RA BRS 2003 GB >pdf

RA BRS 2003 GB >pdf

RA BRS 2003 GB >pdf

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

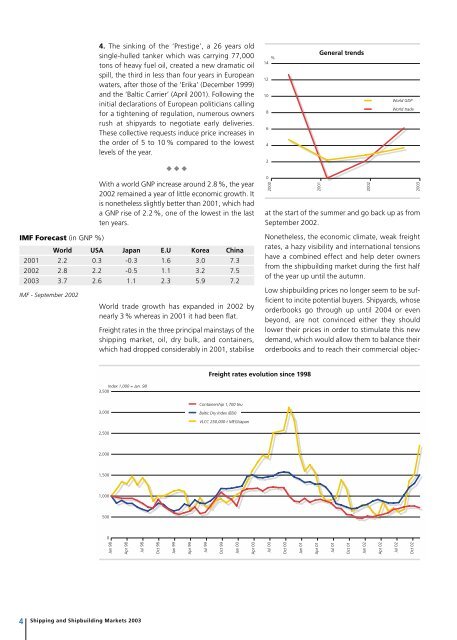

IMF Forecast (in GNP %)<br />

4<br />

Shipping and Shipbuilding Markets <strong>2003</strong><br />

4. The sinking of the ‘Prestige’, a 26 years old<br />

single-hulled tanker which was carrying 77,000<br />

tons of heavy fuel oil, created a new dramatic oil<br />

spill, the third in less than four years in European<br />

waters, after those of the ‘Erika’ (December 1999)<br />

and the ‘Baltic Carrier’ (April 2001). Following the<br />

initial declarations of European politicians calling<br />

for a tightening of regulation, numerous owners<br />

rush at shipyards to negotiate early deliveries.<br />

These collective requests induce price increases in<br />

the order of 5 to 10 % compared to the lowest<br />

levels of the year.<br />

◆ ◆ ◆<br />

With a world GNP increase around 2.8 %, the year<br />

2002 remained a year of little economic growth. It<br />

is nonetheless slightly better than 2001, which had<br />

a GNP rise of 2.2 %, one of the lowest in the last<br />

ten years.<br />

World USA Japan E.U Korea China<br />

2001 2.2 0.3 -0.3 1.6 3.0 7.3<br />

2002 2.8 2.2 -0.5 1.1 3.2 7.5<br />

<strong>2003</strong> 3.7 2.6 1.1 2.3 5.9 7.2<br />

IMF - September 2002<br />

World trade growth has expanded in 2002 by<br />

nearly 3 % whereas in 2001 it had been flat.<br />

Freight rates in the three principal mainstays of the<br />

shipping market, oil, dry bulk, and containers,<br />

which had dropped considerably in 2001, stabilise<br />

Index 1,000 = Jan. 98<br />

3,500<br />

3,000<br />

2,500<br />

2,000<br />

1,500<br />

1,000<br />

500<br />

0<br />

Jan 98<br />

Apr 98<br />

Jul 98<br />

Oct 98<br />

Jan 99<br />

Apr 99<br />

Jul 99<br />

Freight rates evolution since 1998<br />

Containership 1,700 teu<br />

Baltic Dry Index (BDI)<br />

VLCC 250,000 t MEG/Japan<br />

Oct 99<br />

Jan 00<br />

Apr 00<br />

%<br />

14<br />

12<br />

10<br />

8<br />

6<br />

4<br />

2<br />

0<br />

2000<br />

at the start of the summer and go back up as from<br />

September 2002.<br />

Nonetheless, the economic climate, weak freight<br />

rates, a hazy visibility and international tensions<br />

have a combined effect and help deter owners<br />

from the shipbuilding market during the first half<br />

of the year up until the autumn.<br />

Low shipbuilding prices no longer seem to be sufficient<br />

to incite potential buyers. Shipyards, whose<br />

orderbooks go through up until 2004 or even<br />

beyond, are not convinced either they should<br />

lower their prices in order to stimulate this new<br />

demand, which would allow them to balance their<br />

orderbooks and to reach their commercial objec-<br />

Jul 00<br />

Oct 00<br />

Jan 01<br />

2001<br />

Apr 01<br />

General trends<br />

Jul 01<br />

Oct 01<br />

Jan 02<br />

2002<br />

Apr 02<br />

World GDP<br />

World trade<br />

Jul 02<br />

Oct 02<br />

<strong>2003</strong>