CHAPTER 3 - Educators

CHAPTER 3 - Educators

CHAPTER 3 - Educators

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

100 <strong>CHAPTER</strong> 3/COST-ESTIMATION TECHNIQUES<br />

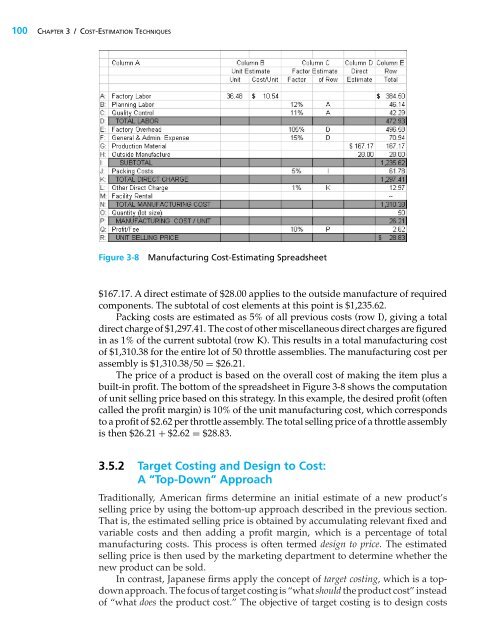

Figure 3-8 Manufacturing Cost-Estimating Spreadsheet<br />

$167.17. A direct estimate of $28.00 applies to the outside manufacture of required<br />

components. The subtotal of cost elements at this point is $1,235.62.<br />

Packing costs are estimated as 5% of all previous costs (row I), giving a total<br />

direct charge of $1,297.41. The cost of other miscellaneous direct charges are figured<br />

in as 1% of the current subtotal (row K). This results in a total manufacturing cost<br />

of $1,310.38 for the entire lot of 50 throttle assemblies. The manufacturing cost per<br />

assembly is $1,310.38/50 = $26.21.<br />

The price of a product is based on the overall cost of making the item plus a<br />

built-in profit. The bottom of the spreadsheet in Figure 3-8 shows the computation<br />

of unit selling price based on this strategy. In this example, the desired profit (often<br />

called the profit margin) is 10% of the unit manufacturing cost, which corresponds<br />

to a profit of $2.62 per throttle assembly. The total selling price of a throttle assembly<br />

is then $26.21 + $2.62 = $28.83.<br />

3.5.2 Target Costing and Design to Cost:<br />

A “Top-Down” Approach<br />

Traditionally, American firms determine an initial estimate of a new product’s<br />

selling price by using the bottom-up approach described in the previous section.<br />

That is, the estimated selling price is obtained by accumulating relevant fixed and<br />

variable costs and then adding a profit margin, which is a percentage of total<br />

manufacturing costs. This process is often termed design to price. The estimated<br />

selling price is then used by the marketing department to determine whether the<br />

new product can be sold.<br />

In contrast, Japanese firms apply the concept of target costing, which is a topdown<br />

approach. The focus of target costing is “what should the product cost” instead<br />

of “what does the product cost.” The objective of target costing is to design costs