plan de negocio

plan de negocio

plan de negocio

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

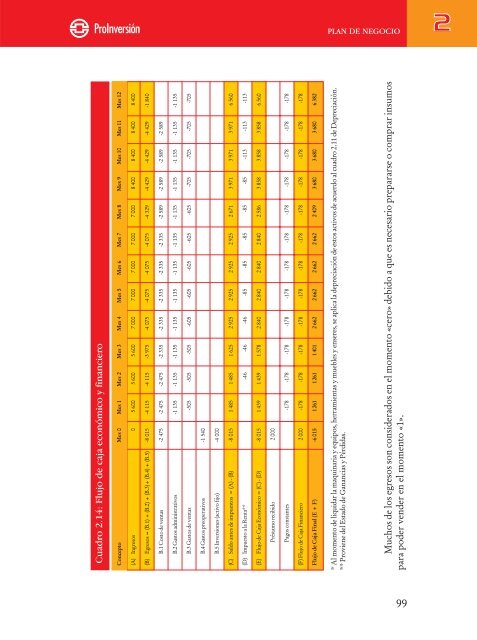

Cuadro 2.14: Flujo <strong>de</strong> caja económico y financiero<br />

Concepto Mes 0 Mes 1 Mes 2 Mes 3 Mes 4 Mes 5 Mes 6 Mes 7 Mes 8 Mes 9 Mes 10 Mes 11 Mes 12<br />

(A) Ingresos 0 5 600 5 600 5 600 7 000 7 000 7 000 7 000 7 000 8 400 8 400 8 400 8 400<br />

(B) Egresos = (B.1) + (B.2) + (B.3)+ (B.4) + (B.5) -8 015 -4 115 -4 115 -3 975 -4 075 -4 075 -4 075 -4 075 -4 329 -4 429 -4 429 -4 429 -1 840<br />

B.1 Costo <strong>de</strong> ventas -2 475 -2 475 -2 475 -2 335 -2 335 -2 335 -2 335 -2 335 -2 589 -2 589 -2 589 -2 589<br />

B.2 Gastos administrativos -1 135 -1 135 -1 135 -1 135 -1 135 -1 135 -1 135 -1 135 -1 135 -1 135 -1 135 -1 135<br />

B.3 Gastos <strong>de</strong> ventas -505 -505 -505 -605 -605 -605 -605 -605 -705 -705 -705 -705<br />

B.4 Gastos preoperativos -1 540<br />

B.5 Inversiones (activo fijo) -4 000<br />

(C) Saldo antes <strong>de</strong> impuestos = (A) - (B) -8 015 1 485 1 485 1 625 2 925 2 925 2 925 2 925 2 671 3 971 3 971 3 971 6 560<br />

(D) Impuesto a la Renta** -46 -46 -46 -85 -85 -85 -85 -85 -113 -113 -113<br />

(E) Flujo <strong>de</strong> Caja Económico = (C) - (D) -8 015 1 439 1 439 1 578 2 840 2 840 2 840 2 840 2 586 3 858 3 858 3 858 6 560<br />

Préstamo recibido 2 000<br />

Pagos constantes -178 -178 -178 -178 -178 -178 -178 -178 -178 -178 -178 -178<br />

(F) Flujo <strong>de</strong> Caja Financiero 2 000 -178 -178 -178 -178 -178 -178 -178 -178 -178 -178 -178 -178<br />

Flujo <strong>de</strong> Caja Final (E + F) -6 015 1 261 1 261 1 401 2 662 2 662 2 662 2 662 2 409 3 680 3 680 3 680 6 382<br />

PLAN DE NEGOCIO<br />

* Al momento <strong>de</strong> liquidar la maquinaria y equipos, herramientas y muebles y enseres, se aplica la <strong>de</strong>preciación <strong>de</strong> estos activos <strong>de</strong> acuerdo al cuadro 2.11 <strong>de</strong> Depreciación.<br />

** Proviene <strong>de</strong>l Estado <strong>de</strong> Ganancias y Pérdidas.<br />

Muchos <strong>de</strong> los egresos son consi<strong>de</strong>rados en el momento «cero» <strong>de</strong>bido a que es necesario prepararse o comprar insumos<br />

para po<strong>de</strong>r ven<strong>de</strong>r en el momento «1».<br />

99