Goldman Sachs Investor Research - Discovery Metals Limited

Goldman Sachs Investor Research - Discovery Metals Limited

Goldman Sachs Investor Research - Discovery Metals Limited

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

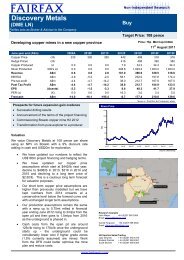

7 October 2010 <strong>Discovery</strong> <strong>Metals</strong> <strong>Limited</strong><br />

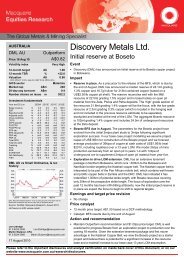

RECOMMENDATION - Our Thinking<br />

RECOMMENDATION:<br />

HOLD<br />

Stock Code: DML Rationale: -ve Neut +ve<br />

Share Price: $ 1.28 Industry Structure: <br />

Valuation: $ 0.91 EVA Trend: <br />

Earnings Momentum:<br />

Catalysts:<br />

Price / Valuation:<br />

<br />

<br />

<br />

We are initiating coverage with a neutral recommendation and a 12-month target price of<br />

$1.50.<br />

Our positive view of copper is driven by our view that the market is moving to an ongoing<br />

deficit which will require a higher copper price, both to allow lower grade and less profitable<br />

greenfield projects to be developed over time and to destroy some demand from those areas<br />

where substitution can take place.<br />

DML controls a significant area of copper mineralisation within the Botswana Kalahari<br />

Copperbelt which is thought to be a continuation of the renowned Zambian Copperbelt.<br />

The geology appears to be well understood and DML is proposing a combined open pit and<br />

underground mining operation and, given the extensive strike continuity of the orebody,<br />

should be able to extend the mine life by progressively adding to the strike extent of mining.<br />

Whilst there has been only limited deeper drilling to date, the nature of the orebody (sharp<br />

geological cut-offs on the F/W and some mineralisation into the H/W) suggest that it will be<br />

amenable to mechanised underground mining at similar (or better) grade than the open pit.<br />

The two key operational risks that we can identify are the average strip ratio 15.9:1 (LOM) in<br />

the development case and the percentages of oxide and transition ore versus sulphide ore<br />

which will impact overall recoveries.<br />

We can identify with a strategy of limiting the open pit depth of mining to lower the waste<br />

stripping and thus LOM strip ratio (but this does mean that there will be a higher percentage<br />

of oxide and transition ore) and increasing the strike extent of the open pit, or more<br />

accurately strip mine, to maintain the overall open pit tonnage.<br />

The second key risk is the cost of actually moving a tonne of material. DML has synthesised a<br />

material movement cost of US$1.35/tonne which we find extremely low but acknowledge<br />

that the strip mining may allow less waste handling, leading to a lowering of waste haul<br />

distances, etc. Nonetheless, this unit cost/tonne is significantly lower than that of any of the<br />

other companies we cover.<br />

Corporate Structure<br />

• <strong>Discovery</strong> <strong>Metals</strong> is listed on the following markets:<br />

• Australian Stock Exchange (ASX: DML) - December 2003<br />

• Botswana Stock Exchange (BSE: DML) - December 2006<br />

• Alternative Investment Market (AIM: DME) - June 2007<br />

• The company has a June year-end and reports in AUD.<br />

<strong>Goldman</strong> <strong>Sachs</strong> & Partners Australia<br />

Investment <strong>Research</strong><br />

All figures in A$ unless otherwise advised 2