The Birth of Insurance Contracts - The Ataturk Institute for Modern ...

The Birth of Insurance Contracts - The Ataturk Institute for Modern ...

The Birth of Insurance Contracts - The Ataturk Institute for Modern ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

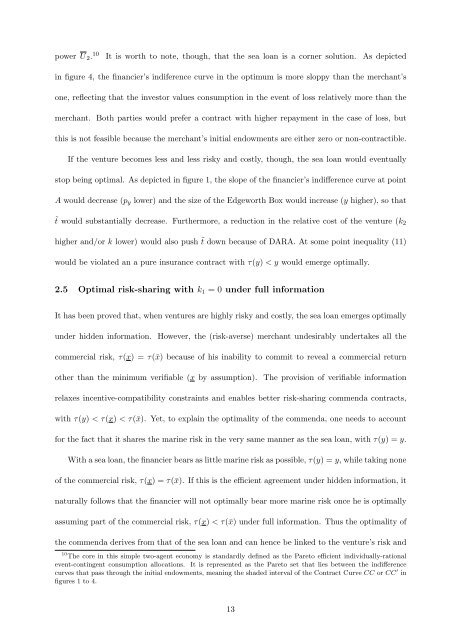

power U 2. 10 It is worth to note, though, that the sea loan is a corner solution. As depicted<br />

in figure 4, the financier’s indiference curve in the optimum is more sloppy than the merchant’s<br />

one, reflecting that the investor values consumption in the event <strong>of</strong> loss relatively more than the<br />

merchant. Both parties would prefer a contract with higher repayment in the case <strong>of</strong> loss, but<br />

this is not feasible because the merchant’s initial endowments are either zero or non-contractible.<br />

If the venture becomes less and less risky and costly, though, the sea loan would eventually<br />

stop being optimal. As depicted in figure 1, the slope <strong>of</strong> the financier’s indifference curve at point<br />

A would decrease (py lower) and the size <strong>of</strong> the Edgeworth Box would increase (y higher), so that<br />

˜t would substantially decrease. Furthermore, a reduction in the relative cost <strong>of</strong> the venture (k2<br />

higher and/or k lower) would also push ˜t down because <strong>of</strong> DARA. At some point inequality (11)<br />

would be violated an a pure insurance contract with τ(y) < y would emerge optimally.<br />

2.5 Optimal risk-sharing with k1 = 0 under full in<strong>for</strong>mation<br />

It has been proved that, when ventures are highly risky and costly, the sea loan emerges optimally<br />

under hidden in<strong>for</strong>mation. However, the (risk-averse) merchant undesirably undertakes all the<br />

commercial risk, τ(x) = τ(¯x) because <strong>of</strong> his inability to commit to reveal a commercial return<br />

other than the minimum verifiable (x by assumption). <strong>The</strong> provision <strong>of</strong> verifiable in<strong>for</strong>mation<br />

relaxes incentive-compatibility constraints and enables better risk-sharing commenda contracts,<br />

with τ(y) < τ(x) < τ(¯x). Yet, to explain the optimality <strong>of</strong> the commenda, one needs to account<br />

<strong>for</strong> the fact that it shares the marine risk in the very same manner as the sea loan, with τ(y) = y.<br />

With a sea loan, the financier bears as little marine risk as possible, τ(y) = y, while taking none<br />

<strong>of</strong> the commercial risk, τ(x) = τ(¯x). If this is the efficient agreement under hidden in<strong>for</strong>mation, it<br />

naturally follows that the financier will not optimally bear more marine risk once he is optimally<br />

assuming part <strong>of</strong> the commercial risk, τ(x) < τ(¯x) under full in<strong>for</strong>mation. Thus the optimality <strong>of</strong><br />

the commenda derives from that <strong>of</strong> the sea loan and can hence be linked to the venture’s risk and<br />

10 <strong>The</strong> core in this simple two-agent economy is standardly defined as the Pareto efficient individually-rational<br />

event-contingent consumption allocations. It is represented as the Pareto set that lies between the indifference<br />

curves that pass through the initial endowments, meaning the shaded interval <strong>of</strong> the Contract Curve CC or CC ′ in<br />

figures 1 to 4.<br />

13