Lectures for Part II: Time Series Models in Finance

Lectures for Part II: Time Series Models in Finance

Lectures for Part II: Time Series Models in Finance

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

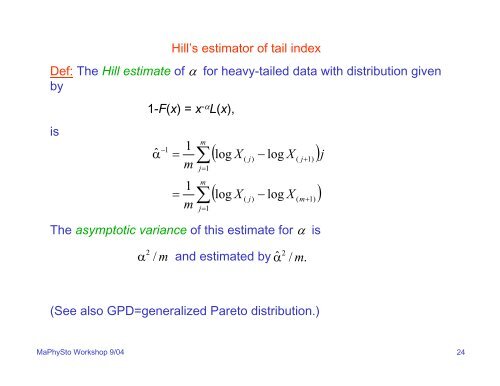

Hill’s estimator of tail <strong>in</strong>dex<br />

Def: The Hill estimate of α <strong>for</strong> heavy-tailed data with distribution given<br />

by<br />

1-F(x) = x -α L(x),<br />

is<br />

αˆ<br />

−1<br />

=<br />

1<br />

m<br />

m<br />

∑( log X<br />

( j)<br />

− log X<br />

( j+<br />

1)<br />

)<br />

j=<br />

1<br />

j<br />

=<br />

1<br />

m<br />

m<br />

∑( log X<br />

( j)<br />

− log X<br />

( m+<br />

1)<br />

)<br />

j=<br />

1<br />

The asymptotic variance of this estimate <strong>for</strong> α is<br />

ˆ 2<br />

2<br />

α / m and estimated by α / m.<br />

(See also GPD=generalized Pareto distribution.)<br />

MaPhySto Workshop 9/04<br />

24