Necesidades de ecoinnovación y ecoconstrucción en la edificación

Necesidades de ecoinnovación y ecoconstrucción en la edificación

Necesidades de ecoinnovación y ecoconstrucción en la edificación

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

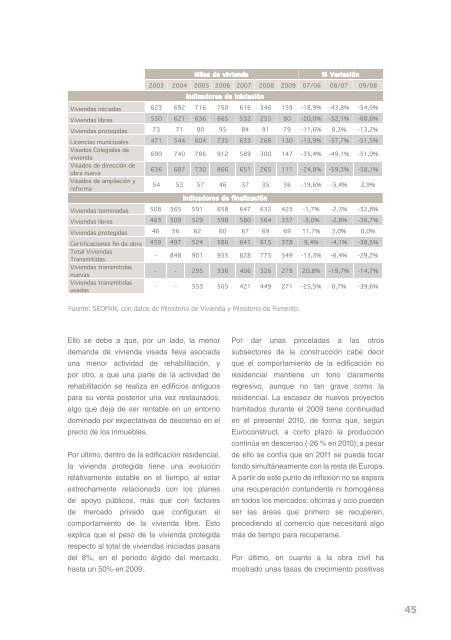

Miles <strong>de</strong> vivi<strong>en</strong>da % Variación<br />

2003 2004 2005 2006 2007 2008 2009 07/06 08/07 09/08<br />

Indicadores <strong>de</strong> iniciación<br />

Vivi<strong>en</strong>das iniciadas 623 692 716 760 616 346 159 -18,9% -43,8% -54,0%<br />

Vivi<strong>en</strong>das libres 550 621 636 665 532 255 80 -20,0% -52,1% -68,6%<br />

Vivi<strong>en</strong>das protegidas 73 71 80 95 84 91 79 -11,6% 8,3% -13,2%<br />

Lic<strong>en</strong>cias municipales 471 544 604 735 633 268 130 -13,9% -57,7% -51,5%<br />

Visados Colegiales <strong>de</strong><br />

vivi<strong>en</strong>da<br />

690 740 786 912 589 300 147 -35,4% -49,1% -51,0%<br />

Visados <strong>de</strong> dirección <strong>de</strong><br />

obra nueva<br />

636 687 730 866 651 265 111 -24,8% -59,3% -58,1%<br />

Visados <strong>de</strong> ampliación y<br />

reforma<br />

54 53 57 46 37 35 36 -19,6% -5,4% 2,9%<br />

Indicadores <strong>de</strong> finalización<br />

Vivi<strong>en</strong>das terminadas 508 565 591 658 647 632 425 -1,7% -2,3% -32,8%<br />

Vivi<strong>en</strong>das libres 463 509 529 598 580 564 357 -3,0% -2,8% -36,7%<br />

Vivi<strong>en</strong>das protegidas 46 56 62 60 67 69 69 11,7% 3,0% 0,0%<br />

Certificaciones fin <strong>de</strong> obra 459 497 524 586 641 615 378 9,4% -4,1% -38,5%<br />

Total Vivi<strong>en</strong>das<br />

Transmitidas<br />

- 848 901 955 828 775 549 -13,3% -6,4% -29,2%<br />

Vivi<strong>en</strong>das transmitidas<br />

nuevas<br />

- - 295 336 406 326 278 20,8% -19,7% -14,7%<br />

Vivi<strong>en</strong>das transmitidas<br />

usadas<br />

- - 553 565 421 449 271 -25,5% 6,7% -39,6%<br />

Fu<strong>en</strong>te: SEOPAN, con datos <strong>de</strong> Ministerio <strong>de</strong> Vivi<strong>en</strong>da y Ministerio <strong>de</strong> Fom<strong>en</strong>to.<br />

Ello se <strong>de</strong>be a que, por un <strong>la</strong>do, <strong>la</strong> m<strong>en</strong>or<br />

<strong>de</strong>manda <strong>de</strong> vivi<strong>en</strong>da visada lleva asociada<br />

una m<strong>en</strong>or actividad <strong>de</strong> rehabilitación, y<br />

por otro, a que una parte <strong>de</strong> <strong>la</strong> actividad <strong>de</strong><br />

rehabilitación se realiza <strong>en</strong> edificios antiguos<br />

para su v<strong>en</strong>ta posterior una vez restaurados,<br />

algo que <strong>de</strong>ja <strong>de</strong> ser r<strong>en</strong>table <strong>en</strong> un <strong>en</strong>torno<br />

dominado por expectativas <strong>de</strong> <strong>de</strong>sc<strong>en</strong>so <strong>en</strong> el<br />

precio <strong>de</strong> los inmuebles.<br />

Por último, <strong>de</strong>ntro <strong>de</strong> <strong>la</strong> <strong>edificación</strong> resi<strong>de</strong>ncial,<br />

<strong>la</strong> vivi<strong>en</strong>da protegida ti<strong>en</strong>e una evolución<br />

re<strong>la</strong>tivam<strong>en</strong>te estable <strong>en</strong> el tiempo, al estar<br />

estrecham<strong>en</strong>te re<strong>la</strong>cionada con los p<strong>la</strong>nes<br />

<strong>de</strong> apoyo públicos, más que con factores<br />

<strong>de</strong> mercado privado que configuran el<br />

comportami<strong>en</strong>to <strong>de</strong> <strong>la</strong> vivi<strong>en</strong>da libre. Esto<br />

explica que el peso <strong>de</strong> <strong>la</strong> vivi<strong>en</strong>da protegida<br />

respecto al total <strong>de</strong> vivi<strong>en</strong>das iniciadas pasara<br />

<strong>de</strong>l 8%, <strong>en</strong> el periodo álgido <strong>de</strong>l mercado,<br />

hasta un 50% <strong>en</strong> 2009..<br />

Por dar unas pince<strong>la</strong>das a <strong>la</strong>s otros<br />

subsectores <strong>de</strong> <strong>la</strong> construcción cabe <strong>de</strong>cir<br />

que el comportami<strong>en</strong>to <strong>de</strong> <strong>la</strong> <strong>edificación</strong> no<br />

resi<strong>de</strong>ncial manti<strong>en</strong>e un tono c<strong>la</strong>ram<strong>en</strong>te<br />

regresivo, aunque no tan grave como <strong>la</strong><br />

resi<strong>de</strong>ncial. La escasez <strong>de</strong> nuevos proyectos<br />

tramitados durante el 2009 ti<strong>en</strong>e continuidad<br />

<strong>en</strong> el pres<strong>en</strong>tel 2010, <strong>de</strong> forma que, según<br />

Euroconstruct, a corto p<strong>la</strong>zo <strong>la</strong> producción<br />

continúa <strong>en</strong> <strong>de</strong>sc<strong>en</strong>so (-26 % <strong>en</strong> 2010); a pesar<br />

<strong>de</strong> ello se confía que <strong>en</strong> 2011 se pueda tocar<br />

fondo simultáneam<strong>en</strong>te con <strong>la</strong> resta <strong>de</strong> Europa.<br />

A partir <strong>de</strong> este punto <strong>de</strong> inflexión no se espera<br />

una recuperación contun<strong>de</strong>nte ni homogénea<br />

<strong>en</strong> todos los mercados: oficinas y ocio pue<strong>de</strong>n<br />

ser <strong>la</strong>s áreas que primero se recuper<strong>en</strong>,<br />

precedi<strong>en</strong>do al comercio que necesitará algo<br />

más <strong>de</strong> tiempo para recuperarse.<br />

Por último, <strong>en</strong> cuanto a <strong>la</strong> obra civil ha<br />

mostrado unas tasas <strong>de</strong> crecimi<strong>en</strong>to positivas<br />

45