Goldman Sachs Investor Research - Discovery Metals Limited

Goldman Sachs Investor Research - Discovery Metals Limited

Goldman Sachs Investor Research - Discovery Metals Limited

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

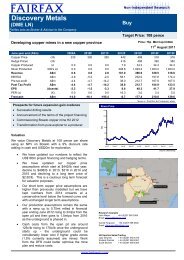

7 October 2010 <strong>Discovery</strong> <strong>Metals</strong> <strong>Limited</strong><br />

Valuation<br />

• As stated previously, we have included the commencement of open pit mining in FY12<br />

and underground mining in FY15. Our base case assumes combined production from<br />

these two sources at a rate of 3mtpa increasing to 3.5mtpa for 15 years out to the<br />

conclusion of FY26. This base case also includes $65m in exploration assets, which is<br />

included to approximate the likelihood of further resource upgrades.<br />

• For our upside case, we have included a 10-year extension to Boseto, which, given the<br />

size of the current resource is feasible, as well as some benefit from a project<br />

development at Dikoloti. This project is clearly early-stage and not the primary focus of<br />

DML at present.<br />

• We have included a summary of our valuation below:<br />

<strong>Discovery</strong> <strong>Metals</strong><br />

DISCOUNTED CASH FLOW VALUATION<br />

Discount Rate Used % 11.7%<br />

Issued Shares millions 313.9<br />

Mines<br />

A$m<br />

$ per share<br />

Boseto (15 Year Mine Life) 385 $1.23<br />

- $0.00<br />

Sub Total Mines 385 $1.23<br />

Exploration Assets 65 $0.21<br />

NPV of Tax (188) ($0.60)<br />

NPV of Hedge Book – $0.00<br />

Net Cash 39 $0.13<br />

Corporate (36) ($0.11)<br />

Franking Credits 7 $0.02<br />

Option Dilution 15 $0.05<br />

Other – $0.00<br />

Sub Total Corporate/Other (98) ($0.31)<br />

NET PRESENT VALUE 287 $0.91<br />

Upside Options<br />

Boseto Extension of Life (10 Years) - post tax 41 $0.13<br />

Dikoloti Ni Project - attributable and post tax 48 $0.15<br />

UPSIDE VALUATION 377 $1.20<br />

Source: GS&PA <strong>Research</strong> estimates<br />

Financing<br />

DML is yet to complete the funding arrangements for the development of Boseto. However,<br />

the company has articulated the desire to use a maximum amount of debt (as high as 60%).<br />

We see some risk to this high level of debt given the experience of a number of junior<br />

development companies that have not only been forced into excessive hedge positions but<br />

have also been precluded from accessing the project cash flow to fund any exploration or<br />

other developments until the debt has been reduced following the commissioning and<br />

financial closure of the project.<br />

We further note that, on our estimates, DML is currently trading above our base NPV and<br />

thus any equity raising (above NPV) is accretive for shareholders.<br />

Based on the current share price and assuming an equity raising of $121m (gross) 40%<br />

debt: 60% equity (a 7.5% discount to the current share price $1.28/share) our base case<br />

valuation increases to $1.01/share.<br />

<strong>Goldman</strong> <strong>Sachs</strong> & Partners Australia<br />

Investment <strong>Research</strong><br />

All figures in A$ unless otherwise advised 16