Ferro-alloys - Metal Bulletin Store

Ferro-alloys - Metal Bulletin Store

Ferro-alloys - Metal Bulletin Store

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

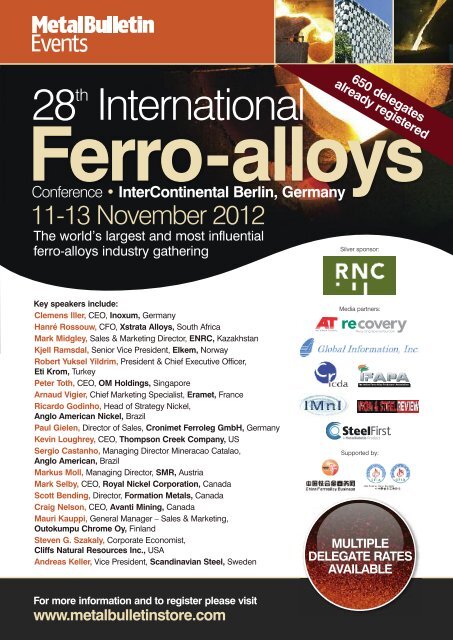

28<br />

th<br />

International<br />

<strong>Ferro</strong>-<strong>alloys</strong><br />

Conference • InterContinental Berlin, Germany<br />

11-13 November 2012<br />

The world’s largest and most influential<br />

ferro-<strong>alloys</strong> industry gathering<br />

Key speakers include:<br />

Clemens Iller, CEO, Inoxum, Germany<br />

Hanré Rossouw, CFO, Xstrata Alloys, South Africa<br />

Mark Midgley, Sales & Marketing Director, ENRC, Kazakhstan<br />

Kjell Ramsdal, Senior Vice President, Elkem, Norway<br />

Robert Yuksel Yildrim, President & Chief Executive Officer,<br />

Eti Krom, Turkey<br />

Peter Toth, CEO, OM Holdings, Singapore<br />

Arnaud Vigier, Chief Marketing Specialist, Eramet, France<br />

Ricardo Godinho, Head of Strategy Nickel,<br />

Anglo American Nickel, Brazil<br />

Paul Gielen, Director of Sales, Cronimet <strong>Ferro</strong>leg GmbH, Germany<br />

Kevin Loughrey, CEO, Thompson Creek Company, US<br />

Sergio Castanho, Managing Director Mineracao Catalao,<br />

Anglo American, Brazil<br />

Markus Moll, Managing Director, SMR, Austria<br />

Mark Selby, CEO, Royal Nickel Corporation, Canada<br />

Scott Bending, Director, Formation <strong>Metal</strong>s, Canada<br />

Craig Nelson, CEO, Avanti Mining, Canada<br />

Mauri Kauppi, General Manager – Sales & Marketing,<br />

Outokumpu Chrome Oy, Finland<br />

Steven G. Szakaly, Corporate Economist,<br />

Cliffs Natural Resources Inc., USA<br />

Andreas Keller, Vice President, Scandinavian Steel, Sweden<br />

For more information and to register please visit<br />

www.metalbulletinstore.com<br />

650 delegates<br />

already registered<br />

Silver sponsor:<br />

Media partners:<br />

Supported by:<br />

MULTIPLE<br />

DELEGATE RATES<br />

AVAILABLE

28<br />

th<br />

International<br />

<strong>Ferro</strong>-<strong>alloys</strong><br />

Conference • InterContinental Berlin, Germany<br />

<strong>Metal</strong> <strong>Bulletin</strong> Events’ 28th International <strong>Ferro</strong>-<strong>alloys</strong> Conference<br />

(IFA) will once again bring together the world of ferro-<strong>alloys</strong><br />

under one roof in Berlin on 11-13 November 2012.<br />

Already confirmed this year are many of the global industries most important<br />

miners, producers, smelters, steel mills and logistics/service companies.<br />

Wherever your position in the ferro-<strong>alloys</strong> value chain, the conference offers<br />

unrivalled opportunities to meet and secure deals with your customers, suppliers<br />

and competitors.<br />

The following companies have already registered delegations:<br />

l AB <strong>Ferro</strong>legeringar<br />

l Abel <strong>Metal</strong> Services Pty Ltd<br />

l Acarer <strong>Metal</strong> Sanayi Ticaret AS<br />

l Acarer <strong>Metal</strong> Sanayi VE Ticaret AS<br />

l Affival Inc<br />

l Afro Minerals Trading AG<br />

l Al Ezz Dekheila Company –<br />

Alexandria<br />

l ALKOR Spj<br />

l Allied <strong>Metal</strong>s Corp<br />

l Allied <strong>Metal</strong>s GmbH<br />

l Alloys & <strong>Metal</strong>s INDIA<br />

l AlzChem AG<br />

l Ampere Alloys<br />

l Andina Group<br />

l Anglo American<br />

l Anglo American –<br />

Mineracao Catalao<br />

l Aria International GmbH<br />

l ARTEX II<br />

l Artex II SPJ<br />

l Asaco<br />

l Asia Minerals Ltd<br />

l Asil Celik Sanayi ve Ticaret A.S<br />

l ASO Siderurgica SrL<br />

l Aveks AS<br />

l Befesa Steel Services GmbH<br />

l Besta Group SA<br />

l BHP Billiton<br />

l BHP Billiton International<br />

<strong>Metal</strong>s BV<br />

l Bohler Schweisstechnik Austria<br />

GmbH<br />

l Bozel Europe<br />

l Brindavan Enterprises Pvt Ltd<br />

l Camelot Group Ltd<br />

l Camet <strong>Metal</strong>lurgie GmbH<br />

l Capital International<br />

l Carboleghe Srl<br />

l Casasco & Nardi Spa<br />

l Cast <strong>Metal</strong> Services Pty Ltd<br />

l CBMM Europe BV<br />

l CCMA LLC<br />

l CEDIE Cedifil Cored Wire<br />

l Chengdu Molyplus<br />

Technologies Ltd<br />

l China National Nonferrous <strong>Metal</strong>s<br />

Import & Export Jiangxi Corp Ltd<br />

l Chrome Partners<br />

l Cia <strong>Ferro</strong>ligas Minas Gerais<br />

Minasligas<br />

l Cliffs Natural Resources<br />

l Climax Molybdenum<br />

l CMC Cometals<br />

l Cogne Acciai Speciali Spa<br />

l Cometal SA<br />

l Commexim Group AS<br />

l Compania Minera Autlan<br />

SAB de CV<br />

l Concast Steel and Power Ltd<br />

l Credit Suisse<br />

l Credit Suisse AG<br />

l Cronimet <strong>Ferro</strong>leg GmbH<br />

l Cronimet Noble Alloys<br />

Handelsges mbH<br />

l CTB Magemon SA<br />

l Cunico Marketing FZE<br />

l Daido Kogyo Co Ltd<br />

l Dala Mining<br />

l Dala Mining LLC<br />

l David J Joseph Co <strong>Ferro</strong><br />

Alloy Group<br />

l dbt Duisburg Bulk Terminal GmbH<br />

l DCM Decometal GmbH<br />

l De <strong>Metal</strong> AS<br />

l Delachaux Gennevilliers<br />

l DEUMU GmbH<br />

l Deutsche Nickel GmbH<br />

l Duferco SA<br />

l East <strong>Metal</strong>s AG<br />

l Ekin Maden Tic Ve San AS<br />

l Electrometalurgica Andina SAIC<br />

l Elkem AS Materials<br />

l Enco International Inc<br />

l ENRC Marketing AG<br />

l ENRC Marketing LLC<br />

l Eramet International<br />

l Eregli Iron and Steel Works Co<br />

l ESD SIC<br />

l Eti Krom Inc<br />

l Euro Rijn International BV<br />

l Euroinvest International Srl<br />

l Euromet SA<br />

l Euroports Inland Terminals<br />

l Euro-Rijn International BV<br />

l Evraz Holding<br />

l Exiros Techint Group<br />

l Ezz Steel Co<br />

l Ferco<br />

l <strong>Ferro</strong>atlantica Deutschland GmbH<br />

l <strong>Ferro</strong>atlantica SA<br />

l <strong>Ferro</strong>trade Consulting AG<br />

l Filhet Allard Maritime<br />

l FIMBank plc<br />

l Finnfjord AS<br />

l Fondel<br />

l Fondel <strong>Metal</strong>s BV<br />

l Forsteel Srl<br />

l Fulger Industrial Dynamic<br />

l FW Hempel <strong>Metal</strong>lurgical GmbH<br />

l Galmet Srl<br />

l Genoa <strong>Metal</strong> Terminal Srl<br />

l Georgsmarienhuette Holding<br />

l Gerdau<br />

l Gerdau Group<br />

l GfE <strong>Metal</strong>le und Materialien GmbH<br />

l GfE MIR AG<br />

l GFM Fesil GmbH<br />

l Global Bulk Logistic GmbH<br />

l Global Metwire Injection<br />

l Globe <strong>Metal</strong>es SA<br />

l Globus 8 Alloys Ptd Ltd<br />

l Gloria Material Technology Corp<br />

l Gradient AS<br />

l Gruppo Cividale<br />

l Gulf <strong>Ferro</strong> Alloys Co Sabayek<br />

l Haldor Topsoe AS<br />

l Hangten Asia Co Ltd<br />

l Hanwa Co Ltd<br />

l Hornos Electricos de<br />

Venezuela SA<br />

l HS Alloys<br />

l Ibermet doo<br />

l Icdas AS<br />

l ICI UK Ltd Ukrainian<br />

Representative Office<br />

l Impex <strong>Ferro</strong> Tech Ltd<br />

l IMT Shipping & Chartering GmbH<br />

l Inner Mongolia Alashan Xingda<br />

<strong>Ferro</strong>alloy Ltd<br />

l Insimbi Alloys Supplies Pty<br />

l Inspectorate Hoff<br />

l Inspectorate International Ltd<br />

l Inter<strong>alloys</strong> Trading & Business<br />

Consulting<br />

l Intermetal SA<br />

l International Cobalt Company Inc<br />

l International Manganese Institute<br />

l Intertrade Kompani<br />

l Invest <strong>Metal</strong> Sp zoo<br />

l Iran <strong>Ferro</strong>alloy Industries Co<br />

l Iran <strong>Ferro</strong>silice Co<br />

l IRTrading Srl<br />

l Italfond Spa<br />

l Itochu Corporation<br />

l J & E Trading<br />

l Jajoo Exports<br />

l JAP Trading sro<br />

l JFE Shoji Trade Corp<br />

l Jiangsu Shunchi Tungsten &<br />

Molybdenum Products Co Ltd<br />

l JS Company Privat Intertrading<br />

l Karthik Alloys Ltd<br />

l Kay Bee Industrial Alloys Pvt Ltd<br />

l Kovintrade D D Celje<br />

l KTC Korea Co Ltd<br />

l Kwtsteel<br />

l L&M Handels AG<br />

l Lalemant Trucking<br />

l Ledar<br />

l Lemetco GmbH<br />

l Let-Lagerhus Ekstrom AB<br />

l Ligas de Aluminio SA LIASA<br />

l LN <strong>Metal</strong>s International Ltd<br />

l London & Scandinavian<br />

<strong>Metal</strong>lurgical Co Limited<br />

l London <strong>Metal</strong> Exchange<br />

l London <strong>Metal</strong>s Limited<br />

l LS Alloys SA<br />

l Luda Commodities Ltd<br />

l Luxembourg <strong>Metal</strong>lurgical Trade<br />

SA (LMT)<br />

l M B <strong>Metal</strong>s Corporation Ltd<br />

l Maj Komerc Lear<br />

l Marmara <strong>Metal</strong> Mamulleri Tic AS<br />

l Marsh SA<br />

l MBR <strong>Metal</strong>s<br />

l MC <strong>Metal</strong>loinvest LLC<br />

l Meca Trade Oy<br />

l Mechel<br />

l Memor Marketing Pty Ltd<br />

l Mercon Commodities DMCC<br />

l <strong>Metal</strong> Ravne DOO<br />

l <strong>Metal</strong> Trading International Srl<br />

l <strong>Metal</strong> Trading UK Ltd<br />

l <strong>Metal</strong>ink International Co Ltd<br />

l <strong>Metal</strong>leghe SpA<br />

l <strong>Metal</strong>liage Inc<br />

l <strong>Metal</strong>lurgica GmbH & Co. KG<br />

l <strong>Metal</strong>min & CO UK Ltd<br />

l <strong>Metal</strong>min <strong>Metal</strong>s and Minerals Ltd<br />

l <strong>Metal</strong>s & Alloys International Ltd<br />

l <strong>Metal</strong>s & Minerals Imp Exp Co<br />

l Metherma KG<br />

l Metinvest<br />

l Metmar Trading Pty Ltd<br />

l Micon GmbH<br />

l Minelco AB<br />

l Minelco BV<br />

l Minerais US LLC<br />

l Minerall Co Srl<br />

l Minerco International DMMC<br />

l Mitsubishi Corp do Brasil SA<br />

l Molymet Services Ltd<br />

l Mortex Group<br />

l MPT SWEDEN AB<br />

l Nederlandse Erts en<br />

Mineraalbewerking<br />

l Nedstaal B.V.<br />

l Nepa Forwarding BV<br />

l Nepa Rotterdam<br />

l Neska GmbH<br />

l Nippon Denko Co Ltd<br />

l Nizi International SA<br />

l NLMK Services LLC<br />

l Nordmet<br />

l Norecom Limited<br />

l Norsilva AS<br />

l Nova Era Silicon SA<br />

l Novotroitsk Plant of<br />

Chromium Compounds<br />

l Nucor Steel-Arkansas<br />

l Odermath Stahlwerkstechnik<br />

l Omni Industries BV<br />

l OOO Mechel <strong>Ferro</strong><strong>alloys</strong><br />

Management Company<br />

l Ore & <strong>Metal</strong> Co Ltd<br />

l Ore Alloy Development<br />

Corporation Ltd<br />

l Outokumpu Chrome Oy<br />

l Outotec<br />

l Ovako Hofors AB<br />

l Pacorini <strong>Metal</strong>s Rotterdam BV<br />

l PCC Morava Chem sro<br />

l PEC Ltd<br />

l Pimasa<br />

l Pimasa Ltda<br />

l Polchar Sp zoo<br />

l Portnex<br />

l Possehl Mexico SA de CV<br />

l PPH Alkor Sp j<br />

l Promet Czech<br />

l Promet Slovakia sro<br />

l Prometal Corp<br />

l PSI DMCC<br />

l Raw & Refined Commodities AG<br />

l RC Inspection BV<br />

l RC Inspection South Africa<br />

(Pty) Ltd<br />

l RCS Ltd Ruukki Group<br />

l Reward Raw Materials Millbank<br />

Materials<br />

l RFA International<br />

l Rheinfelden Carbon GmbH<br />

l Rima Industrial SA<br />

l Rio Tinto Iron Ore<br />

l Roc International Co Ltd<br />

l Rohit <strong>Ferro</strong> Tech Limited<br />

l Ronly Ltd<br />

l RusChrome GmbH<br />

l Ruukki <strong>Metal</strong>s Oy<br />

l RUX Limited<br />

l Sadaci NV<br />

l Salzgitter Flachstahl GmbH<br />

l Samancor Chrome<br />

l Samchrome FZE<br />

l Sat & Company JSC<br />

l Satka <strong>Metal</strong>lurgical Mill Russia<br />

l Satvik Enterprises Limited<br />

l Scandinavian Steel AB<br />

OVER 1000<br />

DELEGATES<br />

EXPECTED AGAIN<br />

THIS YEAR<br />

l Scandmetal International SA<br />

l Scholz Rohstoffe GmBH & Co KG<br />

l SeAH M&S<br />

l Seatrade Group<br />

l SGL Carbon GmbH<br />

l SGS Supervise Gozetme Etud<br />

Kontrol Servisleri AS<br />

l Shengyuan <strong>Metal</strong> Co Ltd<br />

l Shriram Steels<br />

l Sidenor SA<br />

l Sider<strong>alloys</strong> Intl SA<br />

l SIJ Slovenian Steel Group<br />

l Silcorex SA<br />

l Simpac <strong>Metal</strong>loy Co Ltd<br />

l Sims FE Mottram Ltd<br />

l Sinosteel Germany GmbH<br />

l Sinter srl<br />

l Skopski Leguri Dooel<br />

l SMS-Siemag<br />

l Sonaco Trading AB<br />

l Spring Autumn Commercial<br />

Trade Co Ltd<br />

l SSAB Emea AB<br />

l Ssp BV<br />

l Stalmet SRL<br />

l Stanchem Spj<br />

l Steel Services Sarl<br />

l Stemcor UK Limited<br />

l Sudamin<br />

l Sumitomo Corp<br />

l Sumitomo Corporation Europe<br />

l Tata Steel Trading GmbH<br />

l Tata Steel Europe <strong>Metal</strong>s<br />

Trading BV<br />

l Tata Steel Ymuiden BV<br />

l TD TMZ<br />

l The Egyptian <strong>Ferro</strong> Alloys Co<br />

l ThyssenKrupp <strong>Metal</strong>lurgical<br />

Products GmBh<br />

l ThyssenKrupp Nirosta GmbH<br />

l ThyssenKrupp VDM USA LLC<br />

l TIMA Tungsten GmbH<br />

l Trading House SAT<br />

l Trasteel International SA<br />

l Traxys (UK) Ltd<br />

l Traxys Europe SA<br />

l Traxys North America LLC<br />

l Treibacher Industrie AG<br />

l TUF Group<br />

l Uddeholms AB<br />

l Ultracore Polska Sp zoo<br />

l Uni <strong>Metal</strong> Co Ltd<br />

l Unimet Resources Limited<br />

l United Manganese of Kalahari<br />

l Vale International SA<br />

l Vale Minerals China Co Ltd<br />

l Vallourec & Mannesmann Tubes<br />

l Vargon Alloys AB / Yildirim Group<br />

l Varomet Corp<br />

l Vietnam Youngsun Tungsten<br />

Industry Co Ltd<br />

l Voestalpine Rohstoffbeschaffungs<br />

GmbH<br />

l Votorantim GmbH<br />

l Votorantim Metais<br />

l William Rowland Ltd<br />

l Wogen Pacific Ltd<br />

l Wogen Resources Limited<br />

l Xiangxi Minmetals Co Ltd

Meeting Room Packages<br />

To enhance your networking capabilities we are providing<br />

you access to on-site meeting rooms, priority is given to<br />

companies registering 3 or more delegates. With our<br />

revised price structure we aim to offer cost effective<br />

delegate passes combined with meeting rooms.<br />

Types of meeting rooms include:<br />

l Meeting rooms – access via conference registration,<br />

inside the conference networking and refreshment area<br />

l Meeting rooms – open access to all offering complete<br />

privacy on the second floor<br />

l Senior Suites – limited number available<br />

l Junior Suites – limited number available<br />

Sponsorship & Exhibition<br />

What’s available?<br />

Raise your company profile before, during and after the<br />

event using our unique sponsorship options. Sponsorship<br />

offers longevity and packages are tailored so that your<br />

company can gain exposure from the time of inception to<br />

the event itself.<br />

Meeting room & suite prices/availability<br />

Meeting room name Cost per day Status<br />

Schoenberg 1 € Booked<br />

Schoenberg 2 € Booked<br />

Schoenberg 3 € Booked<br />

Koepenick 1 € Booked<br />

Koepenick 2 € Booked<br />

Koepenick 3 € Booked<br />

Glienicke € Booked<br />

Dahlem € Booked<br />

Rook – 2nd Floor Booked<br />

Chess – 2nd Floor €450 Available<br />

Bishop – 2nd Floor €450 Available<br />

Knight – 2nd Floor €450 Available<br />

King – 2nd Floor €450 Available<br />

Queen – 2nd Floor €450 Available<br />

Check – 2nd Floor €900 Available<br />

Charlottenburg 2 €1000 Available<br />

Charlottenburg 3 €1000 Available<br />

Senior Suites €465 Limited Availablity<br />

Junior Suites €280 Limited Availablity<br />

Reach out to international decision makers and budget<br />

holders at the world’s leading ferro-<strong>alloys</strong> conference<br />

Platinum, Gold, Silver & Bronze sponsorship packages are<br />

available, offering various degrees of exposure. We can<br />

customise a variety of options to suit your budget, objectives<br />

and aspirations.<br />

For sponsorship & exhibition opportunities, please contact:<br />

Manjit Sandhu on telephone: +44 (0) 20 7779 8188 or email: msandhu@metalbulletin.com

Programme<br />

Sunday 11 November 2012<br />

18:00 Welcome drinks reception: Bavarian Oktoberfest<br />

Day one:<br />

Monday 12 November 2012<br />

Plenary session: Meeting room I<br />

Future of the ferro-<strong>alloys</strong> business in the<br />

tough economic times<br />

09:00 Chairman’s opening remarks<br />

09:15 Macroeconomics: how will the unstable situation and the<br />

financial crisis affect the ferro-<strong>alloys</strong> business?<br />

• What is the long term scenario: will the debt crisis in Europe continue to be<br />

the main setback?<br />

• Is the rest of world recovering? How did the USA manage to overcome the<br />

difficulties so quickly? Will it have a knock-on effect on the European economies?<br />

• Lack of credit – did the situation improve through the past year? How did it<br />

affect the industries?<br />

• Currency fluctuation – what will be the future of the Euro? How will it set against<br />

the dollar and will the trust in the single European currency be reinstalled?<br />

Frank Bekaert, Director, Mckinsey, Luxembourg<br />

09:45 Outlook on the global ferro-<strong>alloys</strong> marketplace: is the industry<br />

heading in the right direction?<br />

• European economic downturn and impact on the ferro-<strong>alloys</strong> business<br />

• Supply/demand balance – is the market oversupplied? How does it affect<br />

market dynamics and pricing? Which ferro-<strong>alloys</strong> markets are mostly affected?<br />

• Focus on the ferro-silicon markets – how did they perform in the past year?<br />

What will be the trends ruling the market in the year to come?<br />

• Prospects for the future – will 2013 be a better year for the ferro-<strong>alloys</strong> business?<br />

Kjell Ramsdal, Senior Vice President, Elkem, Norway<br />

10:15 Networking coffee break<br />

11:15 How might the winds blow for 2013 in stainless and special steels?<br />

• Status quo 2012: volumes, prices, margins, growth dynamics for stainless<br />

steel, tool steel and engineering steels<br />

• Outlook for 2013: trends in automotive, consumer goods, process<br />

equipment, oil and gas and power generation, construction<br />

• Consolidation ahead? What will be the impact on the ferro-<strong>alloys</strong> industry?<br />

Markus Moll, Managing Director, SMR, Austria<br />

11:45 Stainless scrap availability and the impact it has on the ferro<strong>alloys</strong><br />

markets<br />

• Overview of the stainless steel scrap market – is the market undersupplied?<br />

• Scrap vs primary raw materials – is there a cost advantage?<br />

• Outlook on the future of the industry – view from the market leader<br />

Paul Gielen, Director Sales, Cronimet <strong>Ferro</strong>leg GmbH, Germany<br />

12:15 Networking lunch<br />

Specialist session: Meeting room I<br />

MANGANESE<br />

14:00 Chairman’s opening remarks<br />

Anne Tremblay, Executive Director,<br />

International Manganese Institute, France<br />

14:15 Manganese market dynamics – focus on steel performance and<br />

impact of inventory levels in Asia<br />

• Performance of downstream steel industry, who is growing, contracting etc.?<br />

• Mn alloy supply and demand balance – why are the alloy<br />

prices underperforming?<br />

• Major producers retreat from costly SiMn – why is capacity being removed?<br />

• Global trade flows of <strong>alloys</strong> in comparison to Mn ore<br />

• Performance of major miners and their inventory levels<br />

• Ore imports and port stocks in China – are they telling us anything?<br />

• India ore imports – is the new tiger being born?<br />

Mark Camaj, Market Research Manager,<br />

International Manganese Institute, France<br />

14:45 New manganese smelting capacity and – where will the <strong>alloys</strong><br />

come from in the future?<br />

• Has India replaced China as an exporter? What is the forecast for the long<br />

term prospects?<br />

• Manganese <strong>alloys</strong> production in Asia and Africa, who can be the next star<br />

performer? Indonesia, Korea or the Middle East?<br />

• The situation in Europe, will the Ukraine reach the top of their game and<br />

beat the Asian producers in the race to be the main supplier?<br />

• Focus on beneficiation in South East Asia – will the region bring more<br />

investments into smelting projects? Would the global producers be<br />

prepared to get involved?<br />

• What would be the cost curve of the <strong>alloys</strong> produced, would it hurt low cost<br />

producers like India?<br />

• Correlation to China – will the domestic consumption levels and prices stay<br />

low? How will it affect the global markets?<br />

• SiMn vs high carbon ferro-manganese in China – will the current low prices<br />

of energy continue to support silicon-manganese?<br />

Kevin Fowkes, Managing Consultant, Alloys Consult, UK<br />

15:15 Networking coffee break<br />

15:45 Focus on South Africa: will new capacities in the Kalahari basin<br />

really materialize?<br />

• Significant increase in prices of manganese as a reason for the new start<br />

ups – will they materialize in the current market situation?<br />

• Constraints on the sustained growth – will South Africa overcome its<br />

logistical problems and give a clear way for the new deposits to flourish?<br />

• What will be the cost of the new manganese capacity? Will it make South<br />

African ore the most competitive or the least competitive?<br />

• What will happen with the extra manganese ore capacity – will it be<br />

beneficiated or exported?<br />

David Wellbeloved, Technical Director, Asia Minerals, South Africa<br />

16:15 Regulatory affairs and manganese ore shipments – what will<br />

change in the near future and how will it affect the industry?<br />

• Influence of REACH on the worldwide regulations – how does it affect the<br />

industry, will its impact increase in the coming years?<br />

• The GHS system as an attempt to harmonise worldwide classification and<br />

labelling of substances<br />

• What will be the impact of GHS System on the shipping of metallic ores and<br />

ferro-<strong>alloys</strong>?<br />

• Timeframe of the new regulations: is the industry ready for changes as<br />

of 2013?<br />

• Will the two year postponement be ratified? Will investment in port facilities<br />

go ahead? Will global trade in ores and <strong>alloys</strong> stop from 1 Jan next year?<br />

Dr Keven Harlow, Regulatory Affairs Manager,<br />

International Manganese Institute, France<br />

16:45 Executives’ Panel discussion: Manganese <strong>alloys</strong> business –<br />

how were they affected by the sluggish steel demand in Europe<br />

and flat market in China?<br />

• Good price level of ore – what is the reason behind it and will it continue for<br />

the next 12 months?<br />

• Impact of shipping prices – why the low cost of logistics didn’t play a vital<br />

part in lowering the prices?<br />

• Why are the prices of <strong>alloys</strong> so volatile, is it due to the shut downs or did<br />

other factors also have a role to play?<br />

• Different reality for different manganese <strong>alloys</strong> – what kind of material kept a<br />

strong position in the past year and which one is set to perform best in the<br />

year to come?<br />

• Will the prices settle according to China?<br />

Arnaud Vigier, Chief Marketing Specialist, Eramet, France<br />

Peter Toth, CEO, OM Holdings, Singapore<br />

Kevin Fowkes, Managing Consultant, Alloys Consult, UK<br />

Anne Tremblay, Executive Director,<br />

International Manganese Institute, France<br />

17:30 Chairman’s closing remarks and drinks reception<br />

19:30 Gala Dinner<br />

Specialist session: Meeting room II<br />

NICKEL<br />

14:00 Chairman’s opening remarks<br />

14:15 Nickel and ferro-nickel pricing volatility – has the market settled<br />

down a bit?<br />

• Has the interest from investors and speculators materialised in the nickel<br />

market this year? Is the market still liquid enough?<br />

• Level of inventories – how much material is locked out from the market?<br />

Where has it been accumulating?<br />

• Forecasting LME prices – will they keep going down? Where is the<br />

bottom line?<br />

• Long term contracts vs spot market prices- why is the industry leaning<br />

towards longer term deals? Will the spot pricing eventually achieve previous<br />

or even higher levels?<br />

Angus Staines, Analyst, UBS, UK<br />

<strong>Metal</strong> <strong>Bulletin</strong> Events reserve the right to alter the venue, timings and/or speakers. © <strong>Metal</strong> <strong>Bulletin</strong> Events, part of Euromoney Trading Limited

14:45 Developments of the nickel market in China – will the industry<br />

change to more efficient and cleaner furnaces and NPI supplies?<br />

• Changes in China – will the government continue to implement closures of<br />

the inefficient blast furnaces?<br />

• Electricity as a major cost – is the price of energy going up in China?<br />

With the introduction of the new better quality NPI for the electric arc<br />

furnace, will the margins be significantly squeezed?<br />

• Overview of nickel Pig Iron prices, will they continue to decrease? What will<br />

be the affect on the Chinese producers, will they cut down on production?<br />

• Impact of the Indonesian nickel ore export restrictions on the NPI<br />

production. With generally higher grade ore limitations, will the electric arc<br />

furnace quality find it difficult to replace traditional material?<br />

Andrew Mitchell, Principal Nickel Analyst, Wood Mackenzie, UK<br />

15:15 Networking coffee break<br />

15:45 Outlook on the future of the industry: the most exciting nickel<br />

cycle yet to come?<br />

• Is the market close to a turn?<br />

• Will explosive growth in nickel prices once again occur during this cycle?<br />

• Will “empty nickel project cupboard” result in higher prices for longer? Is<br />

NPI up to the challenge?<br />

Mark Selby, CEO, Royal Nickel Corporation, Canada<br />

16:15 Nickel – creating sustainability in the long term<br />

• Nickel material of the future – current and prospective usage of nickel<br />

• The contributions of nickel to sustainability<br />

• The importance of nickel in future technologies to address global challenges<br />

Dr Mark Minister, Director, Nickel Institute, Belgium<br />

16:45 Executives’ Panel discussion: Supply/demand balance and the<br />

impact of new capacities coming on stream<br />

• Demand/supply balance for nickel is really unclear, how will the new<br />

capacities from the new projects change the scenery of the marketplace?<br />

Will the market fall into oversupply?<br />

• Raising capital for the new projects – is it viable for the new deposits to<br />

come on stream at the current nickel price levels?<br />

• Partnerships with the stainless steel producers on new projects – will more<br />

stainless steel companies get involved, does it make commercial sense?<br />

• Declining quality of ore – what is the way forward for the new deposits,<br />

where to look out for new sources?<br />

Ricardo Godinho, Head of Strategy Nickel, Anglo American, Brazil<br />

Angus Staines, Analyst, UBS, UK<br />

Mark Selby, CEO, Royal Nickel Corporation, Canada<br />

Andrew Mitchell, Principal Nickel Analyst, Wood Mackenzie, UK<br />

17:30 Chairman’s closing remarks and drinks reception<br />

19:30 Gala Dinner<br />

Specialist session: Meeting room III<br />

MOLYBDENUM<br />

VANADIUM<br />

14:00 Chairman’s opening remarks<br />

14:10 Accessing molybdenum demand in China – what will be the<br />

implications for the global market and prices?<br />

• Demand level in China – will it continue to slow down? What about<br />

inventories – is the demand covered up by high stocks?<br />

• Slower spot market, will the situation continue? What impact will it have on<br />

inventories and prices?<br />

• More steel capacity in India – can it make up for the sluggish Chinese demand?<br />

• WTO objection towards molybdenum Chinese mining quotas and tax<br />

issues – will it keep this market flat?<br />

Catherine M. Virga, Director of Research, CPM Group, USA<br />

14:35 Development of new molybdenum sources – is there a<br />

sustainable solution for the long term supplies?<br />

• What is the market supply/demand forecast?<br />

• What is the molybdenum price forecast beyond 2015?<br />

• Industry cost structure – do new projects provide a suitable future for<br />

the industry?<br />

• What is the growing (and essential) role of primary producers in the market?<br />

• What is the new projects financing strategy in an effectively non-hedgeable<br />

commodity? Will it be difficult to come on stream with the primary projects<br />

at the current price level of molybdenum?<br />

• An overview of Avanti Mining and the Kitsault Project<br />

Craig Nelson, CEO, Avanti Mining, Canada<br />

16:00 Executives’ Panel discussion: Long term demand for molybdenum<br />

in the steel sector, is the long time growth sustained?<br />

• What was the real impact of the steel mills closures in Europe on<br />

molybdenum demand?<br />

• Is the demand from the construction sector still keeping molybdenum<br />

consumption on the rise?<br />

• Recent recovery of the US construction sector – will the situation be<br />

repeated in Europe soon?<br />

• When will consumption outgrow production and what price pressures will<br />

it present?<br />

Kevin Loughrey, CEO, Thompson Creek Company, US<br />

Craig Nelson, CEO, Avanti Mining, Canada<br />

Catherine M. Virga, Director of Research, CPM Group, USA<br />

Andreas Keller, Vice President, Scandinavian Steel, Sweden<br />

16:30 Networking coffee break<br />

17:00 Demand for vanadium – how is the new rebar grade 3/4 policy<br />

really impacting this market?<br />

• Vanadium supplies in China – is the market in balance?<br />

• How are construction trends driving ferro-<strong>alloys</strong> demand in Asia? Why is the<br />

continent looking for better quality material?<br />

• Are those changes in the material specification really being reinforced in<br />

China to get closer to the Western standards?<br />

• Why have neither the prices nor production gone up because of the new<br />

rebar grade 3 usage policy? Will that change in the future and how can it<br />

potentially impact the international market?<br />

• Niobium vs vanadium – what will be the extent of the real impact on those<br />

two materials with the new policy in place?<br />

Jack Bedder, Senior Analyst, Roskill Information Services, UK<br />

17:30 Prices and future supply/demand balance of vanadium<br />

• Outlook on the vanadium prices – has the market finally stabilized?<br />

• Why have the trade flows with China stayed the same even though the new<br />

rebar policy has been introduced? Did the national production of Chinese<br />

vanadium increase?<br />

• Supply/demand balance at this price is good, will more material be brought<br />

to the market soon?<br />

• Demand from the steel and batteries sector – which sectors will be growing<br />

fastest and where?<br />

Terry Perles, President, TTP Squared, USA<br />

18:00 Chairman’s closing remarks and drinks reception<br />

19:30 Gala Dinner<br />

Day two:<br />

Tuesday 13 November 2012<br />

Plenary session: Meeting room I<br />

Future of the ferro-<strong>alloys</strong> business in the<br />

tough economic times continued...<br />

09:00 Chairman’s opening remarks<br />

09:05 Overview of the ferro-<strong>alloys</strong> marketplace – is there light at the<br />

end of the tunnel?<br />

• Uncertainty in the business associated to the European economic<br />

downturn – what was the real impact on the ferro-<strong>alloys</strong> industry?<br />

• Focus on pricing: did the pattern follow general volatility in the market?<br />

• Why did the spot market shrink, will it come back to previous volumes?<br />

• Outlook on supply/demand balance – is there an oversupply? How are<br />

producers adjusting to this challenge?<br />

• How will it affect medium and small players, will there be need<br />

for consolidation?<br />

Hanré Rossouw, CFO, Xstrata Alloys, South Africa<br />

09:35 Stainless and special steels focus – difficult year behind us,<br />

hopeful year ahead of us?<br />

• Stainless steel output – which regions were impacted by the reductions and<br />

where have we seen growth?<br />

• Prices and alloy surcharges – are the stainless steel producers still making<br />

healthy margins?<br />

• Reasons for industry consolidation and the impact it has on the ferro-<strong>alloys</strong><br />

producers, will the stronger consumer mean weaker supplier?<br />

• Sourcing ferro-<strong>alloys</strong> to the stainless steel market: benchmark vs spot<br />

market – view on the future from the end user perspective<br />

Clemens Iller, CEO, Inoxum, Germany<br />

10:05 Economy and steel – what was the correlation in the past and<br />

what will it be in the future?<br />

• How likely is Europe to recover and re-install their purchasing power?<br />

• What will be the effect on the industries – will North and South Europe fall<br />

into deeper division?<br />

• Global trade and the effect of the economic downturn – have we seen the<br />

flows changing?<br />

• China – does the growth remain suppressed? What is the outlook on the<br />

industrial growth and consumer confidence in Asia? How will it affect the<br />

rest of the world?<br />

Steven G. Szakaly, Corporate Economist,<br />

Cliffs Natural Resources Inc, USA<br />

10:35 Networking coffee break

Specialist session: Meeting room I<br />

CHROME<br />

11:00 Chairman’s opening remarks<br />

11:05 Global outlook on the supply/demand balance of chrome and<br />

ferro-chrome market<br />

• Did the recent shut downs of capacity in South Africa really affect the<br />

market? What will happen if South Africa gets stuck?<br />

• High carbon ferro-chrome is going to longer term contracts, why is<br />

no-one is interested in spot? Is it due to limited number of suppliers or<br />

the market volatility?<br />

• Is there an oversupply in the ferro-chrome market at the moment with the<br />

sluggish stainless steel demand? What is the outlook for the future and<br />

what is the trigger to change this situation?<br />

• Is the current supply/demand balance supportive of the price increase in<br />

the long term?<br />

Robert Yuksel Yildrim, President & Chief Executive Officer,<br />

Eti Krom, Turkey<br />

11:35 Changes in the chrome ore beneficiation policy – what will<br />

really happen in South Africa and how will it affect the<br />

global picture?<br />

• Export tax on chrome ore – why is it being considered? Does the<br />

chrome ore market need state intervention?<br />

• Is beneficiation really at the heart of an argument? How to beneficiate<br />

when you don’t have the energy?<br />

• Chinese imports of chrome ore – what will be the long term effect on<br />

South African and global ferro-chrome producers?<br />

• What will be the impact of the chrome ore tax on non integrated chrome<br />

ore producers – will it push South African producers out of the picture?<br />

Will the customers shift to Kazakhstan and Turkey?<br />

Dr Alistair Ruiters, CEO, Ruuki SA, South Africa*<br />

12:05 Energy efficiency: does responsible energy<br />

management need to become an integral part of the<br />

ferro-chrome business?<br />

• Energy cost in the final price – how important are the sustainable energy<br />

sources? Which region hosts the most competitive rates?<br />

• Securing energy supplies, what are the alternative energy solutions that<br />

could be used?<br />

• Carbon tax – why has it caused a lot of volatility in the USA? What are<br />

the implications for the ferro-<strong>alloys</strong> producers in Australia? What lesson<br />

can be drawn for the ferro-chrome industry?<br />

• Co-generation plants as an answer to industry problems? What could be<br />

the commercial benefit?<br />

Conan Jones, Sub Sahara Africa – Area Sales Leader,<br />

GE Energy, South Africa<br />

12:30 Executives’ panel discussion: Supply/demand balance in<br />

the chrome and ferro-chrome markets – are we heading<br />

towards oversupply?<br />

• <strong>Ferro</strong>-chrome vs chrome – what impact has the recent decrease of<br />

capacity in South Africa had on the international balance?<br />

• Consolidation of the stainless steel industry – how will it affect the future<br />

ferro-chrome sourcing?<br />

• European stainless steel market – why there is still an overcapacity in<br />

stainless steel production? Is Europe the only region doing badly?<br />

Where is production of stainless steel increasing?<br />

• With increased demand from China, will the benchmark negotiation<br />

system go out of fashion? What will happen to the alloy surcharge, will<br />

the industry decide to drop them in the future?<br />

• Supply/demand balance- will the market support growth of prices in the<br />

near future?<br />

Mark Midgley, Sales and Marketing Director, ENRC, Kazakhstan<br />

Robert Yuksel Yildrim, President & Chief Executive Officer,<br />

Eti Krom, Turkey<br />

Mauri Kauppi, General Manager – Sales & Marketing,<br />

Outokumpu Chrome Oy, Finland<br />

Conan Jones, Sub Sahara Africa – Area Sales Leader,<br />

GE Energy, South Africa<br />

13:15 Chairman’s closing remarks and networking lunch<br />

Specialist session: Meeting room II<br />

JUNIOR MINERS SHOWCASE<br />

& SILICON<br />

11:00 Overview of the new mining projects in all major ferro-<strong>alloys</strong><br />

ores: Chrome, Manganese, Nickel, Silicon, Molybdenum,<br />

Vanadium, Niobium<br />

SILICON<br />

12:00 Supply/demand balance for ferro-silicon and the outlook for<br />

demand from the crude steel sector<br />

• Whilst demand for flat steel is still strong in the automotive sector, what is<br />

the outlook for construction material?<br />

• What is the outlook on the global crude steel output at the moment and<br />

how is it likely to shape up in the year to come?<br />

• Supply/demand balance of ferro-silicon- is the production growing<br />

enough to sustain the demand in the long term? Are producers looking<br />

to increase their capacities?<br />

Amy Bennett, Principal Consultant, <strong>Metal</strong> <strong>Bulletin</strong> Research, USA<br />

12:30 Silicon and ferro-silicon market in China – how will the shut<br />

downs of capacity effect the international market balance?<br />

• Outlook on Chinese ferro-siliicon supplies – domestic output vs exports<br />

volumes, why are there discrepancies in numbers?<br />

• Has the shortage of Chinese material boosted new silicon and<br />

ferro-silicon capacity elsewhere?<br />

• Chinese ferro-silicon prices – will the market prices stay low in<br />

comparison to the European producers? Contracts vs spot market – how<br />

did the move towards shorter term deals impact market prices?<br />

• Chinese consumption – will the low performance of the past year<br />

continue into the future leaving the market oversupplied due to high<br />

export duty?<br />

• What is the long term outlook – when will Asia ask for more specialist<br />

steel, giving silicon a boost?<br />

• China as a net exporter? How much material still leaves the country<br />

avoiding the high export duties?<br />

Kevin Fowkes, Managing Consultant, Alloys consult, UK<br />

13:00 Chairman’s closing remarks and networking lunch<br />

Specialist session: Meeting room III<br />

MINOR METALS<br />

11:00 Chairman’s opening remarks<br />

11:10 <strong>Ferro</strong>-niobium – still a critical additive in the production of<br />

sophisticated steels?<br />

• Is demand for niobium going up? Which regions are continuously<br />

developing more appetite for specialist steel with ferro-niobium content?<br />

• Vehicle production as a main driver for more niobium consumption:<br />

can niobium save the environment?<br />

• What is the suppy/demand balance in the market, is there enough<br />

capacity to sustain steel applications?<br />

Sergio Castanho, Managing Director Mineracao Catalao,<br />

Anglo American, Brazil<br />

11:40 Tungsten market in China – will it continue to dominate?<br />

What could be the alternatives?<br />

• Is China still at the forefront of tungsten production? What is the outlook<br />

for the prices?<br />

• Global consumption of tungsten and prospects for Chinese demand<br />

growth – is there a correlation in the consumption trend?<br />

• Review of the tungsten export quotas – what is the outlook for the future?<br />

Did the government crackdown on illegal smuggling?<br />

12:05 Overview of cobalt market dynamics – what dictated the<br />

market performance in the past year?<br />

• Review of price volatility – will the market settle down soon? What were<br />

the main factors dragging prices down?<br />

• Supply/demand balance – which regions are growing fastest and where<br />

are producers facing the biggest challenges?<br />

• Potential for new capacities – will new projects come on line soon?<br />

• Asian interest in cobalt – is Africa the next stop for Chinese investments?<br />

Scott Bending, Director, Formation <strong>Metal</strong>s, Canada<br />

12:35 Titanium-is the market developing in the right direction?<br />

• Is the consumption growing in-line with demand? Are the developed<br />

economies still consuming the largest volumes in the consumer<br />

goods sector?<br />

• Will the low scrap prices and high levels of availability still be<br />

undermining alloy producers in the upcoming year? Will the prices<br />

reach record low?<br />

• Potential for new supplies – will we see more material coming on<br />

stream soon?<br />

13:00 Chairman’s closing remarks and networking lunch<br />

*Subject to final confirmation

Enhanced networking environment<br />

Features this year<br />

l Intuitive colour coded badges for each ferro-alloy interest<br />

With over 1000 people in the conference halls and lounges it can be difficult to work out which delegates<br />

are interested in which ferro-<strong>alloys</strong>. Our new colour coding system will streamline the process – a quick glance<br />

at a badge will tell you the relevance to your business - meaning you only spend time networking with<br />

relevant companies.<br />

l Speed networking sessions arranged for each ferro-alloy<br />

Dedicated ‘speed dating’ sessions for each alloy have been included this year. Each session is designed to<br />

separate out the <strong>alloys</strong> and give you a chance to meet lots of relevant people in one go, in the easy<br />

environment of a speed session. Champagne will be served throughout to keep the room flowing.<br />

l Gala dinner for all delegates<br />

Back by popular demand there will be a full gala dinner on the 12th November and it will be open to all<br />

delegates. Spouses are welcome too but spaces will be capped at 400 so reserve your space early.<br />

l All new business lounge in addition to last years’<br />

With the hugely popular business lounge last year jam packed with meetings, we have added a second<br />

dedicated meeting space to give you more room.<br />

l A Bavarian Oktoberfest (in Berlin in November)<br />

Breaking with just about all the traditions of the festival we are hosting our own ‘Oktoberfest’ in November.<br />

Wrong region, wrong time of year but still the same great beer and sausages.<br />

l Early activation of the Delegate Messenger Service<br />

By request we will be activating the delegate messenger service earlier than usual this year to allow you to set<br />

up and prepare your meeting schedule in advance.<br />

Who should attend?<br />

l Miners<br />

l <strong>Ferro</strong>-<strong>alloys</strong> producers<br />

l <strong>Ferro</strong>-<strong>alloys</strong> traders<br />

Conference layout<br />

l Steel mill<br />

ferro-<strong>alloys</strong> buyers<br />

l Logistics service providers<br />

l Finance providers<br />

l Industry consultants<br />

l Equipment providers<br />

ADDITIONAL<br />

BUSINESS<br />

LOUNGE<br />

THIS YEAR

If your details above are incorrect please amend them here<br />

PLEASE COMPLETE IN BLOCK CAPITALS<br />

(Mr/Miss/Mrs/Ms/Dr)<br />

Family Name:<br />

First/Given Name:<br />

*Delegate Email:<br />

*Administrator Email:<br />

Position in Company:<br />

Company Name:<br />

Address:<br />

Postal/Zip Code:<br />

Country:<br />

Tel: +<br />

Fax: +<br />

Please indicate your metals interest in order of preference:<br />

1 2 3<br />

What is your company’s main business activity:<br />

MB STORE<br />

28th International <strong>Ferro</strong>-<strong>alloys</strong><br />

Conference 11-13 November 2012<br />

InterContinental Berlin, Germany<br />

*Delegates must provide their email address in order to receive booking confirmation and access to the<br />

delegate messenger system.<br />

DATA PROTECTION NOTICE<br />

The information you provide on this form will be used by Euromoney Trading Ltd and its group companies (“we” or “us”) to process<br />

your order and deliver the relevant products/services. We may also monitor your use of the website(s) relating to your order, including<br />

information you post and actions you take, to improve our services and track compliance with our terms of use. Except to the extent<br />

you indicate your objection below, we may also use your data (including data obtained from monitoring) (a) to keep you informed of<br />

our products and services; (b) occasionally to allow companies outside our group to contact you with details of their<br />

products/services; or (c) for our journalists to contact you for research purposes. As an international group, we may transfer your data<br />

on a global basis for the purposes indicated above, including to countries which may not provide the same level of protection to<br />

personal data as within the European Union. By submitting this order, you will be indicating your consent to the use of your data as<br />

identified above. Further detail on our use of your personal data is set out in our privacy policy, which is available at<br />

www.euromoneyplc.com or can be provided to you separately upon request.<br />

If you object to contact by telephone , fax , or email , or post , please tick the relevant box. If you do not want us to share your<br />

information with our journalists , or other companies please tick the relevant box.<br />

BOOKING CONDITIONS<br />

Registrations can only be confirmed upon receipt of payment or proof of payment and discounted fees will only apply when payment<br />

is received within the offer period. If you are not able to attend, a substitute delegate will be accepted. Cancellations must be received<br />

in writing 28 days prior to the event to qualify for a full refund less €200 administration fee. It may be necessary for reasons beyond<br />

the control of the organisers to alter the content, timing and venue. In the unlikely event of the conference being cancelled or curtailed<br />

due to any reason beyond the control of <strong>Metal</strong> <strong>Bulletin</strong> Ltd., or it being necessary or advisable to relocate or change the date and/or<br />

location of the event, neither <strong>Metal</strong> <strong>Bulletin</strong> Ltd., nor its employees will be held liable for refunds, damages and/or additional expenses<br />

which may be incurred by delegates. We therefore recommend prospective delegates arrange appropriate insurance cover.<br />

REGISTRATION RATES<br />

Full Standard Rate<br />

1 delegate €2,099<br />

2 delegates €1,799 per delegate<br />

3 delegates €1,499 per delegate<br />

4 delegates €1,399 per delegate<br />

5 delegates €1,299 per delegate<br />

6 delegates €1,249 per delegate<br />

7 delegates €1,213 per delegate<br />

8 delegates €1,074 per delegate<br />

9 delegates €1,055 per delegate<br />

METHODS OF PAYMENT<br />

PLEASE SIGN THE FORM IN ORDER FOR REGISTRATION TO BE PROCESSED<br />

Signature:<br />

Date:<br />

q To make a payment by credit card, please call +44 (0) 20 7779 8905<br />

or visit www.metalbulletinstore.com to book and pay online<br />

q I would like to pay by bank transfer.<br />

Option only available before 12 October 2012.<br />

Note: Full bank details will be emailed to you with your booking confirmation. When paying by<br />

bank transfer, please ensure that you transfer enough funds to cover the full price of your<br />

purchase, plus any bank charges you may incur.<br />

IMPORTANT: Please make sure you quote your full invoice number, details can be found on<br />

your invoice.<br />

<strong>Metal</strong> <strong>Bulletin</strong> standard terms and conditions apply.<br />

Visas are the responsibility of delegates<br />

Fees: The conference fee includes attendance at all sessions, refreshments, welcome reception<br />

and lunches.<br />

Accommodation: The fee does not include accommodation. A limited allocation of rooms has<br />

been reserved at the conference hotel. Delegates will be sent an accommodation booking form<br />

along with confirmation of registration. This form should be completed and returned to the hotel.<br />

VAT: If your organisation is tax registered within the European Union please provide your company<br />

VAT number:<br />

Our VAT Number is GB 243 31 57 84<br />

Please tick if you are not registered for sales tax.<br />

EASY WAYS TO REGISTER<br />

Contact: Roger Cooke<br />

Online: www.metalbulletinstore.com<br />

Tel: +44 (0) 20 7779 8905<br />

Fax: +44 (0) 20 7779 5200<br />

Email: mbstore@metalbulletin.com<br />

Address: <strong>Metal</strong> <strong>Bulletin</strong> Events, Nestor House,<br />

Playhouse Yard, London, EC4V 5EX, UK<br />

VENUE<br />

Intercontinental Berlin, Germany<br />

Reduced room rates – please book early to avoid<br />

disappointment as there are only a limited amount of rooms<br />

available at this rate.<br />

Address:<br />

INTERCONTINENTAL BERLIN<br />

BUDAPESTER STRASSE 2-3, BERLIN,<br />

10787, GERMANY<br />

Front Desk: +49-30-26020<br />

Fax: +49-30-26022600<br />

Booking your accommodation:<br />

Upon registration, delegates will be emailed an<br />

accommodation booking form along with their confirmation<br />

to be completed and returned direct to the hotel.