Goldman Sachs Investor Research - Discovery Metals Limited

Goldman Sachs Investor Research - Discovery Metals Limited

Goldman Sachs Investor Research - Discovery Metals Limited

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

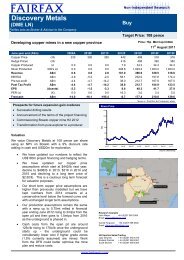

7 October 2010 <strong>Discovery</strong> <strong>Metals</strong> <strong>Limited</strong><br />

Mine Plan<br />

• The BFS released in late August 2010 outlines a mine plan for BCP, which will see it<br />

commence production as an open pit in late 2011. In conjunction with this, DML also<br />

released a development plan, which incorporates additional mineralised material which is<br />

not of sufficient confidence to be promoted to reserves. We have, where applicable,<br />

assumed some material outlined in the development plan as part of our base case. In<br />

effect, we have modelled both open pit and underground mining in our base estimate.<br />

• Our current base case for DML assumes the construction and operation of Boseto open<br />

pit for the initial 3 years followed by the addition of an underground mine from 2015.<br />

Combined production would remain at 3mtpa, increasing to 3.5mtpa (GS&PA estimates)<br />

as operations are optimised with ore being sourced initially equally from the two<br />

operations, but at the expanded rate 2mtpa (open pit) and 1.5mtpa (underground).<br />

• Our key production assumptions compared to the BFS are shown below:<br />

GS&PA<br />

DML<br />

Production Metrics<br />

Annual Production mtpa 3.0 3.0<br />

Strip Ratio waste:ore 15 15<br />

Cu feed grade % 1.5 1.5<br />

Cu recovery % 84.0 84.0<br />

Cu production kt Cu 36.4 36.4<br />

Ag feed grade g/t 20.2 20.2<br />

Ag recovery % 61.0 61.0<br />

Ag production moz 1.1 1.1<br />

Source: Company data, GS&PA <strong>Research</strong> estimates<br />

Capital Cost<br />

DML's pre-feasibility study capital estimate for a 2mtpa plant was US$185m which was<br />

updated in September 2009 to US$150m. More recently, DML has increased the planned<br />

throughput rate from 2mtpa to 3mtpa and advised that the contracted capital cost for the<br />

plant to be ~US$91m and that the total capital cost of construction of the operation at<br />

Boseto will be in the order of US$175m (including contingencies).<br />

A breakdown of these capital costs is included below.<br />

Capital Items<br />

US$m<br />

Process plant - fixed price EPCM 91.2<br />

First fills and spares 10.3<br />

Tailings storage facility 2.7<br />

Diesel power generators 10.7<br />

Roads, offices, workshope, land compensation 13.1<br />

Process and mine control systems 8.0<br />

Village infrastructure 15.5<br />

Temp. Infrastructure 8.7<br />

Owners Team 3.6<br />

Subtotal 163.8<br />

Contigency & escalation 11.2<br />

Total 175.0<br />

Source: Company data<br />

Operating Cost<br />

DML has provided guidance as to its expected operating cost of BCP during the initial start-up<br />

when the project will still have a debt repayment requirement. We have adjusted these as we<br />

see fit. A summary of the operating costs we have used in our estimates versus the BFS is<br />

included below. The key difference that we have allowed for is a higher unit cost for moving<br />

material.<br />

<strong>Goldman</strong> <strong>Sachs</strong> & Partners Australia<br />

Investment <strong>Research</strong><br />

All figures in A$ unless otherwise advised 8