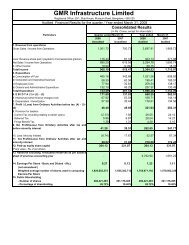

Financial Performance - GMR

Financial Performance - GMR

Financial Performance - GMR

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

<strong>GMR</strong> INFRASTRUCTURE LTD.<br />

FINANCIAL OVERVIEW<br />

OCTOBER 2009<br />

Humility Entrepreneurship Teamwork & Relationships Deliver The Promise Learning Social Responsibility Respect for Individual

Presentation Flow<br />

Page No.<br />

Overview<br />

2<br />

Airports Segment<br />

4<br />

Energy Segment<br />

14<br />

Highways & Urban Infrastructure Segments<br />

20<br />

Consolidated <strong>Financial</strong> <strong>Performance</strong><br />

25

Overview

Leading Infrastructure Developer of India<br />

Infrastructure<br />

Construction Division<br />

Airports<br />

Energy<br />

Highways<br />

Urban<br />

Infrastructure<br />

Indian Businesses<br />

Delhi Airport (Pax Traffic ~ 22.9 mn)<br />

Hyderabad Airport (Pax Traffic ~ 6.2 mn)<br />

Assets in Operation - 823 MW<br />

Assets under Development – 6,808 MW<br />

Assets in Operation - 421 kms<br />

Assets under Development - 210 kms<br />

At Delhi Airport<br />

250 acres for Commercial Development<br />

At Hyderabad Airport<br />

1,000 acres for Commercial Development<br />

250 acres Aviation SEZ<br />

250 acres Logistic SEZ<br />

In Tamil Nadu<br />

3,300 acres SEZ<br />

InterGen N.V.<br />

International Businesses<br />

Istanbul Airport (Pax Traffic ~ 4.4 mn)<br />

Assets in Operation - 7,658 MW<br />

– UK - 2,385 MW<br />

– Mexico - 2,223 MW<br />

– Netherlands - 820 MW<br />

– Philippines - 460 MW<br />

– Australia - 1,770 MW<br />

Assets under Construction - 428 MW<br />

– Netherlands - 428 MW<br />

Island Power<br />

Assets under Development - 800 MW<br />

– Singapore - 800 MW

Airports Segment

Delhi Airport: Developing India’s Largest Airport<br />

ecent Developments<br />

Quarterly Operational <strong>Performance</strong><br />

New Integrated<br />

Terminal (T3)<br />

Passenger (mn)<br />

6.1 5.9 6.2<br />

1.9 2.1<br />

1.8<br />

4.2 3.9 4.5<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

3.4% (1.5%)<br />

(8.6%)<br />

9.8%<br />

6.7%<br />

(4.8%)<br />

Integrated Terminal (T3) – 76% completed as on 30 Sep 09<br />

To be operationalized by March 2010<br />

Domestic Departure Terminal (T1D) operationalized in Apr 2009<br />

10 mn Passenger Capacity added<br />

Airport Development Fees R.s 1,827 bn securitized<br />

JVs signed for Duty-free & F&B Concession in T3<br />

49.9% stake in Duty-free JV with Aer Rianta & Indian Duty<br />

Free Services<br />

40% stake in F&B JVs with Travel Food Services & Devyani<br />

International<br />

Operation Support Period for AAI employees completed<br />

Awarded 29.3 acres of Land Parcels for Commercial<br />

Development<br />

Enhanced flexibility in land usage for 250 acres<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

Cargo (’000 tons)<br />

113.3<br />

99.9<br />

114.4<br />

78.3<br />

69.4<br />

80.1<br />

35.1 30.5 34.4<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

ATMs (’000)<br />

55.4 53.2 57.7<br />

15.4 14.7 14.7<br />

40.0 38.5 43.0<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

Domestic International<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

13.4% (1.0%)<br />

12.7%<br />

14.9%<br />

(2.3%)<br />

<br />

2.0%<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

4.1% (4.0%)<br />

4.8%<br />

3.9%<br />

4.8%<br />

(7.0%)

Delhi Airport: Annual Operational <strong>Performance</strong><br />

1<br />

Passengers (Pax)<br />

2<br />

Air Traffic Movements (ATMs)<br />

CAGR: 16%<br />

CAGR: 16%<br />

(in mn)<br />

(in nos.)<br />

3<br />

Cargo Traffic Movement<br />

Delhi Airport Overview<br />

CAGR: 5%<br />

Terminal 1D<br />

Domestic<br />

International

Delhi Airport: <strong>Financial</strong> <strong>Performance</strong><br />

Rs. mn<br />

1<br />

2<br />

3<br />

Quarterly Results Annual Results<br />

Q4 FY09 Q1 FY10 Q1 FY09 FY 09 FY 08<br />

Gross Revenue 2,391 2,577 2,282 9,476 8,706<br />

Aero Revenue 866 919 898 3,421 3,219<br />

Non Aero Revenue 1,525 1,658 1,384 6,056 5,487<br />

Less: Revenue Share 1,110 1,189 1,059 4,406 4,027<br />

Net Revenue 1,281 1,388 1,223 5,070 4,679<br />

Total Expenditure 1,156 937 1,058 4,444 3,748<br />

EBITDA 125 451 166 626 931<br />

EBITDA margin 5.2% 32.5% 13.5% 12.4% 19.9%<br />

Other Income (20) 7 16 50 48<br />

Interest & Finance Charges 258 327 3 494 5<br />

Depreciation 232 247 23 525 91<br />

PBT (385) (116) 155 (342) 883<br />

Tax (127) (37) 5 (107) 316<br />

PAT (Before Minority Interest) (259) (80) 150 (235) 567<br />

PAT Margin (10.8)% (5.7)% 12.3% (4.6)% 12.1%<br />

Minority Interest (129) (39) 75 (117) 283<br />

PAT (After Minority Interest) (130) (40) 75 (118) 284<br />

Cash Profit (27) 131 173 159 948<br />

1<br />

2<br />

3<br />

Increase in Q1 FY10 Non-Aero revenue (YoY) is mainly due to 1) Increase in Duty-Free revenue due to leasing of additional space;<br />

2) Baggage screening charges for International Terminal initiated in Aug 2008; 3) Additional land leased for Hanger.<br />

Reduction in Q1 FY10 Expenses (YoY) as Operation Support Period for AAI employees was completed in May 2009.<br />

Increase in Q1 FY10 Interest and Depreciation (YoY) due to capitalization of New Runway and Domestic Departure Terminal (T1D)

Hyderabad Airport: India’s First Greenfield Airport Through PPP<br />

Recent Developments<br />

Quarterly Operational <strong>Performance</strong><br />

Passenger (mn)<br />

1.50 1.45<br />

0.42 0.37<br />

1.80<br />

0.40<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

5.8% (13.5%)<br />

11.1%<br />

8.1%<br />

New Terminal<br />

Building<br />

1.13 1.08<br />

1.40<br />

3.9%<br />

(19.5%)<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

10% increase in Aero Charges from 1 Jul 2009;<br />

Includes Landing and Parking Charges<br />

JV for MRO with Malaysian Aerospace Engineering (MAE)<br />

MAE – Certified by 31 National Aviation Authorities Globally<br />

Cargo (’000 tons)<br />

14.0 13.4 14.2<br />

9.1 7.1 8.8<br />

4.9 6.3 5.5<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

4.5% (1.7%)<br />

27.2%<br />

(21.4%)<br />

3.8%<br />

(10.5%)<br />

MoU with CFM International (CFM) to develop Training Center<br />

CFM – Leading Supplier of Engines to Airbus & Boeing<br />

Hyderabad positioned as a “Transshipment Hub”<br />

Appointed Districon as Consultant<br />

ATMs (’000)<br />

20.1 19.6<br />

3.2 3.1<br />

16.9 16.4<br />

22.4<br />

2.6<br />

19.8<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

2.7% (10.2%)<br />

1.3%<br />

3.0%<br />

20.9%<br />

(14.4%)<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

Domestic<br />

International

Hyderabad Airport: Annual Operational <strong>Performance</strong><br />

1<br />

Passengers (PAX)<br />

2<br />

Air Traffic Movements (ATMs)<br />

CAGR: 22%<br />

CAGR: 23%<br />

(in mn)<br />

(in nos.)<br />

3<br />

Cargo Traffic Movement<br />

Hyderabad Airport Overview<br />

CAGR: 12%<br />

Domestic<br />

International

Hyderabad Airport: <strong>Financial</strong> <strong>Performance</strong><br />

Rs. mn<br />

1<br />

Quarterly Results<br />

Annual Results<br />

Q4 FY09 Q1 FY10 Q1 FY09 FY 09<br />

Gross Revenue 1,041 1,132 851 3,859<br />

Aero Revenue 571 630 373 2,058<br />

Non Aero Revenue 470 501 478 1,802<br />

Less: Revenue Share 46 46 34 163<br />

Net Revenue 996 1,086 817 3,696<br />

Total Expenditure 460 502 519 2,266<br />

EBITDA 536 584 298 1,430<br />

EBITDA margin 51% 54% 36% 39%<br />

Other Income 17 16 8 36<br />

Interest & Finance Charges 427 505 301 1,536<br />

Depreciation 319 315 257 1,122<br />

PBT (193) (221) (252) (1,192)<br />

Tax 5 0 4 19<br />

PAT (Before Minority Interest) (187) (221) (256) (1,211)<br />

PAT Margin (18)% (20)% (31)% (33)%<br />

Minority Interest (73) (81) (95) (448)<br />

PAT (After Minority Interest) (114) (139) (161) (763)<br />

Cash Profit 299 94 1 (89)<br />

1<br />

Increase in Q1 FY10 Aero Revenues (YoY) is mainly due to start of collection of User Development Fees (UDF).<br />

UDF collection for International Passengers started from 23 April 08 & for Domestic Passengers started from 22 August 08.

Turkey Airport (ISGIA) : Rapidly Growing Airport<br />

Recent Developments<br />

ISGIA Project on Schedule<br />

New Terminal Building Inauguration scheduled for<br />

31 Oct 2009<br />

New multi-storey car park operationalised in Apr 2009<br />

VIP lounge & Trigen facility to be developed<br />

Quarterly Operational <strong>Performance</strong><br />

Passenger (mn)<br />

1.5<br />

0.5<br />

1.1 1.1<br />

0.3 0.4<br />

1.0 0.8 0.7<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

29.4% 31.8%<br />

45.9% 16.5%<br />

23.0% 40.3%<br />

Financing Secured<br />

Cargo (’000 tons)<br />

19.7<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

2.9% (64.0%)<br />

Master Plan for Development<br />

7.1 6.9<br />

17.6<br />

(27.5%)<br />

(72.0%)<br />

A<br />

D<br />

C<br />

B<br />

A<br />

B<br />

C<br />

D<br />

Existing terminals<br />

New terminal<br />

Car park<br />

Hotel<br />

5.0<br />

2.1 6.9 0.0 2.1<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

ATMs (’000)<br />

11.9<br />

10.0<br />

11.7<br />

4.1<br />

3.6<br />

5.1<br />

7.8 6.4 6.6<br />

0.0%<br />

% Growth<br />

Q-o-Q Y-o-Y<br />

19.0% 1.7%<br />

13.9%<br />

21.9%<br />

(19.6%)<br />

18.2%<br />

Q1 FY 10 Q4 FY 09 Q1 FY 09<br />

Domestic<br />

International

Turkey Airport (ISGIA): <strong>Financial</strong> <strong>Performance</strong><br />

Rs. mn<br />

1<br />

2<br />

Quarterly Results<br />

Annual Results<br />

Q4 FY 09 Q1 FY 10 Q1 FY 09 FY 09<br />

Gross Revenue 365 604 586 2,669<br />

Aero Revenue – – – –<br />

Non Aero Revenue 365 604 586 2,669<br />

Less: Revenue Share – – – –<br />

Net Revenue 365 604 586 2,669<br />

Total Expenditure 414 491 593 2,573<br />

EBITDA (49) 113 (8) 96<br />

EBITDA margin (13)% 18.7% (1.3)% 3.59%<br />

Other Income (90) – – (67)<br />

Interest & Finance Charges (8) 10 17 14<br />

Depreciation 69 148 86 394<br />

PBT (200) (44) (110) (380)<br />

Tax (73) (22) 0 (61)<br />

PAT (Before Minority Interest) (127) (23) (110) (319)<br />

PAT Margin (34.0)% (3.7)% (18.9)% (11.9)%<br />

Cash Profit (58) 106 (24) 13<br />

* All <strong>Financial</strong> Numbers represent GIL’s 40% ownership share<br />

* Q1 FY09 numbers represents results for May 2008 & June 2008 (SGIA assumed control of Project in May 2008)<br />

1<br />

Increase in Q1 FY10 EBITDA (YoY) is mainly due to Revenue mix shift from 1) Increase in higher margin Duty-Free and Passenger Service<br />

Fees revenue; 2) Reduction in lower margin Fuel Sale revenue.<br />

2<br />

Increase in Q1 FY10 Depreciation (YoY) due to capitalization of Car Parking.

Airports Segment: <strong>Financial</strong> <strong>Performance</strong><br />

Rs. mn<br />

Quarterly Results<br />

Annual Results<br />

Q4 FY09 Q1 FY10 Q1 FY09 FY 09 FY 08<br />

Gross Revenue 4,020 4,475 3,862 16,729 8,770<br />

Aero Revenue 1,438 1,549 1,271 5,478 3,238<br />

Non Aero Revenue 2,582 2,897 2,592 11,251 5,532<br />

Mgmt Services 0 29 0<br />

Less: Revenue Share 1,156 1,235 1,093 4,570 4,031<br />

Net Revenue 2,864 3,240 2,769 12,159 4,739<br />

Total Expenditure 2,223 2,067 2,274 9,881 4,380<br />

EBITDA 640 1,174 495 2,278 359<br />

EBITDA margin 15.9% 36.2% 17.9% 18.7% 7.6%<br />

Other Income (75) 18 27 37 91<br />

Interest & Finance Charges 653 836 317 2,036 25<br />

Depreciation 595 722 375 2,077 119<br />

PBT (682) (365) (170) (1797) 307<br />

Tax 202 (54) 14 (120) 317<br />

PAT (Before Minority Interest) (481) (311) (185 (1678) (11)<br />

PAT Margin (11.9)% (9.6)% (6.7)% (13.8)% (0.2)%<br />

Minority Interest (165) (115) 2 (497) 78<br />

PAT (After Minority Interest) (316) (197) (187) (1181) (88)<br />

Cash Profit 114 355 192 204 398

Energy Segment

Click to edit Master title style<br />

Diversified Portfolio of Energy Assets<br />

Project<br />

Recent Developments<br />

Project Pipeline<br />

Vemagiri<br />

Expansion<br />

(768 MW)<br />

<strong>GMR</strong> Energy<br />

(Mangalore)<br />

(235 MW)<br />

768 MW expansion planned<br />

Adequate land available at the site<br />

KG Basin Gas allocation expected<br />

100% of Power on Merchant Tariff<br />

To be relocated to Kakinada by Apr 2010<br />

Gas allocated from KG Basin<br />

9,000<br />

8,000<br />

7,000<br />

6,000<br />

5,000<br />

4,000<br />

3,000<br />

2,000<br />

1,000<br />

0<br />

823<br />

2,418<br />

1,200<br />

2,460<br />

730 7,631<br />

Kamalanga<br />

(1,050 MW)<br />

Achieved financial closure for ~Rs. 45 bn<br />

EPC contract awarded to SEPCO of<br />

China<br />

2009 2012 2013 2014 2015 Ultimate Capac<br />

Chattisgarh<br />

(1,200 MW)<br />

Land acquired<br />

Evaluating bids for BTG and BoP<br />

package<br />

Recommended for coal linkage by CEA 1<br />

Operational <strong>Performance</strong> (PLF)<br />

Q1FY 10 Q4 FY09 Q1 FY09<br />

Acquired 100% stake of Thermal Coal<br />

Plant in Maharashtra<br />

<strong>GMR</strong> Energy<br />

(220 MW)<br />

28 % 90 % 28 %<br />

EMCO<br />

Energy<br />

(600 MW)<br />

Land acquired<br />

Key approvals such as Coal Linkages,<br />

Water Allocation, MOEF 2 Approval<br />

received<br />

Construction to commence in Q4 FY10<br />

<strong>GMR</strong> Power<br />

(200 MW)<br />

Vemagiri<br />

(388 MW)<br />

84 % 78 % 86 %<br />

80 % 39 % 25 %<br />

1 CEA: Central Electricity Authority<br />

2 MOEF: Ministry of Environment and Forestry

Click to edit Master title style<br />

Energy Segment: Quarterly Operational <strong>Performance</strong><br />

Total Portfolio Q1 FY 2010 – 1,202 mn Units<br />

Power Offtake Break-up<br />

Fuel Source Break-up<br />

Merchant,<br />

136 mn Units<br />

11%<br />

Liquid Fuel Plant,<br />

504 mn Units<br />

42%<br />

Contracted,<br />

1,066 mn Units<br />

89%<br />

Gas Plant,<br />

698 mn Units<br />

58%<br />

Vemagiri Power <strong>GMR</strong> Energy <strong>GMR</strong> Power<br />

INR per Unit INR per Unit INR per Unit

Energy Sector: <strong>Financial</strong> <strong>Performance</strong><br />

1<br />

Rs. mn<br />

Quarterly Results<br />

Annual Results<br />

Q4 FY09 Q1 FY10 Q1 FY09 FY 09 FY 08<br />

Gross Revenue 6,537 6,356 5,114 21,527 15,530<br />

Contracted 2,680 4,064 5,071 13,555 15,412<br />

Merchant Sale 2,609 912 – 4,784 –<br />

Power Trading 930 1,308 – 1,320 –<br />

Management Fees 318 72 44 1,868 118<br />

Cost of Fuel 3,723 3,707 3,824 13,450 10,237<br />

Operating Expenses 1,727 1,700 202 2,737 1,794<br />

EBITDA 1,087 949 1,088 5,341 3,499<br />

EBITDA margin 16.5% 14.9% 21.3% 24.8% 22.5%<br />

Other Income 2 31 39 114 511<br />

Interest & Finance Charges (Net) 243 310 217 955 1,065<br />

Depreciation 283 300 293 1,172 1,175<br />

PBT 563 370 617 3,328 1,770<br />

Tax 77 64 77 283 184<br />

PAT (Before Minority Interest) 486 306 540 3,045 1,586<br />

PAT Margin 7.3% 4.8% 10.6% 14.1% 10.2%<br />

Minority Interest 6 95 80 310 276<br />

PAT (After Minority Interest) 480 211 461 2735 1,310<br />

Cash Profit 769 606 833 4,217 2,760<br />

1<br />

Increase in Q1 FY10 Operating Expenses (YoY) due to initiation of Power Trading by <strong>GMR</strong> Energy Trading Ltd. (GETL) in [ ].

Highways & Urban Infrastructure Segments

Highways: Building Paths to Progress<br />

Recent Developments<br />

Highways - Annuity per Month (Rs. mn)<br />

Tindivanam - Ulundurpet commenced<br />

Commercial Operations on 23 Jul 2009<br />

73 kms, 4 lane project on a Toll Basis<br />

Awarded the Hyderabad - Vijaywada project<br />

181 kms, 4 lane project on a Toll Basis<br />

Total estimated outlay of Rs. 22,000 mn<br />

Awarded the Chennai Outer Ring Road project<br />

Highways - Toll Collection per Month (Rs. mn)<br />

30 kms, 6 lane and 2 Service Road on an<br />

Annuity Basis<br />

Total estimated outlay of Rs. 11,000 mn<br />

Shortlisted to submit price bids for 8 Projects<br />

Total estimated outlay of Rs. 99,710 mn

Highways: <strong>Financial</strong> <strong>Performance</strong><br />

Rs. mn<br />

1<br />

Quarterly Results<br />

Annual Results<br />

Q4 FY09 Q1 FY10 Q1 FY 09 FY 09 FY 08<br />

Gross Revenue 464 764 347 1,523 1,397<br />

Annuity Income 365 617 347 1,414 1,397<br />

Toll Collection 99 147 – 109 –<br />

Operating Expenses 70 111 60 266 217<br />

EBITDA 394 653 287 1,257 1,180<br />

EBITDA margin 84.91% 85.5% 82.7% 82.5% 84.5%<br />

Other Income 10 7 5 14.71 1.6<br />

Interest & Finance Charges (Net) 178 379 66 392 273<br />

Depreciation 179 308 113 557 443<br />

PBT 47 (27) 113 322 465<br />

Tax 13 14 13 56 49<br />

PAT (Before Minority Interest) 34 (41) 100 267 417<br />

PAT Margin 7% (5)% 29% 17.52% 29.84%<br />

Minority Interest 38 35 39 163 190<br />

PAT (After Minority Interest) (4) (76) 61 104 227<br />

Cash Profit 213 267 213 824 860<br />

1<br />

Increase in Q1 FY10 Gross Revenue (YoY) due to induction of revenue from Ambala, Jadcherala & Pochanpally Highway Projects.

Urban Infrastructure and Construction<br />

Urban Infrastructure Segment<br />

Construction Division<br />

~50% of 3,300 acres of land acquired for Multi-Product<br />

SEZ in Krishnagiri, Tamil Nadu<br />

SEZ to focus on Biotechnology, IT & ITES,<br />

Electronics & Engineering Industries<br />

Phase-I (around 250 acres) to cost ~Rs. 10 bn<br />

Finalization of MoU to initiate Phase-I<br />

Signed Agreement with SEPCO (Chinese supplier) for<br />

Kamalanga Project in Orrissa<br />

Township Development & Parts of Balance of Plants<br />

Submitted bids for Highway Projects<br />

Hyderabad – Vijaywada & Chennai ORR Projects<br />

Completed Break-water structure at GEL – Barge

Urban Infrastructure & Others: <strong>Financial</strong> <strong>Performance</strong><br />

Rs. mn<br />

Quarterly Results<br />

Annual Results<br />

Q4 FY09 Q1 FY10 Q1 FY09 FY 09 FY 08<br />

Gross Revenue 3,223 1,415 624 4,983 1,282<br />

Income from Investment 338 186 588 1,756 1,098<br />

Operating Income 2,885 1,229 36 3,226 184<br />

Operating Expenses 2,673 979 108 3,188 335<br />

EBITDA 749 436 517 1,794 947<br />

EBITDA margin 23.2% 30.8% 82.8% 36.0% 73.8%<br />

Other Income 56 65 2 45.6 94.1<br />

Interest & Finance Charges (Net) 79 73 89 299 324<br />

Depreciation 47 43 18 93 49<br />

PBT 679 385 412 1,448 668<br />

Tax 296 99 -2 310.9 33.5<br />

PAT (Before Minority Interest) 383 286 414 1,137 634<br />

PAT Margin 11.8% 20.2% 66.3% 22.8% 49.5%<br />

Cash Profit 430 315 419 1,194 673<br />

1<br />

<br />

Increase in Q1 FY10 Operating Income (YoY) due to Income from Construction JV for Turkey Airport Project

Consolidated <strong>Financial</strong> <strong>Performance</strong>

Consolidated Profitability Statement<br />

Rs. mn<br />

Quarterly Results<br />

Annual Results<br />

Q4 FY09 Q1 FY10 Q1 FY09 FY 09 FY 08<br />

Gross Revenue 14,434 13,010 9,948 44,762 26,979<br />

Airports 4,020 4,475 3,862 16,729 8,770<br />

Power 6,528 6,356 5,114 21,527 15,530<br />

Roads 465 764 347 1,523 1,397<br />

Other 3,421 1,415 625 4,981 1,282<br />

Net Revenue 13,278 11,775 8,855 40,192 22,948<br />

Total Expenditure 10,416 8,563 6,468 29,524 16,963<br />

EBITDA 2,862 3,213 2,387 10,668 5,985<br />

EBITDA margin 19.8% 27.3% 27.0% 26.5% 26.1%<br />

Other Income (7) 121 72 214 698<br />

Interest & Finance Charges (Net) 1,152 1598 689 3,682 1,687<br />

Depreciation 1,105 1373 799 3,898 1,785<br />

PBT 598 362 972 3,301 3,210<br />

Tax 186 122 102 530 584<br />

PAT (Before Minority Interest) 412 240 870 2,771 2,627<br />

PAT Margin 2.8% 2.0% 9.8% 6.9% 11.4%<br />

Minority Interest (120) 15 121 (23) 526<br />

PAT (After Minority Interest) 532 225 749 2,794 2,101<br />

Cash Profit 1,517 1,544 1,656 6,438 4,692

Consolidated Balance-Sheet<br />

Rs. mn<br />

Quarterly Results Annual Results<br />

Q1 FY10 Q1 FY09 FY 09 FY 08<br />

Equity 3667 3641 3641 3641<br />

Reserves & Surplus 62740 58415 61070 57531<br />

Minority Interest 17846 13002 18061 11126<br />

Total Networth 84,254 75,059 82,840 72,300<br />

Total Debt 147,870 85,021 120,240 79,770<br />

Secured 126,002 73,453 106,604 68,438<br />

Unsecured 21,872 11,568 13,636 11,332<br />

Deffered Tax Liability 122 413 190 430<br />

Total Liabilities 232,250 160,493 203,270 152,500<br />

Gross Block 119984 70717 114326 66917<br />

Less: Accumulated Depreciation 19003 14933 17809 14218<br />

Net Fixed Assets 100,980 55,784 96,520 52,700<br />

Capital Work in Progress 82,090 57,680 67,910 45,230<br />

Investment 23,366 42,531 14,110 49,000<br />

Cash & Bank Balance 24,495 7,078 23,660 8,940<br />

Net Current Assets 1,319 (2,580) 1,070 (3,370)<br />

Total Assets 232,250 160,493 203,270 152,500

Segment-wise <strong>Financial</strong> <strong>Performance</strong> for Q1 FY2010<br />

Net Revenue<br />

EBITDA<br />

12%<br />

6%<br />

28%<br />

54%<br />

Total = Rs. 11.78 bn<br />

Total = Rs. 3.2 bn<br />

Cash Profit<br />

Capital Employed<br />

Total = Rs. 1.5 bn<br />

Total = Rs. 84.38 bn<br />

Power Airports Highways Others

InterGen: <strong>Financial</strong> <strong>Performance</strong><br />

US$ In Mn<br />

Half yearly Results<br />

Annual Results<br />

H2 CY08 H1 CY09 H1 CY08 CY08 CY 07<br />

Revenue – Proportional 1,152 915 1,017 2,169 1,748<br />

Revenue – Consol 761 602 679 1,440 1,113<br />

EBITDA-Tier I 188 98 241 429 405<br />

EBITDA-Tier II 136 122 78 214 242<br />

Corporate & Development (21) 18 (18) (39) (118)<br />

Consol EBITDA 303 238 301 604 529<br />

Consolidated Debt (Proportional) 4,113 4,298 4,225 3,208 4,090<br />

Proportional Adjusted EBITDA<br />

Tier I<br />

Coryton 75 46 111 186 179<br />

Rocksavage 35 (7) 51 85 83<br />

Spalding 38 52 48 87 73<br />

LaRosita 40 6 31 71 69<br />

Tier II<br />

Rijnmond 49 26 17 66 61<br />

Millmerran 9 12 23 32 32<br />

Callide 1 9 (10) (9) 33<br />

Quezon 38 33 33 71 72<br />

Bijio 26 28 15 40 45<br />

Campeche 9 (12) - 9 -<br />

Chihuahua 4 13 - 4 -<br />

Libramiento 0.9 11 - 0.9 -<br />

1<br />

Decrease in H1 CY09 EBITDA (YoY) due to expected events such as,<br />

1) expiration of Coryton Gas supply contract in 2008; 2) major planned outages combines with weaker spark spread market outcome in 2009;<br />

Positively impacted by events such as 1) acquisition of chihuahua and librammiento acquisition; 2) rebalancing foreign currency hedges

Operating Assets to Drive Revenue Growth<br />

Mar 2009<br />

FY15<br />

Energy<br />

Bajoli Holi<br />

Upper Karnali<br />

Upper Marsyangdi<br />

FY13<br />

Energy<br />

Chhattisgarh<br />

FY14<br />

Energy<br />

Coastal Power<br />

Plants<br />

Alaknanda<br />

Talong<br />

Highways<br />

Hyderabad-Vijayawada<br />

Chennai-Outer ring road<br />

730 MW<br />

FY10<br />

Airport<br />

Delhi T3<br />

Turkey<br />

FY12<br />

Energy<br />

Kamalanga<br />

Vemagiri Expansion<br />

EMCO<br />

1,200 MW<br />

210 kms<br />

2,460 MW<br />

Mar 2015<br />

Airports<br />

(2)<br />

Energy<br />

(13)<br />

Highways<br />

(8)<br />

Intl.<br />

(1)<br />

Highways<br />

Ulundurpet -<br />

Tindivanam<br />

54 mn PAX<br />

73 kms<br />

2,418 MW<br />

72 mn PAX 7,631 MW 631 kms<br />

Hyderabad<br />

Delhi<br />

Coal – 4<br />

Gas – 3<br />

Liquid fuel – 1<br />

Hydro – 5<br />

Annuity–4<br />

Toll–4<br />

25 mn PAX<br />

800 MW<br />

Turkey<br />

Island Power

Asset Growth Over Next Five Years<br />

Assets Under Operations<br />

Assets Under Construction<br />

Capital Outlay : Rs. 90.97 bn;<br />

Equity : Rs. 26.99 bn; Debt : Rs. 63.99 bn<br />

Capital Outlay: Rs. 164.92 bn;<br />

Equity : Rs. 58.93 bn; Debt : Rs. 106.09 bn<br />

Assets Under Development<br />

Total Assets Base<br />

Capital Outlay: Rs. 258.23 bn;<br />

Equity : Rs. 58.3 bn; Debt : Rs. 187.78 bn<br />

Capital Outlay: Rs. 514.12 bn;<br />

Equity : Rs. 144.12 bn; Debt : Rs. 357.86 bn<br />

Power Airports Highways Others

Thank You