The due diligence process from the underwriter's - Fried Frank

The due diligence process from the underwriter's - Fried Frank

The due diligence process from the underwriter's - Fried Frank

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

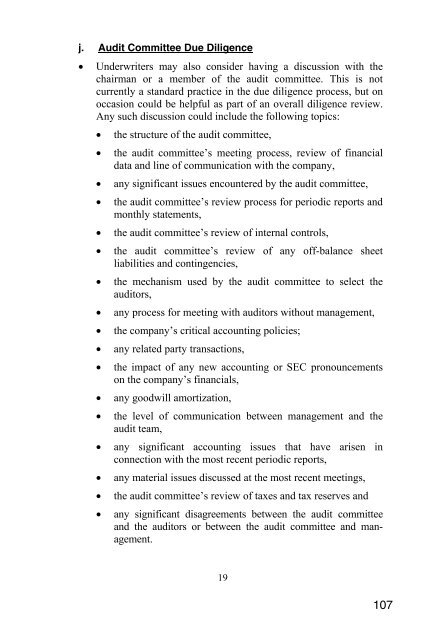

j. Audit Committee Due Diligence<br />

• Underwriters may also consider having a discussion with <strong>the</strong><br />

chairman or a member of <strong>the</strong> audit committee. This is not<br />

currently a standard practice in <strong>the</strong> <strong>due</strong> <strong>diligence</strong> <strong>process</strong>, but on<br />

occasion could be helpful as part of an overall <strong>diligence</strong> review.<br />

Any such discussion could include <strong>the</strong> following topics:<br />

• <strong>the</strong> structure of <strong>the</strong> audit committee,<br />

• <strong>the</strong> audit committee’s meeting <strong>process</strong>, review of financial<br />

data and line of communication with <strong>the</strong> company,<br />

• any significant issues encountered by <strong>the</strong> audit committee,<br />

• <strong>the</strong> audit committee’s review <strong>process</strong> for periodic reports and<br />

monthly statements,<br />

• <strong>the</strong> audit committee’s review of internal controls,<br />

• <strong>the</strong> audit committee’s review of any off-balance sheet<br />

liabilities and contingencies,<br />

• <strong>the</strong> mechanism used by <strong>the</strong> audit committee to select <strong>the</strong><br />

auditors,<br />

• any <strong>process</strong> for meeting with auditors without management,<br />

• <strong>the</strong> company’s critical accounting policies;<br />

• any related party transactions,<br />

• <strong>the</strong> impact of any new accounting or SEC pronouncements<br />

on <strong>the</strong> company’s financials,<br />

• any goodwill amortization,<br />

• <strong>the</strong> level of communication between management and <strong>the</strong><br />

audit team,<br />

• any significant accounting issues that have arisen in<br />

connection with <strong>the</strong> most recent periodic reports,<br />

• any material issues discussed at <strong>the</strong> most recent meetings,<br />

• <strong>the</strong> audit committee’s review of taxes and tax reserves and<br />

• any significant disagreements between <strong>the</strong> audit committee<br />

and <strong>the</strong> auditors or between <strong>the</strong> audit committee and management.<br />

19<br />

107