The due diligence process from the underwriter's - Fried Frank

The due diligence process from the underwriter's - Fried Frank

The due diligence process from the underwriter's - Fried Frank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

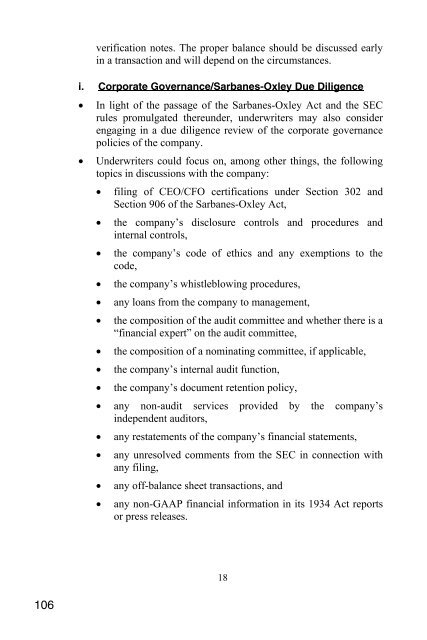

verification notes. <strong>The</strong> proper balance should be discussed early<br />

in a transaction and will depend on <strong>the</strong> circumstances.<br />

i. Corporate Governance/Sarbanes-Oxley Due Diligence<br />

• In light of <strong>the</strong> passage of <strong>the</strong> Sarbanes-Oxley Act and <strong>the</strong> SEC<br />

rules promulgated <strong>the</strong>reunder, underwriters may also consider<br />

engaging in a <strong>due</strong> <strong>diligence</strong> review of <strong>the</strong> corporate governance<br />

policies of <strong>the</strong> company.<br />

• Underwriters could focus on, among o<strong>the</strong>r things, <strong>the</strong> following<br />

topics in discussions with <strong>the</strong> company:<br />

• filing of CEO/CFO certifications under Section 302 and<br />

Section 906 of <strong>the</strong> Sarbanes-Oxley Act,<br />

• <strong>the</strong> company’s disclosure controls and procedures and<br />

internal controls,<br />

• <strong>the</strong> company’s code of ethics and any exemptions to <strong>the</strong><br />

code,<br />

• <strong>the</strong> company’s whistleblowing procedures,<br />

• any loans <strong>from</strong> <strong>the</strong> company to management,<br />

• <strong>the</strong> composition of <strong>the</strong> audit committee and whe<strong>the</strong>r <strong>the</strong>re is a<br />

“financial expert” on <strong>the</strong> audit committee,<br />

• <strong>the</strong> composition of a nominating committee, if applicable,<br />

• <strong>the</strong> company’s internal audit function,<br />

• <strong>the</strong> company’s document retention policy,<br />

• any non-audit services provided by <strong>the</strong> company’s<br />

independent auditors,<br />

• any restatements of <strong>the</strong> company’s financial statements,<br />

• any unresolved comments <strong>from</strong> <strong>the</strong> SEC in connection with<br />

any filing,<br />

• any off-balance sheet transactions, and<br />

• any non-GAAP financial information in its 1934 Act reports<br />

or press releases.<br />

18<br />

106