REAL ESTATE REPORT - REDI-net.com

REAL ESTATE REPORT - REDI-net.com

REAL ESTATE REPORT - REDI-net.com

- TAGS

- real

- estate

- redi-net.com

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

RERC © <strong>REAL</strong> <strong>ESTATE</strong> <strong>REPORT</strong> - THE NATIONAL <strong>REAL</strong> <strong>ESTATE</strong> AUTHORITY<br />

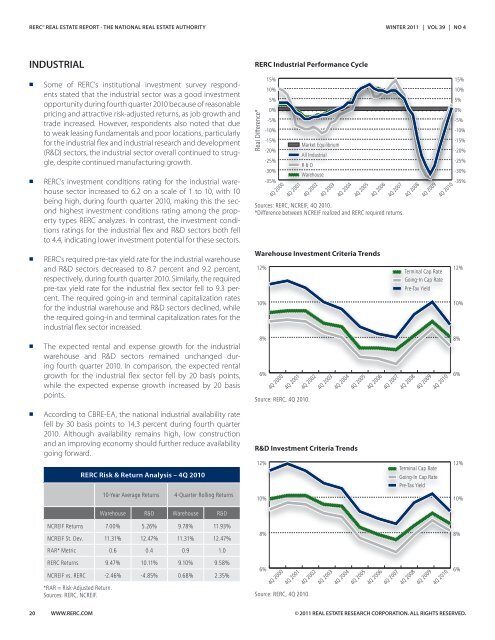

INDUSTRIAL<br />

n Some of RERC’s institutional investment survey respondents<br />

stated that the industrial sector was a good investment<br />

opportunity during fourth quarter 2010 because of reasonable<br />

pricing and attractive risk-adjusted returns, as job growth and<br />

trade increased. However, respondents also noted that due<br />

to weak leasing fundamentals and poor locations, particularly<br />

for the industrial flex and industrial research and development<br />

(R&D) sectors, the industrial sector overall continued to struggle,<br />

despite continued manufacturing growth.<br />

n RERC’s investment conditions rating for the industrial warehouse<br />

sector increased to 6.2 on a scale of 1 to 10, with 10<br />

being high, during fourth quarter 2010, making this the second<br />

highest investment conditions rating among the property<br />

types RERC analyzes. In contrast, the investment conditions<br />

ratings for the industrial flex and R&D sectors both fell<br />

to 4.4, indicating lower investment potential for these sectors.<br />

n RERC’s required pre-tax yield rate for the industrial warehouse<br />

and R&D sectors decreased to 8.7 percent and 9.2 percent,<br />

respectively, during fourth quarter 2010. Similarly, the required<br />

pre-tax yield rate for the industrial flex sector fell to 9.3 percent.<br />

The required going-in and terminal capitalization rates<br />

for the industrial warehouse and R&D sectors declined, while<br />

the required going-in and terminal capitalization rates for the<br />

industrial flex sector increased.<br />

n The expected rental and expense growth for the industrial<br />

warehouse and R&D sectors remained unchanged during<br />

fourth quarter 2010. In <strong>com</strong>parison, the expected rental<br />

growth for the industrial flex sector fell by 20 basis points,<br />

while the expected expense growth increased by 20 basis<br />

points.<br />

n According to CBRE-EA, the national industrial availability rate<br />

fell by 30 basis points to 14.3 percent during fourth quarter<br />

2010. Although availability remains high, low construction<br />

and an improving economy should further reduce availability<br />

going forward.<br />

20 WWW.RERC.COM<br />

RERC Risk & Return Analysis – 4Q 2010<br />

10-Year Average Returns 4-Quarter Rolling Returns<br />

Warehouse R&D Warehouse R&D<br />

NCREIF Returns 7.00% 5.26% 9.78% 11.93%<br />

NCREIF St. Dev. 11.31% 12.47% 11.31% 12.47%<br />

RAR* Metric 0.6 0.4 0.9 1.0<br />

RERC Returns 9.47% 10.11% 9.10% 9.58%<br />

NCREIF vs. RERC -2.46% -4.85% 0.68% 2.35%<br />

*RAR = Risk-Adjusted Return.<br />

Sources: RERC, NCREIF.<br />

RERC Industrial Performance Cycle<br />

Real Difference*<br />

15%<br />

10%<br />

5%<br />

0%<br />

-5%<br />

-10%<br />

-15%<br />

-20%<br />

-25%<br />

-30%<br />

-35%<br />

4Q 2000<br />

4Q 2001<br />

Market Equilibrium<br />

All Industrial<br />

R & D<br />

Warehouse<br />

4Q 2002<br />

4Q 2003<br />

4Q 2004<br />

4Q 2005<br />

4Q 2006<br />

Sources: RERC, NCREIF, 4Q 2010.<br />

*Difference between NCREIF realized and RERC required returns.<br />

Warehouse Investment Criteria Trends<br />

12%<br />

10%<br />

8%<br />

6%<br />

4Q 2000<br />

4Q 2001<br />

Source: RERC, 4Q 2010.<br />

4Q 2002<br />

4Q 2003<br />

4Q 2004<br />

R&D Investment Criteria Trends<br />

12%<br />

10%<br />

8%<br />

6%<br />

4Q 2000<br />

4Q 2001<br />

Source: RERC, 4Q 2010.<br />

4Q 2002<br />

4Q 2003<br />

4Q 2004<br />

4Q 2005<br />

4Q 2005<br />

4Q 2006<br />

4Q 2006<br />

WINTER 2011 | VOL 39 | NO 4<br />

4Q 2007<br />

4Q 2007<br />

4Q 2007<br />

4Q 2008<br />

4Q 2009<br />

Terminal Cap Rate<br />

Going-In Cap Rate<br />

Pre-Tax Yield<br />

4Q 2008<br />

4Q 2009<br />

Terminal Cap Rate<br />

Going-In Cap Rate<br />

Pre-Tax Yield<br />

4Q 2008<br />

4Q 2009<br />

4Q 2010<br />

4Q 2010<br />

4Q 2010<br />

15%<br />

10%<br />

-10%<br />

-15%<br />

-20%<br />

-25%<br />

-30%<br />

-35%<br />

© 2011 <strong>REAL</strong> <strong>ESTATE</strong> RESEARCH CORPORATION. ALL RIGHTS RESERVED.<br />

5%<br />

0%<br />

-5%<br />

12%<br />

10%<br />

8%<br />

6%<br />

12%<br />

10%<br />

8%<br />

6%