July - Summer Edition - CI Investments

July - Summer Edition - CI Investments

July - Summer Edition - CI Investments

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

www.ci.com/perspective<br />

<strong>Summer</strong> 2011<br />

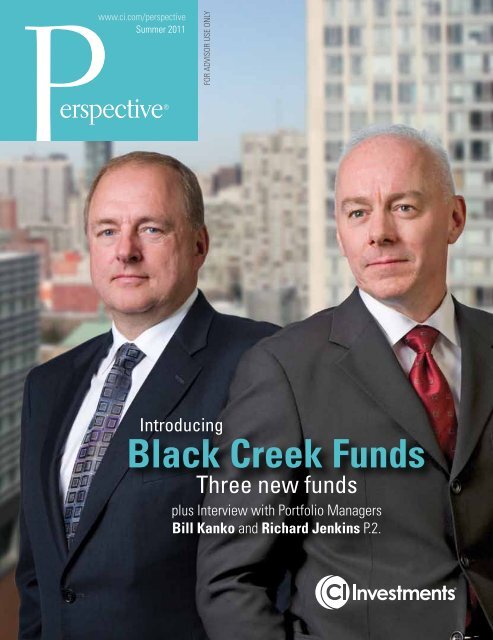

Introducing<br />

Black Creek Funds<br />

Three new funds<br />

plus Interview with Portfolio Managers<br />

Bill Kanko and Richard Jenkins P.2.

Table of contents<br />

Message from Derek J. Green 1<br />

Market Update<br />

Introducing Black Creek Funds 2<br />

Book reviews 7<br />

Portfolio Snapshot – Cambridge Funds 14<br />

Signature Market Roundup 20<br />

Managers’ Commentary 28<br />

<strong>CI</strong> Investment Consulting 28<br />

Black Creek Investment Management 30<br />

Harbour Advisors 32<br />

Cambridge Advisors 34<br />

Tetrem Capital Management Ltd. 35<br />

Scorecard 71<br />

<strong>CI</strong> Corporate Class 72<br />

Signature Funds 73<br />

Harbour Funds ® 73<br />

Synergy Funds 74<br />

<strong>CI</strong> Funds ® 74<br />

Portfolio Series 74<br />

Portfolio Select Series 75<br />

Insight ® Units/Shares 75<br />

Hedge Funds 75<br />

Labour-sponsored Funds 76<br />

<strong>CI</strong> GIFs 77<br />

<strong>CI</strong> Segregated Funds 78<br />

Legacy Segregated Funds ® I & II 78<br />

Clarica MVP Segregated Funds 79<br />

Clarica Portfolio Segregated Funds 80<br />

SunWise ® I 82<br />

SunWise ® II 83<br />

SunWise ® Elite 91<br />

SunWise ® Essential Series 96<br />

<strong>CI</strong> Sales Team 100<br />

Globefund profiles as at June 30, 2011 38<br />

Portfolio Series<br />

Portfolio Series Income Fund 39<br />

Portfolio Series Conservative Fund 40<br />

Portfolio Series Conservative Balanced Fund 41<br />

Portfolio Series Balanced Fund 42<br />

Portfolio Series Balanced Growth Fund 43<br />

Portfolio Series Growth Fund 44<br />

Portfolio Series Maximum Growth Fund 45<br />

Global Equity Funds<br />

Cambridge Global Equity Corporate Class 46<br />

<strong>CI</strong> Global Fund 47<br />

<strong>CI</strong> Global High Dividend Advantage Fund 48<br />

Harbour Foreign Equity Corporate Class 49<br />

Synergy Global Corporate Class 50<br />

<strong>CI</strong> International Value Fund 51<br />

<strong>CI</strong> Emerging Markets Fund 52<br />

American Equity Funds<br />

<strong>CI</strong> American Managers ® Corporate Class 53<br />

<strong>CI</strong> American Value Corporate Class 54<br />

Canadian Equity Funds<br />

Cambridge Canadian Equity Corporate Class 55<br />

<strong>CI</strong> Canadian Investment Fund 56<br />

Harbour Fund 57<br />

Signature Select Canadian Fund 58<br />

Synergy Canadian Corporate Class 59<br />

Balanced Funds<br />

Cambridge Canadian Asset Allocation Corp. Class 60<br />

Harbour Growth & Income Fund 61<br />

Signature Income & Growth Fund 62<br />

Signature Canadian Balanced Fund 63<br />

Industry-specific Funds<br />

Signature Canadian Resource Fund 64<br />

Signature Global Energy Corporate Class 65<br />

Income Funds<br />

Signature Canadian Bond Fund 66<br />

Signature Dividend Fund 67<br />

Signature High Income Fund 68<br />

Signature Diversified Yield Fund 69<br />

Signature Corporate Bond Fund 70<br />

For Advisor Use Only

<strong>Summer</strong> 2011<br />

Dear Advisor,<br />

<strong>CI</strong> <strong>Investments</strong> is pleased<br />

to announce the launch<br />

of the Black Creek<br />

funds, which offer you<br />

the proven investment<br />

expertise of Bill Kanko<br />

and Richard Jenkins of<br />

Black Creek Investment<br />

Management.<br />

The three new funds – Black Creek Global Leaders Corporate<br />

Class, Black Creek International Equity Corporate Class and<br />

Black Creek Global Balanced Corporate Class – provide<br />

you and your clients with compelling new global investment<br />

options at <strong>CI</strong>.<br />

Bill and Richard have consistently produced excellent results<br />

in their long careers as money managers. Since 2006, Black<br />

Creek has managed portfolios for our Castlerock <strong>Investments</strong><br />

affiliate, outperforming their benchmarks and peer group.<br />

The new funds now provide you with access to Black<br />

Creek through the <strong>CI</strong> platform and with the benefits of the<br />

<strong>CI</strong> Corporate Class structure.<br />

The Black Creek managers will use the same successful<br />

approach used with their Castlerock funds. For more<br />

information about the Black Creek team and the new funds,<br />

please see the interview starting on page 2. For current<br />

information on Black Creek’s Castlerock funds, please visit<br />

www.castlerockinvestments.ca.<br />

We believe that this fund launch is especially timely, given that<br />

the Canadian market has performed very well in recent years.<br />

As a result, some client portfolios may be overweight Canada,<br />

requiring an increased allocation to global investments to<br />

enhance diversification and reduce risk.<br />

Consider that during the second quarter, the Canadian stock<br />

market performed significantly worse than the U.S. and broad<br />

global market indexes. The S&P/TSX Composite Index<br />

declined 10% from April to June before rebounding at the<br />

end of June to reduce its quarterly loss to 5.2%. This action<br />

was driven primarily by a pullback in the resource sectors,<br />

which now account for a 50% weighting on the index.<br />

In addition to the Black Creek funds, <strong>CI</strong> offers a rich selection<br />

of global funds, including Signature Select Global Fund,<br />

Harbour Foreign Equity Corporate Class, Cambridge Global<br />

Equity Corporate Class, <strong>CI</strong> Global High Dividend Advantage<br />

Fund and <strong>CI</strong> International Value Fund. Our lineup also<br />

includes globally oriented balanced and income funds, such<br />

as Signature Diversified Yield Fund.<br />

In other news, we have made our first addition to the Harbour<br />

family of funds since 2002 with the launch of Harbour<br />

All Cap Corporate Class. This fund offers the conservative,<br />

value-oriented approach of the Harbour team in a flexible<br />

mandate investing primarily in Canadian companies, with no<br />

restrictions on market capitalization.<br />

Also available now are the Fund Facts documents for <strong>CI</strong>’s<br />

mutual funds. Fund Facts are a regulatory requirement and<br />

provide fund information such as holdings, past performance<br />

and costs of investing. <strong>CI</strong>’s Fund Facts can be accessed<br />

through a link on our home page (under What’s New) or by<br />

going directly to www.fundfacts.com.<br />

The new funds now provide you with<br />

access to Black Creek through the<br />

<strong>CI</strong> platform and with the benefits of<br />

the <strong>CI</strong> Corporate Class structure.<br />

We have other intiatives planned for this fall to help you build<br />

your business. These include a revised investment program<br />

for high net worth clients and extensive information from our<br />

portfolio managers through meetings, roadshows, webcasts<br />

and podcasts.<br />

In the meantime, you can find manager commentary and<br />

other information in this issue of Perspective, as well as on<br />

our website, www.ci.com. And, as always, feel free to contact<br />

your <strong>CI</strong> Sales Team.<br />

Wishing you and your family a safe and enjoyable summer,<br />

Derek J. Green<br />

President<br />

<strong>CI</strong> <strong>Investments</strong><br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 1

Introducing Black Creek<br />

Black Creek Q&A<br />

Introducing Black Creek funds<br />

Black Creek funds – managed by Bill Kanko and<br />

Richard Jenkins – are now available on the <strong>CI</strong><br />

platform. The <strong>CI</strong> Black Creek funds are investing in units<br />

of their equivalent Castlerock funds, so the investment<br />

mandates and underlying portfolios are the same. However,<br />

the <strong>CI</strong> Black Creek funds are part of the <strong>CI</strong> Corporate<br />

Class structure, which provides investors with several tax<br />

advantages. And, by being on the <strong>CI</strong> platform, it is easier for<br />

existing <strong>CI</strong> investors to access the funds.<br />

Black Creek Global Leaders Corporate Class is a<br />

global equity fund with a concentrated portfolio of 20-25<br />

high-quality, globally competitive companies.<br />

Black Creek International Equity Corporate Class<br />

invests in companies domiciled in countries outside of<br />

Canada and the United States, including companies located<br />

in emerging markets. It may also invest in small, medium<br />

and large-cap companies. As with Global Leaders the<br />

portfolio will be concentrated with 20-25 holdings.<br />

The equity portion of Black Creek Global Balanced<br />

Corporate Class invests in a diversified portfolio of<br />

globally competitive companies within growing sectors.<br />

While the debt portion of the fund invests primarily in<br />

government and corporate bonds, it may also include highyield<br />

bonds.<br />

Together, Bill Kanko and Richard Jenkins of<br />

Black Creek Investment Management have<br />

been managing global portfolios for more<br />

than a half a century. Here they discuss their<br />

investment approach that has led to excellent<br />

results in Castlerock Global Leaders Fund,<br />

Castlerock International Equity Fund and<br />

Castlerock Global Balanced Fund<br />

[Q] You stress “unique insights, proprietary ideas” as<br />

part of your investment philosophy. Can you explain?<br />

KANKO: We chose “unique insights, proprietary ideas”<br />

as something that best represents what we do in terms of<br />

investment style and philosophy. There is a lot of information<br />

available in the market – but no informational advantage<br />

to any one investor. The advantage comes with how the<br />

information is used to make decisions. We piece together<br />

bits of information to form a view of a company that other<br />

investors aren’t recognizing. If we have a unique insight about<br />

a company, it might end up as an idea in the portfolio. We<br />

base it on the valuation of the business and our insight – but<br />

it really means having a view of something that the rest of the<br />

market doesn’t. Coming up with our thesis can sometimes<br />

take a relatively short period – a week or two – and sometimes<br />

we study a company for months or years.<br />

JENKINS: We create an insight and follow with an idea, but<br />

that needs to work in order for us to achieve returns higher<br />

than the market. Over time, we judge whether or not the<br />

thesis is working. If it is, we stay with the investment, but if we<br />

judge that something has changed, then we sell and move on.<br />

[Q] You talk about investing in leading companies. How<br />

do you define a leading company?<br />

JENKINS: We focus on companies, but part of analyzing a<br />

business is to look at the industry structure – the nature of the<br />

industry they’re in – whether or not it’s easy to enter or difficult<br />

to exit, the nature of competition, and technological changes.<br />

2 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Introducing Black Creek<br />

That gives us a sense of how a company is positioned. To us,<br />

it means that they’re leading in market share and growing<br />

market share faster than the competition. In our judgment,<br />

it’s essentially a company that’s going to outpace its industry.<br />

In general, those companies typically have significantly<br />

higher long-term profits and sustainable positions. Our view<br />

may not be the common view, but over time, we feel that<br />

they’re going to do much better than other companies.<br />

A good example is Adidas. We invested in it over a decade ago<br />

when it was viewed as not being as strong as Nike. At the time,<br />

Adidas was a well-known brand that had suffered for lack of<br />

investment. However, it had new management with a lot of<br />

brand experience and there were tailwinds for the industry,<br />

such as demographics. Over the years, they have done a<br />

really great job of rebuilding the brand, taking market share<br />

and building it up in different parts of the world. It’s now to<br />

the point where they’re growing just as fast as Nike. It’s a good<br />

example of identifying a leading company before everyone else<br />

figured that out. Hence, the idea was unique and proprietary.<br />

KANKO: The flip side is also true. If it’s a widely held view<br />

that a company is a leading in its field and the prospects look<br />

great, and we don’t have any view that’s different than the<br />

market view, then we might choose not to own it. A portfolio<br />

is not just what you own – it’s also what you don’t.<br />

[Q] Are there any themes that run through your portfolios?<br />

KANKO: We are not “thematic” investors, but we are<br />

certainly aware of the big picture and the trends and issues<br />

that might impact our investments. For example, we stay on<br />

top of technology and how it could affect various companies<br />

– either positively or negatively. As investors, we are very<br />

conscious of the threat to manufacturers from low-priced<br />

Chinese and Korean suppliers. Another area we follow are<br />

companies that are dependent on government financing or<br />

subsidies because these might have more difficulty in the<br />

future because of the fiscal position of governments. There<br />

are a host of other factors that we consider which could<br />

present investment opportunities or risks.<br />

[Q] The Black Creek portfolios are concentrated –<br />

generally only 20–25 companies. How do you achieve<br />

diversification with such a concentrated portfolio?<br />

JENKINS: From financial theory perspective, 20 to<br />

25 companies is statistically more than enough to achieve<br />

diversification – so long as the businesses are in different<br />

geographies and industries and exposed to different<br />

economic effects. We make sure our portfolio is diversified,<br />

but in the end there has to be someone making decisions<br />

about a portfolio. In order to understand the businesses at<br />

great length, you need to study them, follow them, build<br />

a thesis, and then track them. It’s impossible to do that as a<br />

decision maker if you have100 or 200 companies. No one can<br />

know that many companies in depth. The Black Creek team<br />

is four people. Inside our firm there are about 35 holdings.<br />

Divided by four people, that’s roughly 8 to 9 each. On average,<br />

each person is looking at 10 to 12 companies, and with our<br />

turnover rate of between 20% and 30%, each person is buying<br />

two or three stocks a year. In addition, the discipline of having<br />

20 to 25 companies forces us to make choices between<br />

something that’s good and something that’s even better – which<br />

is hard to do as an investor. It might mean selling something<br />

that’s still undervalued to buy something more undervalued.<br />

In the long run, it ensures that we’re always upgrading the<br />

portfolio. We are always selling our least preferred idea to buy<br />

our most preferred one.<br />

[Q] What are the benefits of a focused portfolio?<br />

KANKO: The biggest benefit of having a focused portfolio is<br />

that it keeps you from getting overly diversified and becoming<br />

like the market. We think that if our investment approach is<br />

correct and we execute properly, we should focus our efforts<br />

on a select group of companies. The shorter list also helps<br />

us stay on top of the companies better and know them a<br />

little better than our competitors. Lastly, it promotes a sell<br />

discipline. If we find a new idea that we like, we have to make<br />

room in the portfolio for it by selling our least favourite idea.<br />

[Q] How do you make that decision to buy or sell one<br />

company instead of another?<br />

KANKO: The selling goes along with the buy process. It’s<br />

having a unique view that is different from everyone else –<br />

and a picture of the company looking out five or 10 years. We<br />

then determine what we think the company is worth based on<br />

that view. If we think it’s worth substantially more than what<br />

the market says, it becomes an idea. That’s how we build the<br />

portfolio. We find 20 or 25 of those ideas, and then the sell<br />

process just follows. If we find something else that we think<br />

is a good idea, we have to make room for it by selling our<br />

least favourite idea. Anything we look at has to compare with<br />

everything we already own. Ideally, we sell to make room for<br />

a new holding, and that maintains the discipline of a focused,<br />

concentrated portfolio. We also sell if there’s a significant<br />

negative change in the business that we think is ongoing, or if<br />

the price gets too high.<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 3

Introducing Black Creek<br />

JENKINS: Sometimes an event happens – let’s say a competitor<br />

gets taken over and everything goes up – so we decide, “Okay,<br />

everything positive we can think about that could happen to<br />

this company has happened, so it’s time to move on.”<br />

[Q] Let’s talk about some of your current and previous<br />

holdings and why you bought and sold them.<br />

JENKINS: I’m going to talk about Publicis – a French<br />

company that leads in different advertising markets around<br />

the world. It’s number one in advertising, media planning<br />

and buying, and an industry leader in digital media, such<br />

as Web ads. We bought it in 2008 when cyclically many<br />

of their customers were cutting back on advertising. Since<br />

automobiles are a very large portion of media advertising,<br />

the concern was with General Motors and Chrysler going<br />

bankrupt. At Publicis, auto advertising accounted for<br />

significant revenues and market sentiment was that the<br />

company would have bad accounts receivable from the auto<br />

firms. As we did our work, we discovered that the accounts<br />

receivable to Publicis from these two firms was less than the<br />

upfront deposits they had already made to buy media for the<br />

following year. As we thought about it, we assumed that even<br />

if they went bankrupt, it would be interesting for them to<br />

try to get their money back from Publicis. We came to the<br />

conclusion that the market had overdone it.<br />

The second part of our thesis was that as we came out of this<br />

downturn, the battle for market share was actually going to<br />

be at a higher level than it was before the recession. That’s<br />

because company balance sheets would be very clean. In<br />

addition, we were seeing the emergence of competitors from<br />

emerging markets. Companies like Jaguar and Volvo were<br />

being rejuvenated by India’s Tata Motors and China’s Geely<br />

Automobile Holdings. Our view was that competition in<br />

advertising would snap back faster and be more intense than<br />

it was before the downturn. Recently, we had Publicis’ largest<br />

competitor in our office and they were surprised at how fast<br />

the market snapped back. Our thesis is now playing out.<br />

KANKO: It goes back to our unique insights and how we<br />

generate ideas. Years ago, I owned Canon and for me, it was<br />

always an Internet idea because the Internet was changing<br />

the print model. Instead of printing glossy brochures centrally<br />

and distributing them, companies could easily distribute the<br />

information electronically and then print at any location.<br />

Canon owned the desktop. They had an 80% market<br />

share of laser print engines, plus bubble jet printers,<br />

and camera printers. Since the Internet was driving the local<br />

print business, it benefited Canon and its ability to sell ink.<br />

Then, three or four years ago, we started using Adobe Acrobat<br />

in our office. Almost everything we do is in electronic form.<br />

We started thinking about the prospects for a paperless world<br />

as technology became cheaper. In 2009, Adobe went from<br />

US$50 down to less than US$17. That was the genesis of the<br />

idea. We sold Canon and bought Adobe. Adobe is a follow up<br />

on the Canon idea.<br />

[Q] How do you manage risk?<br />

KANKO: We define risk as permanent impairment of capital<br />

– not volatility of share price. We focus on businesses and<br />

how they act in different environments. Typically, we buy<br />

companies dramatically below what we think it’s worth. We<br />

have 25 holdings and make sure they are not all in the same<br />

geography and industry. Then we go through an exercise,<br />

such as, “What happens if commodity prices are higher than<br />

what we expect? Can our companies increase prices? If they<br />

can’t, who gets hurt? Who gets hurt by low interest rates?<br />

Who gets hurt by different economic factors?”<br />

[Q] As investors, Black Creek measures itself over a<br />

10-year horizon. Why?<br />

JENKINS: The reason we use 10 years is because we want<br />

to understand how that business does throughout an entire<br />

business cycle. If it has two or three years where it does great<br />

and eight that do poorly – it’s a bad investment. As investors,<br />

we want to be in businesses that over a 10-year period are<br />

growing value for their shareholders. For example, if I’m<br />

buying a business that is cyclical, and we’re at year six of an<br />

expansion, and I’m using a 10-year view, then I’m putting a<br />

recession in the next two or three years, which is presumably<br />

going to be reflected in the price. If I’m in the middle of a<br />

recession, and I’m doing a 10-year analysis, it’s likely that the<br />

next recession isn’t for another eight to 10 years – again, it<br />

should be reflected in the price. The point is to make sure<br />

you differentiate between cyclical growth and real growth.<br />

This is the problem right now because we’re coming out of a<br />

big downturn, where lots of things look like they’re growing<br />

quickly. But we are about to shift down. Over the next year or<br />

so, we’re going to find out who is really growing.<br />

KANKO: If you’re focused on the long term, you see things<br />

differently when you speak to companies – you ask different<br />

questions. When we go to meetings with other investment<br />

managers, we’re asking very different questions than everyone else.<br />

4 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Introducing Black Creek<br />

[Q] Why have you chosen not to hedge against the effects<br />

of currency?<br />

KANKO: Hedging is supposed to reduce the volatility of your<br />

expected results – but it comes at a cost. It’s an ongoing cost<br />

that we’ve chosen not to incur because it eats up capital and<br />

we don’t think it serves any long-term purpose. Plus, many<br />

companies that we hold are already hedged, either through<br />

where they generate their sales and earnings, or they have<br />

hedges in place.<br />

JENKINS: The other thing is that for Canadian investors,<br />

the dollar is pro-cyclical. If the global economy strengthens,<br />

the Canadian dollar gets strong – particularly if energy<br />

prices strengthen. There’s a natural offset by owning a global<br />

portfolio to slowdowns or weakening of the economy. We<br />

saw that in 2008, when the equity market was down 50% or<br />

more, the Canadian dollar fell from US$1.02 to US$0.74. A<br />

global portfolio did substantially better in a weakened market<br />

than a Canadian portfolio. Our view of currency is based on<br />

purchasing power parity because over the long term that is<br />

the most reliable indicator. Relative to the U.S. dollar, we feel<br />

the Canadian dollar is overvalued by 25%. It’s also overvalued<br />

relative to the pound and euro. We have views on currencies,<br />

but they’re just one of the factors that go into the decisionmaking<br />

process.<br />

[Q] Canadian investors still have a large percentage of<br />

their holdings in domestic companies. What would you<br />

say to Canadian investors about going global?<br />

JENKINS: In just about every country studied, people carried<br />

a home market bias. Some of that is related to currency, some<br />

of it is a form of nationalism – I don’t know how else to put it.<br />

People tend to think that domestic companies are better than<br />

foreign ones. We try to find the very best company we can<br />

whether it’s in Canada, Japan or the U.S. – each environment<br />

has its own positives and negatives. A Canadian company has<br />

a lot of positives and some negatives – so does a Japanese<br />

one. We try to look at each case independently and find the<br />

25 best ideas.<br />

KANKO: Plus, the Canadian market is pretty narrow – it’s<br />

largely resources and financials. If you look at our portfolios,<br />

there are a lot of sectors you cannot access in Canada. There<br />

is a world of opportunities out there that simply does not exist<br />

in Canada.<br />

JENKINS: Another way to say it is, “Okay, if I’m in Canada<br />

and have a portfolio of stocks, why would I go elsewhere?”<br />

Well, I’d go elsewhere to get a better company or to invest<br />

in industries that are not available in Canada. For example,<br />

if I’m going to look at an oil company, why would I buy an<br />

oil company somewhere else? It has to be better than a<br />

Canadian one. Adidas owns Reebok CCM and everyone<br />

knows CCM hockey equipment – they just don’t know it’s<br />

owned by the Germans.<br />

Black Creek Investment Management<br />

Toronto-based Black Creek Investment Management was<br />

founded by Bill Kanko in February 2005. He was later joined<br />

by Richard Jenkins in <strong>July</strong> 2008. They believe that their ability<br />

to develop proprietary investment ideas will grow wealth for<br />

their clients over the long term. Their goal is to provide capital<br />

growth over the long term through investments in common<br />

equities, and to achieve superior returns relative to equity<br />

market averages in general and to competitors.<br />

Black Creek Investment Management strives to offer a worldclass<br />

global equity capability for its clients. Building on the<br />

background, experience and track records of the founding<br />

partners, the managers aim to provide long-term results that<br />

are among the best of their competitor peer group.<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 5

Introducing Black Creek<br />

The Black Creek Team<br />

Bill Kanko<br />

President & Portfolio Manager<br />

• 30 years’ investment management experience<br />

• From 1999 to 2004, Bill managed global equity portfolios<br />

for AIM Trimark as lead manager of Trimark Fund and<br />

Trimark Select Growth Fund<br />

• Managed more than $13 billion in assets<br />

• Trimark Fund performance was top-decile,1999-2004<br />

• Canadian Investment Award winner, 2002, best global<br />

equity fund<br />

• Castlerock Global Leaders – Silver award winner,<br />

Canadian Investment Awards, 2009; Lipper Fund Award,<br />

Global Equity category, 2011 (3 years)<br />

Richard Jenkins<br />

Managing Director<br />

& Portfolio Manager<br />

• Over 20 years’ investment management experience<br />

• Prior to joining Black Creek, Richard spent over 14 years<br />

with AIM Trimark as the lead manager of the top-performing<br />

Trimark Europlus Fund and the Trimark Global Balanced Fund<br />

• Managed $10 billion in assets<br />

• Five-time Canadian Investment Award winner, 2004-2006,<br />

in the global balanced and European equity categories<br />

• Two Lipper Fund Awards: Castlerock Global Balanced Fund,<br />

2011 (3 years) and Castlerock International Fund, 2010 (1 year)<br />

Matias Galarce<br />

Director of Global Equities<br />

• Joined Black Creek in 2006<br />

• Over nine years of investment experience and<br />

five years in the operational and consulting fields<br />

• Prior to Black Creek, he was part of the investment<br />

management team at Wirth Associates<br />

Evelyn Huang<br />

Director of Global Equities<br />

• Joined Black Creek in 2010<br />

• Prior to Black Creek, spent five years with Invesco<br />

Trimark as an investment analyst and portfolio manager<br />

for global equities<br />

• Co-managed Trimark Select Growth Fund and Trimark<br />

International Companies Fund<br />

6 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Book reviews<br />

Book reviews<br />

Settling in for a<br />

long read<br />

<strong>Summer</strong> is a time to kick back,<br />

fi nd a shady spot on the beach and<br />

settle in for a long read. As the season<br />

was starting, we asked our portfolio<br />

managers what they planned to read<br />

this summer – what they had read<br />

recently that they particularly liked.<br />

We hope you fi nd their selections on<br />

the following pages both insightful<br />

and entertaining.

Book reviews<br />

Book reviews<br />

Richard Jenkins<br />

Managing Director<br />

& Portfolio Manager<br />

Black Creek Investment Management<br />

What I plan to read this summer<br />

The Logic of Scientific Discovery by Karl Popper<br />

Routledge, 544 pages<br />

In essence, it applies the same logic we do to “uncovering<br />

ideas” in the realm of scientific discovery.<br />

last century.<br />

First published in English in 1959 (1935<br />

in Germany), Karl Popper’s The Logic<br />

of Scientific Discovery revolutionized<br />

contemporary thinking about science<br />

and knowledge and is one of the most<br />

widely read books about science written<br />

Popper presents the two ideas that did more than anything<br />

else to make him famous: that the only true knowledge<br />

is scientific knowledge and that knowledge grows only<br />

when on testing a theory, it can be shown to be false.<br />

Popper’s now legendary doctrine of ‘falsificationism’<br />

electrified the scientific community, influencing even the<br />

methods of working scientists. It also had a profound<br />

effect on the shape of postwar philosophy. Translated into<br />

many languages, it ranks alongside The Open Society and<br />

Its Enemies as one of Popper’s most enduring and famous.<br />

The best book I’ve read in the past year<br />

FICTION: Fall of Giants by Ken Follett,<br />

Dutton, 985 pages<br />

I really enjoyed Fall of Giants by Ken Follett, a historical<br />

novel set in the World War I era. The book follows the fates<br />

of five interrelated families – American, German, Russian,<br />

English and Welsh.<br />

This is a huge novel that follows five<br />

families through the world-shaking<br />

dramas of the First World War, the<br />

Russian Revolution, and the struggle<br />

for votes for women. It is 1911. The<br />

Coronation Day of King George V. The<br />

Williams, a Welsh coal-mining family,<br />

are linked by romance and enmity to the Fitzherberts,<br />

aristocratic coal-mine owners. Lady Maud Fitzherbert<br />

falls in love with Walter von Ulrich, a spy at the German<br />

Embassy in London. Their destiny is entangled with that<br />

of an ambitious young aide to U.S. President Woodrow<br />

Wilson and to two orphaned Russian brothers, whose<br />

plans to emigrate to America fall foul of war, conscription<br />

and revolution. In a plot of unfolding drama and intriguing<br />

complexity, Fall of Giants moves seamlessly from<br />

Washington to St Petersburg, from the dirt and danger of a<br />

coal mine to the glittering chandeliers of a palace, from the<br />

corridors of power to the bedrooms of the mighty.<br />

– Amazon.com<br />

– Wikipedia<br />

8 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Book reviews<br />

NON-FICTION: The Big Short: Inside the Doomsday Machine<br />

by Michael Lewis<br />

Norton, 266 pages<br />

I enjoyed The Big Short: Inside the Doomsday Machine, but<br />

to be honest, it actually sickened me as to how many Wall<br />

Street firms had betrayed their clients.<br />

The global financial crisis of 2008,<br />

which economists estimate could<br />

result in several trillion dollars of<br />

losses and which has already cost<br />

American taxpayers billions of dollars<br />

in government bailouts, was triggered<br />

not by war or recession but by a crazy,<br />

man-made money machine, built on flawed mathematical<br />

models that most financial executives did not really<br />

understand themselves. Greedy and heedless, Wall Street<br />

firms had been turning subprime mortgages – loans made<br />

to people with low creditworthiness or little documentation<br />

– into exotic, toxic financial products that they made a<br />

fortune laundering and reselling, and they were enabled in<br />

doing so by the very ratings agencies that were supposed<br />

to police risk. The insanity of this growing and highly<br />

leveraged trade in mortgage derivatives continued even<br />

as the quality of the underlying loans grew increasingly<br />

dubious, even as it became increasingly likely that the<br />

American housing bubble was going to pop.<br />

– The New York Times<br />

Matthew Strauss<br />

Global Strategist &<br />

Portfolio Manager<br />

Signature Global Advisors<br />

What I plan to read this summer<br />

Lula of Brazil: The Story So Far by Richard Bourne<br />

University of California Press, 304 pages<br />

Luiz Inacio Lula da Silva (two-time Brazilian president) is<br />

often described as a charismatic, rags-to-riches, working-class<br />

president who commanded global respect. Also, his path to the<br />

Presidency and style differed significantly from his predecessor,<br />

Fernando Cardoso. I’m hoping that this book will provide as<br />

much insight into Brazilian politics and economics as Cardoso’s<br />

memoirs, but with an obvious difference – instead of following<br />

the political and intellectual elite, this should provide a vivid<br />

and compelling view from the workers’ perspective.<br />

Luiz Inácio Lula da Silva’s dramatic life<br />

story has captured the imagination of<br />

millions, and his progressive politics have<br />

brought hope and excitement to Brazil –<br />

and the world. This compelling work is the<br />

first major English-language biography of<br />

the metalworker who became president<br />

of Latin America’s largest and most powerful country. In a<br />

clearly written, vividly detailed narrative, Richard Bourne<br />

describes Lula’s childhood hardships in an impoverished<br />

family, his days as a revered trade unionist, and the strike<br />

movement that brought down Brazil’s military dictatorship.<br />

The book chronicles Lula’s campaigns for the presidency,<br />

his first term in office beginning in 2002, a major corruption<br />

scandal, and his re-election in 2006. Throughout, Lula<br />

of Brazil connects this charismatic leader’s life to larger<br />

issues, such as the difficulty of maintaining a progressive<br />

policy in an era of globalization.<br />

– University of California Press<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 9

Book reviews<br />

The best book I’ve read in the past year<br />

FICTION: The Assassin by Stephen Coonts<br />

St. Martin’s Press, 512 pages<br />

When it comes to reading for relaxation, I end up in the<br />

thriller section with Robert Ludlum and Wilbur Smith<br />

high on my list. I will now add Steven Coonts. I thoroughly<br />

enjoyed the combination of suspense, politics and quasirealism<br />

in The Assassin.<br />

From Stephen Coonts comes a novel of<br />

high octane excitement – The Assassin<br />

– featuring Tommy Carmellini in his most<br />

dangerous mission yet.<br />

In the finale of Coonts’s last novel The<br />

Traitor, the ruthless and brilliant Al Qaeda<br />

leader who nearly succeeded in blowing up a meeting of the<br />

Group of 7 in Paris slipped the noose and escaped. But Abu<br />

Qasim has another trick up his sleeve: he has offered to pay<br />

the Mafia a fortune to help him bring New York to its knees.<br />

The <strong>CI</strong>A learns that something is up and a worried president<br />

sends his best – Jake Grafton and his secret weapon, Tommy<br />

Carmellini. Tommy is soon in grave danger as he tries to piece<br />

the deadly puzzle together. Set amidst ticking bombs and flying<br />

bullets, the stakes have never been higher. Will Tommy put it<br />

all together in time t stop the disaster? Or will the terrorists set<br />

events in motion that will leave America reeling?<br />

– Barnes & Noble<br />

NON-FICTION: The Accidental President of Brazil by<br />

Fernando Henrique Cardoso<br />

Public Affairs, 320 pages<br />

I found The Accidental President a fascinating and easy<br />

read, taking you on an absorbing journey through Brazil’s<br />

recent history. At times, the book read more like a novel<br />

than a memoir, but given Brazil’s extraordinary political<br />

and economic history, this should not come as a surprise.<br />

The country moved from a military regime to a democracy<br />

(1980s), and from hyper-inflation (1990s) and seven<br />

currencies in eight years to a stable and flourishing economy<br />

in the last 10 years.<br />

Fernando Henrique Cardoso received<br />

a phone call in the middle of the night<br />

asking him to be the new Finance<br />

Minister of Brazil. As he put the phone<br />

down and stared into the darkness of his<br />

hotel room, he feared he’d been handed<br />

a political death sentence. The year was<br />

1993, and he would be responsible for an economy that had<br />

had seven different currencies in the previous eight years to<br />

cope with inflation that had run at 3000% a year. Brazil had<br />

a habit of chewing up finance ministers with the ferocity of<br />

an Amazon piranha.<br />

This was just one of the turns in a largely unscripted and<br />

sometimes unwanted political career. In exile during the<br />

harshest period of the junta that ruled Brazil for twenty years,<br />

Cardoso started his political life with a tentative run for the<br />

Federal Senate in 1978. Within fifteen years, and despite<br />

himself, this former sociologist was running the country.<br />

– Public Affairs<br />

10 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Book reviews<br />

Brandon Snow<br />

Principal & Portfolio Manager<br />

Cambridge Advisors<br />

What I plan to read this summer<br />

The Little Book of Behavioral Investing: How not to be your<br />

own worst enemy (Little Book, Big Profits) by James Montie<br />

Wiley, 236 pages<br />

In order to better understand how other investors react in the<br />

market, I’m reading The Little Book of Behavioral Investing,<br />

which explores behavioural investing and the pitfalls many<br />

investors make.<br />

Bias, emotion, and overconfidence are<br />

just three of the many behavioral traits<br />

that can lead investors to lose money<br />

or achieve lower returns. Behavioral<br />

finance, which recognizes that there is<br />

a psychological element to all investor<br />

decision-making, can help you overcome this obstacle.<br />

In The Little Book of Behavioral Investing, expert James<br />

Montier takes you through some of the most important<br />

behavioral challenges faced by investors. Montier reveals<br />

the most common psychological barriers, clearly showing<br />

how emotion, overconfidence, and a multitude of other<br />

behavioral traits, can affect investment decision-making.<br />

Written in a straightforward and accessible style, The<br />

Little Book of Behavioral Investing will enable you to<br />

identify and eliminate behavioral traits that can hinder<br />

your investment endeavors and show you how to go about<br />

achieving superior returns in the process.<br />

– Wiley<br />

The best book I’ve read in the past year<br />

Lords of Finance: The Bankers Who Broke the World, by<br />

Liaquat Ahamed<br />

Penguin, 576 pages<br />

Lords of Finance helped me understand how new and<br />

dysfunctional central banks failed to prevent the Great<br />

Depression. While there will be unintended consequences<br />

from all the recent central bank actions, the world is unlikely<br />

to face the same outcome as it did in the 1930s.<br />

In The Lords of Finance, Ahamed, a<br />

professional money manager, sums up<br />

the causes of the Great Depression as a<br />

series of economic policy blunders that<br />

could have been avoided. He cites as<br />

causal factors the inflationary financing<br />

of World War I by printing money, the<br />

insurmountable war debts of Germany and the Allies,<br />

Germany’s plunge into hyperinflation, and the return of most<br />

currencies to the gold standard at excessive and deflationary<br />

prewar rates. For example, he explains that when the U.S.<br />

stock market bubble burst in 1929 and economic activity<br />

collapsed, the central banks were restrained in stimulating<br />

the economy for fear of losing their gold reserves.<br />

In an epilog, Ahamed draws parallels between the crises of<br />

the Great Depression and those in recent times. He keeps<br />

his history interesting by highlighting the personalities<br />

of the heads of the major central banks, and he employs<br />

the economist John Maynard Keynes as a one-man Greek<br />

chorus critiquing the bankers’ actions. This erudite and<br />

exceedingly well-written tale of financial chaos in the<br />

1920s and 1930s is both timely and instructive for today’s<br />

economic climate.<br />

– Library Journal, vol. 138<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 11

Book reviews<br />

The best book I’ve read in the past year<br />

Losing Mum and Pup by Christopher Buckley<br />

Twelve, 251 pages<br />

Gerry Coleman<br />

Chief Investment Officer<br />

Harbour Advisors<br />

What I plan to read this summer<br />

Unbroken: A World War II Story of Survival, Resilience, and<br />

Redemption by Laura Hillenbrand<br />

Random House, 473 pages<br />

Unbroken is the story of Louis Zamperini. Born in 1917, Louis<br />

was an Olympic distance runner, World War II prisoner of<br />

war and inspirational speaker. The book is billed as a World<br />

War II story of Survival, Resilience, and Redemption. Laura<br />

Hillenbrand is the best selling author of Seabiscuit: An<br />

American Legend.<br />

Laura Hillenbrand reached Louis<br />

Zamperini just in the nick of time – he<br />

was in his mid-80s when she found<br />

him, and 93 now – and it’s an excellent<br />

thing, for his is surely one of the most<br />

extraordinary war stories of all.<br />

In late May 1943, the B-24 carrying the 26-year-old<br />

Zamperini went down over the Pacific. For nearly seven<br />

weeks – longer, Hillenbrand believes, than any other<br />

such instance in recorded history – Zamperini and his<br />

pilot managed to survive on a fragile raft. They traveled<br />

2,000 miles, only to land in a series of Japanese prison<br />

camps, where, for the next two years, Zamperini<br />

underwent a whole new set of tortures. His is one of the<br />

most spectacular odysseys of this or any other war, and<br />

“odyssey” is the right word, for with its tempests and<br />

furies and monsters, many of them human, Zamperini’s<br />

saga is something out of Greek mythology.<br />

– New York Times<br />

A book that I really enjoyed this past year was Losing Mum<br />

and Pup by Christopher Buckley, son of William F. and<br />

Patricia Buckley. Bill Buckley was, of course, the father of the<br />

modern conservative movement. Bill had a terrific intellect<br />

and razor sharp wit, which was on display in the many books<br />

he wrote, as well as TV appearances. The tragicomic true<br />

story traces the year in which both of Chris’s parents died.<br />

The book is a highly entertaining read. Christopher Buckley<br />

is an award-winning author in his own right.<br />

The younger Buckley’s new memoir,<br />

Losing Mum and Pup – about seeing<br />

both his parents die within less than 11<br />

months of each other in 2007 and 2008<br />

– is sure to cause a few moments of<br />

further discomfort in the temple of American conservatism,<br />

where except for Ronald and Nancy Reagan, Bill and Pat<br />

Buckley will always be the First Couple.<br />

The author explains that he’d “pretty much resolved not to<br />

write a book" about his famous parents until he realized<br />

that “when the universe hands you material like this, not<br />

writing about it seems either a waste or a conscious act of<br />

evasion.” Buckley makes clear that the primary “material”<br />

he’s speaking of is the grim business of losing two parents<br />

in such a short span, but he is also well aware that the<br />

elder Buckleys were material, pure and simple.<br />

Well, anything but simple. Each was, it might be said,<br />

a piece of work, in both the Shakespearean sense of<br />

something wondrous to behold and the more current one<br />

of being, shall we say, a handful. The memoir provoked by<br />

their lives and deaths is loving, exasperated and very funny.<br />

In its moments of real ambivalence, Losing Mum and Pup is<br />

surprisingly strong drink.<br />

– New York Times<br />

12 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Book reviews<br />

Malcolm White<br />

Vice-President Portfolio Management<br />

and Portfolio Manager<br />

Signature Global Advisors<br />

What I plan to read this summer<br />

And the Money Kept Rolling In (and Out): Wall Street, the<br />

IMF, and the bankrupting of Argentina by Paul Blustein<br />

Public Affairs, 320 pages<br />

I bought this book in 2003 and recently dusted it off again.<br />

Given the Greek situation, this book is especially relevant and<br />

shows why – in my opinion – Greece will default, devalue its<br />

currency and go back to the drachma.<br />

In the 1990s, few countries were more<br />

lionized than Argentina for its efforts<br />

to join the club of wealthy nations.<br />

Argentina’s policies drew enthusiastic<br />

applause from the IMF, the World Bank<br />

and Wall Street. But the club has a<br />

disturbing propensity to turn its back on<br />

arrivistes and cast them out. That was what happened in<br />

2001, when Argentina suffered one of the most spectacular<br />

crashes in modern history. With it came appalling social<br />

and political chaos, a collapse of the peso, and a wrenching<br />

downturn that threw millions into poverty and left nearly<br />

one-quarter of the workforce unemployed.<br />

– Public Affairs<br />

The best book I’ve read in the past year<br />

The Age of Entanglement: When Quantum Physics<br />

Was Reborn by Louisa Gilder<br />

Alfred A. Knopf, 443 pages<br />

Entanglement is the strange property of physics where two<br />

particles can be synced and communicate over vast distances.<br />

Einstein never really believed in the principle – which would<br />

infer faster than light speeds – but entanglement has been<br />

shown to work and is at the heart of new advances in quantum<br />

computing and communications.<br />

This book offers an easy-to-read account of the history and<br />

physics behind the science.<br />

The first quarter of the 20 th century<br />

produced two theories, relativity and<br />

quantum mechanics, that are still<br />

changing our universe.<br />

With special relativity, Albert Einstein<br />

upended the long-understood meaning<br />

of time, space and simultaneity. With general relativity,<br />

he swapped Newton’s law of gravity based on force for<br />

curved space¬time, and cosmology became a science. Just<br />

after World War I, relativity made front-page news when<br />

astronomers saw the Sun bend starlight. Overnight, Einstein<br />

became famous as no physical scientist before or since, his<br />

theory the subject of poetry, painting and architecture.<br />

Then, with the development of quantum mechanics in the<br />

1920s, physics got really interesting. Quantum physics<br />

was a theory so powerful – and so powerfully weird – that<br />

nearly a century later, we’re still arguing about how to<br />

reconcile it with Einsteinian relativity and debating what it<br />

tells us about causality, locality and realism.<br />

– New York Times<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 13

Portfolio Snapshot<br />

Cambridge Global Equity June 30, 2011<br />

Fund management<br />

Portfolio advisor: Cambridge Advisors<br />

Portfolio manager: (start date)<br />

Alan Radlo (January 2008<br />

Brandon Snow (April 2011)<br />

About Cambridge<br />

• Cambridge Advisors is a Boston and Toronto-based<br />

investment management team which currently manages<br />

over $3 billion in assets.<br />

• It is led by Alan Radlo, Chief investment Officer, who has<br />

over 28 years of investment experience.<br />

• The team has a proven ability to protect investors’ capital<br />

in all markets.<br />

• Cambridge funds provide growth with downside protection.<br />

• The funds have flexible mandates, which are ideal for<br />

pursuing good buying opportunities.<br />

Fund characteristics<br />

Fund inception date:<br />

December 2007<br />

Assets:<br />

$619 million*<br />

*Class A shares at June 30, 2011<br />

Investment objective:<br />

The fund’s objective is to achieve long-term capital growth by<br />

investing primarily in equity securities of companies located<br />

anywhere in the world.<br />

How is the fund managed?<br />

• Although the fund tends to focus on the developed world,<br />

there are no restrictions to its geographic allocation.<br />

• The portfolio is made up of small to large-cap stocks and<br />

encompasses all industry sectors.<br />

• The manager seeks companies which are building economic<br />

value – these typically have strong earnings, solid balance<br />

sheets, excellent management and reasonable values.<br />

Why invest in this fund?<br />

• You want a core foreign equity fund for your portfolio<br />

• you are investing for the medium and/or long term<br />

• you can tolerate medium risk<br />

Holdings analysis<br />

Asset class<br />

International equity 50%<br />

US equity 38%<br />

Cash & equivalents 8%<br />

Canadian equity 4%<br />

Country breakdown<br />

United States 38%<br />

Other 14%<br />

Britain 14%<br />

Germany 12%<br />

France 5%<br />

Canada 4%<br />

Jersey Island 4%<br />

Switzerland 4%<br />

Norway 3%<br />

Denmark 2%<br />

Sector<br />

Industrials 23%<br />

Information technology 19%<br />

Energy 15%<br />

Health care 10%<br />

Cash 8%<br />

Financials 8%<br />

Materials 8%<br />

Consumer discretionary 7%<br />

Utilities 2%<br />

14 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Portfolio Snapshot<br />

Performance<br />

YTD 1 Year 2 Years 3 Years Since inception*<br />

Cambridge Global Equity Corporate Class 0.3% 20% 12% 0% 2.4%<br />

*December 31, 2007<br />

Holdings<br />

Top 15 holdings Country Sector Weight<br />

JPMorgan Chase & Co. United States Financials 2.6%<br />

Standard Chartered PLC Britain Financials 2.5%<br />

Roche Holdings Switzerland Health care 2.0%<br />

Novo-Nordisk Denmark Health care 2.0%<br />

Apache Corp. United States Energy 1.9%<br />

Seadrill Ltd. Bermuda Energy 1.9%<br />

Petrofac Ltd. Jersey Island Energy 1.9%<br />

Devon Energy Corp. United States Energy 1.8%<br />

Abbott Labs Inc. United States Health care 1.6%<br />

Volkswagen AG Germany Consumer discretionary 1.6%<br />

Siemens AG Germany Industrials 1.6%<br />

Brookfield Infrastructure Partners L.P. Canada Utilities 1.6%<br />

Astrazeneca Britain Health care 1.6%<br />

Tourmaline Oil Corp. Canada Energy 1.6%<br />

Schroders PLC Britain Financials 1.5%<br />

Fund codes<br />

Class A<br />

ISC DSC LL<br />

Class F PMA<br />

Cambridge Global Equity Corporate Class 2323 3323 1523 4323 5323<br />

US$ 2518 3518 1218 4518 N/A<br />

T5 118T5 218T5 318T5 418T5 518T5<br />

T8 618T8 718T8 818T8 918T8 018T8<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 15

Portfolio Snapshot<br />

Cambridge Canadian Equity<br />

Corporate Class June 30, 2011<br />

Fund management<br />

Portfolio advisor: Cambridge Advisors<br />

Portfolio managers: (start date)<br />

Alan Radlo (January 2008)<br />

Brandon Snow (April 2011)<br />

About Cambridge<br />

• Cambridge Advisors is a Boston and Toronto-based<br />

investment management team which currently manages<br />

over $3 billion in assets.<br />

• It is led by Alan Radlo, Chief investment Officer, who has<br />

over 28 years of investment experience.<br />

• The team has a proven ability to protect investors’ capital in<br />

all markets.<br />

• Cambridge funds provide growth with downside protection.<br />

• The funds have flexible mandates, which are ideal for<br />

pursuing good buying opportunities.<br />

Fund characteristics<br />

Fund inception date:<br />

December 2007<br />

Assets:<br />

$704 million*<br />

*Class A shares at June 30, 2011<br />

Investment objective:<br />

This fund’s objective is to achieve long-term capital growth<br />

by investing primarily in equity securities of Canadian<br />

companies<br />

How is the fund managed?<br />

• The fund mainly invests in Canadian equities, but has the<br />

ability to invest up to 49% in foreign content.<br />

• The portfolio is made up of small to large-cap companies<br />

encompassing all industry sectors.<br />

• The managers embed risk controls in their stock selection<br />

and continually monitor company earnings and valuations<br />

in order to mitigate risk.<br />

Why invest in this fund?<br />

• You want a core Canadian equity fund for your portfolio<br />

• You are investing for the medium and/or long term<br />

• You are willing to accept medium risk<br />

Holdings analysis<br />

Asset class<br />

Canadian equity 62%<br />

US equity 23%<br />

International equity 10%<br />

Cash & equivalents 5%<br />

Country breakdown<br />

Canada 62%<br />

United States 23%<br />

Other 9%<br />

Britain 3%<br />

Switzerland 1%<br />

Brazil 1%<br />

France 1%<br />

Sector<br />

Energy 20%<br />

Industrials 17%<br />

Information technology 16%<br />

Financials 14%<br />

Consumer staples 9%<br />

Consumer discretionary 8%<br />

Materials 7%<br />

Cash 5%<br />

Utilities 2%<br />

Health care 1%<br />

Other 1%<br />

16 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Portfolio Snapshot<br />

Performance<br />

YTD 1 Year 2 Years 3 Years Since inception*<br />

Cambridge Canadian Equity Corporate Class 4.0% 23.4% 15.0% 1.2% 2.9%<br />

*December 31, 2007<br />

Holdings<br />

Top 15 holdings Country Sector Weight<br />

Shoppers Drug Mart Inc. Canada Consumer staples 3.4%<br />

JPMorgan Chase & Co. United States Financials 2.8%<br />

Canadian Natural Resources Ltd. Canada Energy 2.6%<br />

Tourmaline Oil Corp. Canada Energy 2.5%<br />

Toronto-Dominion Bank Canada Financials 2.3%<br />

Alimentation Couche-Tard Canada Consumer staples 2.2%<br />

Keyera Corp. Canada Energy 2.2%<br />

Cenovus Energy Inc. Canada Energy 2.1%<br />

Onex Corp. Canada Industrials 2.1%<br />

Franco-Nevada Corp. Canada Materials 2.0%<br />

Talisman Energy Inc. Canada Energy 2.0%<br />

Canadian National Railway Canada Industrials 1.9%<br />

Jean Coutu Group Inc. Canada Consumer staples 1.8%<br />

Broadridge Financial Solution United States Information technology 1.6%<br />

Transforce Inc. Canada Industrials 1.6%<br />

Fund codes<br />

Class A<br />

ISC DSC LL<br />

Class F PMA<br />

Cambridge Canadian Equity Corporate Class 2321 3321 1521 4321 5321<br />

US$ 2516 3516 1216 4516 N/A<br />

T5 116T5 216T5 316T5 416T5 516T5<br />

T8 616T8 716T8 816T8 916T8 016T8<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 17

Portfolio Snapshot<br />

Cambridge Canadian Asset Allocation<br />

Corporate Class June 30, 2011<br />

Fund management<br />

Portfolio advisor: Cambridge Advisors<br />

Portfolio managers: (start date)<br />

Alan Radlo (January 2008)<br />

About Cambridge<br />

• Cambridge Advisors is a Boston and Toronto-based investment<br />

management team which currently manages over $3 billion<br />

in assets.<br />

• It is led by Alan Radlo, Chief investment Officer, who has<br />

over 28 years of investment experience.<br />

• The team has a proven ability to protect investors’ capital in<br />

all markets.<br />

• Cambridge funds provide growth with downside protection.<br />

• The funds have flexible mandates, which are ideal for<br />

pursuing good buying opportunities.<br />

Fund characteristics<br />

Fund inception date:<br />

December 2007<br />

Assets:<br />

$485 million*<br />

*Class A shares at June 30, 2011<br />

Investment objective:<br />

This fund’s objective is to achieve a superior total investment<br />

return by investing in a combination of primarily Canadian<br />

equity and fixed-income securities.<br />

How is the fund managed?<br />

• The fixed-income portion is conservatively managed with a<br />

focus on Canadian debt securities.<br />

• The equity portion is mainly Canadian companies, but has<br />

the ability to invest up to 49% in foreign content.<br />

• The managers have a flexible mandate that incorporates<br />

active management across asset classes, geographic and<br />

industry sector allocations.<br />

Why invest in this fund?<br />

• You want combined income and growth<br />

• You want active asset allocation among equity securities, fixed<br />

income securities and cash<br />

• You are investing for the medium term<br />

• You can tolerate low to medium risk<br />

Holdings analysis<br />

Asset class<br />

Canadian equity 60%<br />

Cash & equivalents 20%<br />

US equity 16%<br />

International equity 3%<br />

Canadian bonds 1%<br />

Country breakdown<br />

Canada 61%<br />

Other 21%<br />

United States 16%<br />

Germany 1%<br />

Bermuda 1%<br />

Sector<br />

Energy 26%<br />

Financials 23%<br />

Cash 20%<br />

Industrials 11%<br />

Information technology 10%<br />

Health care 2%<br />

Utilities 2%<br />

Consumer discretionary 2%<br />

Materials 2%<br />

Consumer staples 1%<br />

Bonds 1%<br />

18 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Portfolio Snapshot<br />

Performance<br />

YTD 1 Year 2 Years 3 Years Since inception*<br />

Cambridge Canadian Asset Allocation Corporate Class 5.25% 23.45% 15.65% 4.55% 4.85%<br />

*December 31, 2007<br />

Holdings<br />

Top 15 holdings Country Sector Weight<br />

Keyera Corp. Canada Energy 4.5%<br />

Inter Pipeline Fund Canada Energy 4.1%<br />

Provident Energy Ltd. Canada Energy 3.6%<br />

Tourmaline Oil Corp. Canada Energy 2.6%<br />

Pembina Pipeline Corp. Canada Energy 2.6%<br />

Canadian Natural Resources Ltd. Canada Energy 2.5%<br />

JPMorgan Chase & Co. United States Financials 2.0%<br />

Brookfield Infrastructure Partners L.P. Canada Utilities 2.0%<br />

Canadian National Railway Co. Canada Industrials 2.0%<br />

Cenovus Energy Inc. Canada Energy 1.9%<br />

Royal Bank Of Canada Canada Financials 1.7%<br />

Toronto-Dominion Bank Canada Financials 1.7%<br />

Magna International Inc. Canada Consumer discretionary 1.6%<br />

National Bank Of Canada Canada Financials 1.6%<br />

Onex Corp. Canada Industrials 1.5%<br />

Fund codes<br />

Class A<br />

ISC DSC LL<br />

Class F PMA<br />

Cambridge Canadian Asset Allocation Corporate Class 2322 3322 1522 4322 5322<br />

US$ 2517 3517 1217 4517 N/A<br />

T5 117T5 217T5 317T5 417T5 517T5<br />

T8 617T8 717T8 817T8 917T8 017T8<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 19

Signature Market Roundup<br />

Market Roundup<br />

Global outlook<br />

Global outlook<br />

Eric Bushell<br />

Senior Vice-President,<br />

Portfolio Management<br />

and Chief Investment Officer<br />

The extraordinary low interest rate environment has created<br />

a surge of investments into riskier, higher-yielding, illiquid<br />

assets. This behaviour was further encouraged by the Federal<br />

Reserve’s asset purchase program (QE2), which recently<br />

concluded. The effects have been largely consistent across<br />

different markets. In our view, this enthusiasm is misplaced<br />

when consideration is given to systemic risks we see in Europe<br />

and America. Several years of low growth and consumer<br />

deleveraging lie ahead and as consumer prices advance<br />

against stagnant wages, we expect to see widespread consumer<br />

retrenchment. The political and social consequences of<br />

the crisis are becoming apparent. Financial regulation is<br />

being enacted with some unintended consequences – such<br />

as the reduction in market liquidity, which may magnify<br />

volatility. At Signature, we are defensively positioned for<br />

this environment.<br />

Drummond Brodeur<br />

Vice-President,<br />

Portfolio Management<br />

and Global Stategist<br />

In a financial markets version of the movie Groundhog Day,<br />

global markets are embroiled in concerns regarding European<br />

sovereign debt defaults and the soft patch in the U.S. economy.<br />

We feel that these concerns are overdone. It is unforgivable that<br />

the Europeans have failed to use the past year to better dilute the<br />

contagion risk from Greece – but here we are. A key difference<br />

this year is that the scope of the problem is understood, as are<br />

the potential avenues of contagion. There is also a US$110<br />

billion safety net in place that did not exist last spring. So some<br />

progress has definitely been made. The major risk last year was<br />

a failure to grasp the extent of the problem – today it is a risk<br />

of failure on the part of the European politicians to execute a<br />

successful containment strategy.<br />

As for the U.S. soft patch, there is no doubt that the second<br />

quarter was a lot slower than first anticipated – but much of the<br />

slowdown can be attributed to supply chain disruptions in autos<br />

and technology resulting from the Japanese earthquake and<br />

tsunami. These disruptions were expected, but unquantifiable,<br />

immediately after the earthquake. These will likely be reversed<br />

in the second half of the year. There is little doubt that elevated<br />

oil prices have reached a point where they are a drag on U.S.<br />

consumption. As was the case last summer, markets will remain<br />

fragile as participants await confirmation of the temporary<br />

nature of the slowdown. As in Europe, the risk of incompetence<br />

on the part of American politicians looms large. At the time<br />

of writing, we expected that a compromise would be reached<br />

on the debt ceiling issue; however, it is important to recognize<br />

that this is just the early rounds for the upcoming 2012 U.S.<br />

election and such political brinkmanship and sparring will be<br />

continuous over the coming year and a half.<br />

Having reduced risk in late April, our funds remain conservatively<br />

positioned. We will remain data dependent when looking to<br />

reinvest some of our cash at more attractive levels – in what we<br />

anticipate to remain a volatile market environment.<br />

20 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Signature Market Roundup<br />

Interest rates<br />

Emerging markets<br />

James Dutkiewicz<br />

Vice-President,<br />

Portfolio Management<br />

and Portfolio Manager<br />

Recent movements in government bonds have been<br />

driven in part by direct economic indicators and in part by<br />

budgetary uncertainty. Yields had been range bound. This<br />

reflected the market’s appreciation for the hesitant, but<br />

resilient, economic expansion as it dealt with natural disasters<br />

and political wrangling. As the second quarter closed, bonds<br />

rallied relentlessly through the bottom of the previous yield<br />

range in response to signals that growth was below trend in<br />

both Canada and the U.S.<br />

Adding to the lower yields was the discord in Washington over<br />

the Republican Party’s insistence on significant budgetary<br />

cuts in exchange for increasing the debt ceiling. Throw in<br />

more Greek protests over austerity measures, the seemingly<br />

inevitable writedown on Greece’s sovereign debt and the safehaven<br />

nature of U.S. government bonds was re-established.<br />

This is not a trivial matter. Should the budgetary impasse in<br />

Washington lead to doubts about the U.S.’s willingness to pay<br />

its obligations, then the subsequent rise in real yields would<br />

create economic chaos.<br />

With Chinese inflation rising past 6%, look for more efforts<br />

by authorities to reign in growth of the globe’s most powerful<br />

economic engine. This will help foster the notion of a global<br />

economy lacking any meaningful growth drivers. How much<br />

of this is priced in to the below 3% yield on U.S. 10-year<br />

bonds? A fair bit given that the Federal Reserve’s bondbuying<br />

program has ended. We liken current yields to the<br />

notion of keeping a beach ball under the water. If global<br />

policymakers defer the hard decisions in favour of promoting<br />

growth, interest rates could pop higher and settle back into<br />

their earlier range.<br />

Matthew Strauss<br />

Vice-President, Portfolio Management,<br />

Portfolio Manager<br />

and Global Strategist<br />

Inflation fears and economic growth concerns weighed on<br />

emerging market equities in the second quarter, partially<br />

offsetting the gains of 2.1% recorded in the first quarter.<br />

The only region that recorded a positive return was Asia,<br />

led by strong quarterly gains in Indonesia, Malaysia and the<br />

Philippines. Peru was the clear laggard as domestic politics<br />

dominated, following the surprise victory of the left-leaning<br />

presidential candidate. Renewed uncertainty about the Greek<br />

debt situation and the end of quantitative easing (QE2) in the<br />

U.S. added to a sombre investment environment.<br />

European event risk aside, we view the current environment<br />

as a mid-cycle correction in emerging markets and, after last<br />

year’s unsustainably high growth numbers, welcome some<br />

slowing in economic growth. Furthermore, we believe that<br />

many emerging market central banks have done enough or<br />

nearly enough to contain inflation without risking a sharp<br />

slowdown in their respective economies. Consequently, these<br />

central banks are expected to move to the sidelines during<br />

the next two quarters. As inflation peaks in the third quarter<br />

and fears of a hard landing subside, emerging markets are set<br />

to outperform their developed counterparts once again. We<br />

will continue to focus on those sectors with direct exposure to<br />

the domestic markets, paying specific attention to domestic<br />

consumer stocks, financials and health care. From a regional<br />

perspective, we continue to favour Asia given its still strong<br />

underlying growth dynamics and expectations of a pause in<br />

monetary policy tightening.<br />

SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011 21

Signature Market Roundup<br />

Preferred Shares<br />

Autos<br />

John Shaw<br />

Vice-President,<br />

Portfolio Management,<br />

Portfolio Manager<br />

Retail investors’ demand for preferred shares remains very<br />

strong as new issuance has been light and redemptions<br />

continue to dampen supply. Supply will remain low due to<br />

the strong capital position of Canadian banks. Almost all of<br />

the $20 billion of bank preferred shares outstanding will be<br />

redeemed over the next six years and only a small amount will<br />

be re-issued. This will strengthen demand given that almost<br />

35% to 40% of the preferred share market may disappear. The<br />

outlook for the preferred market remains positive, especially<br />

following the Office of the Superintendent of Financial<br />

Institutions (OSFI) ruling that the bank preferred shares will<br />

have to be redeemed or exchanged into qualifying securities.<br />

Massimo Bonansinga<br />

Vice-President,<br />

Portfolio Management<br />

and Portfolio Manager<br />

Along with the rest of the automotive sector, auto parts<br />

manufacturers and suppliers suffered from the Japan’s<br />

earthquake and tsunami. Some auto parts companies had<br />

significant assets in the affected area and their share prices<br />

were hit accordingly.<br />

Since the March 11 earthquake, the Japanese automotive<br />

industry has staged a remarkable comeback. Production levels<br />

are scheduled to be back to normal by the end of the summer.<br />

But, because of the lack of product, Japanese Original<br />

Equipment Manafacturers have lost market share globally<br />

and their inventory levels are significantly below normal.<br />

Dealerships need inventory to function properly, especially in<br />

the U.S., where customers prefer to buy vehicles off the lot,<br />

rather than wait and have them built to order.<br />

Over the coming months, Japanese manufacturers will push<br />

production rates hard to catch up with lost sales and rebuild<br />

inventories. Suppliers benefit from higher production<br />

rates because they bill OEMs before the vehicle hits the<br />

dealerships, regardless if it is sold to a customer or it is part of<br />

the dealer inventory. Japanese suppliers have accelerated their<br />

establishment of facilities outside Japan to help manufacturers<br />

increase local content and to diversify their locations.<br />

At Signature, we increased our holdings in Japanese suppliers<br />

and added new ones in March – less than a week after the<br />

earthquake. We believe there will be a fast recovery in<br />

production, so we have invested in companies with clear<br />

technology leadership and a strong push to sell outside<br />

their traditional relationship with the Japanese OEMs. Our<br />

investments in Aisin Seiki, JTEKT (both Toyota affiliated) and<br />

Keihin (Honda affiliated) have already generated 20% upside.<br />

We are confident there is still more to come from multiples<br />

expansion and expanding sales and profitability.<br />

22 SUMMER 2011 PERSPECTIVE AS AT JUNE 30, 2011

Signature Market Roundup<br />

Consumer products<br />

Stephane Champagne<br />

Vice-President,<br />

Portfolio Management<br />

and Portfolio Manager<br />

Consumer activity slowed during the second quarter on a<br />

sequential basis. The negative stories were sharply higher<br />

gasoline prices, higher food costs, slower employment and<br />

bad weather. Overall, the S&P 500 Index underperformed<br />

the consumer discretionary sector by 340 basis points and<br />

consumer staples by 485 bps. Finally, staples outperformed<br />

the consumer discretionary sector by 145 bps during the<br />

period. The staples index has been helped by an increase in<br />

the U.S. unemployment rate to 9.2% at the end of the quarter<br />