in<br />

steady decline since the beginning of 2001, up<br />

until the notorious jump during the last quarter of<br />

2002. Nonetheless in contrast to the larger sizes,<br />

the lowest levels registered this year did not reach<br />

the abyss of 1999 when returns were frequently<br />

below $10,000 per day.<br />

This ability to absorb the impact of the economic<br />

crisis is largely explained by the great flexibility that<br />

this category of ships possess.<br />

Within the European and American zones, traffic<br />

is extremely steady, but it only requires a minor<br />

movement in the supply / demand equation to<br />

produce a sizeable change in rates. Thus the North<br />

Sea and Caribbean markets were true to form<br />

with wild rate variations, notably in the North Sea<br />

with the traditional bunching of liftings at the end<br />

of the month.<br />

However generally speaking, levels remained fairly<br />

mediocre form January to September: WS 103<br />

for inter North Sea voyages, WS 109 for cross Med<br />

and WS 123 for Caribs / U.S..<br />

The last three months of the year, but especially<br />

November and December, allowed owners to rapidly<br />

get out of this depressed state and to obtain steadily<br />

improving levels. In Europe returns on modern<br />

units often surpassed $40,000 per day. The Caribbean<br />

market was comparatively less favourable.<br />

Aug 01<br />

Sep 01<br />

Nov 01<br />

Dec 01<br />

Jan 02<br />

80,000 t UK/Continent - TCE<br />

80,000 t East Med/West Med - TCE<br />

Mar 02<br />

Apr 02<br />

June 02<br />

July 02<br />

Aug 02<br />

Oct 02<br />

Nov 02<br />

Dec 02