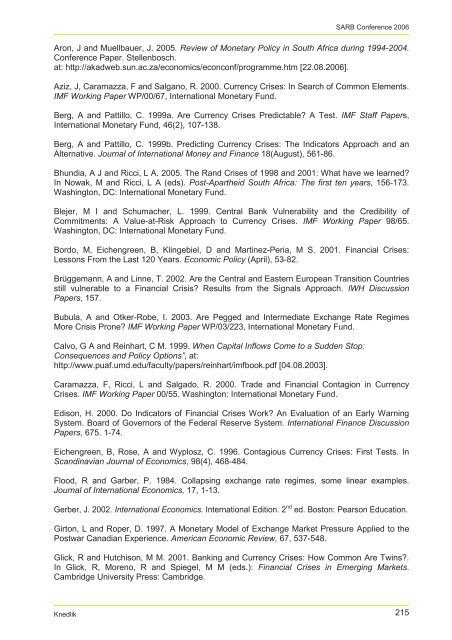

SARB Conference 2006Figure 13: Conditional probabilities with 18-month time w<strong>in</strong>dowConditional probabilities10.80.60.40.201994/011994/071995/011995/071996/011996/071997/011997/071998/011998/071999/011999/072000/012000/072001/012001/072002/012002/072003/012003/072004/012004/072005/012005/072006/01Source: Own calculations. Note: Dotted l<strong>in</strong>e shows unconditional probabilityWhile some difference between the composite <strong>in</strong>dices and the respective conditionalprobabilities can be observed, the general picture rema<strong>in</strong>s the same after chang<strong>in</strong>g the timew<strong>in</strong>dow. While the <strong>in</strong>dex provides <strong>in</strong>dications of the 1996, and <strong>in</strong> particular the 1998, crisis, itfails to clearly <strong>in</strong>dicate 2001 as a crisis. For the time after 2001 there exists no <strong>in</strong>dication ofextraord<strong>in</strong>ary risk of <strong>currency</strong> <strong>crises</strong>. However, as the figure of the unconditional probabilities for<strong>currency</strong> <strong>crises</strong> shows, the overall risk that any month of the period of observation is followed bya crisis with<strong>in</strong> 24 or 18 months is 0,57 or 0,43, respectively. Thus, the risk of <strong>currency</strong> <strong>crises</strong> isthere and the change <strong>in</strong> policy <strong>in</strong> <strong>South</strong> <strong>Africa</strong> resulted <strong>in</strong> less <strong>in</strong>dicated crisis probability due toless risk or to lesser <strong>in</strong>dication of risk.ConclusionThe evaluation of the risk of <strong>currency</strong> <strong>crises</strong> <strong>in</strong> <strong>South</strong> <strong>Africa</strong> by the use of a signals approach,consider<strong>in</strong>g the crisis episodes of 1996, 1998 and 2001 as reference, <strong>in</strong>dicates low current riskfor <strong>currency</strong> <strong>crises</strong>. The approach leads to a correct prediction of the <strong>currency</strong> <strong>crises</strong> of 1996and 1998, but fails to predict the <strong>currency</strong> crisis of 2001. The chang<strong>in</strong>g nature of <strong>currency</strong> <strong>crises</strong>and the change <strong>in</strong> exchange rate policy of the SARB suggest that <strong>crises</strong> of the 2001-type aremore likely to occur <strong>in</strong> future than <strong>crises</strong> of the 1996/1998-type. The crisis <strong>in</strong>dicator, asdeveloped above, must therefore be treated with caution and should be updated frequently. Ashift <strong>in</strong> the period of observation can lead to the detection of new <strong>crises</strong>, previously notconsidered as <strong>crises</strong> and also to a failure of detect<strong>in</strong>g events previously called a crisis. Thechang<strong>in</strong>g volatility of potential signal variables may lead to different signal thresholds and to the<strong>in</strong>clusion or exclusion of variables <strong>in</strong> the composite <strong>in</strong>dex and may therefore change not onlythe <strong>in</strong>dex itself but also the calculated conditional probabilities of <strong>crises</strong>. Further research on<strong>South</strong> <strong>Africa</strong>n <strong>currency</strong> crisis risk should also consider the use of other methods as has beenmentioned <strong>in</strong> the section “Signall<strong>in</strong>g <strong>currency</strong> <strong>crises</strong> – a literature review”.ReferencesAbiad, A. 2003. Early-Warn<strong>in</strong>g Systems: A Survey and a Regime-Switch<strong>in</strong>g Approach. IMFWork<strong>in</strong>g Paper. 03/32. Wash<strong>in</strong>gton: International Monetary Fund.Ahluwalia, P. 2000. Discrim<strong>in</strong>at<strong>in</strong>g Contagion – An Alternative Explanation of ContagiousCurrency Crises <strong>in</strong> Emerg<strong>in</strong>g Markets. IMF Work<strong>in</strong>g Paper WP/00/14, International MonetaryFund.Angk<strong>in</strong>and, A, Li, J and Willett, T. 2006. Measures of Currency Crises: A Survey. Forthcom<strong>in</strong>g<strong>in</strong>: International Interaction.Aron, J and Muellbauer, J. 2000. Estimat<strong>in</strong>g Monetary Policy Rules for <strong>South</strong> <strong>Africa</strong>. Central<strong>Bank</strong> of Chile. Work<strong>in</strong>g Papers 89.214Knedlik

SARB Conference 2006Aron, J and Muellbauer, J. 2005. Review of Monetary Policy <strong>in</strong> <strong>South</strong> <strong>Africa</strong> dur<strong>in</strong>g 1994-2004.Conference Paper. Stellenbosch.at: http://akadweb.sun.ac.za/economics/econconf/programme.htm [22.08.2006].Aziz, J, Caramazza, F and Salgano, R. 2000. Currency Crises: In Search of Common Elements.IMF Work<strong>in</strong>g Paper WP/00/67, International Monetary Fund.Berg, A and Pattillo, C. 1999a. Are Currency Crises Predictable? A Test. IMF Staff Papers,International Monetary Fund, 46(2), 107-138.Berg, A and Pattillo, C. 1999b. Predict<strong>in</strong>g Currency Crises: The Indicators Approach and anAlternative. Journal of International Money and F<strong>in</strong>ance 18(August), 561-86.Bhundia, A J and Ricci, L A. 2005. The Rand Crises of 1998 and 2001: What have we learned?In Nowak, M and Ricci, L A (eds). Post-Apartheid <strong>South</strong> <strong>Africa</strong>: The first ten years, 156-173.Wash<strong>in</strong>gton, DC: International Monetary Fund.Blejer, M I and Schumacher, L. 1999. Central <strong>Bank</strong> Vulnerability and the Credibility ofCommitments: A Value-at-Risk Approach to Currency Crises. IMF Work<strong>in</strong>g Paper 98/65.Wash<strong>in</strong>gton, DC: International Monetary Fund.Bordo, M, Eichengreen, B, Kl<strong>in</strong>gebiel, D and Mart<strong>in</strong>ez-Peria, M S. 2001. F<strong>in</strong>ancial Crises:Lessons From the Last 120 Years. Economic Policy (April), 53-82.Brüggemann, A and L<strong>in</strong>ne, T. 2002. Are the Central and Eastern European Transition Countriesstill vulnerable to a F<strong>in</strong>ancial Crisis? Results from the Signals Approach. IWH DiscussionPapers, 157.Bubula, A and Otker-Robe, I. 2003. Are Pegged and Intermediate Exchange Rate RegimesMore Crisis Prone? IMF Work<strong>in</strong>g Paper WP/03/223, International Monetary Fund.Calvo, G A and Re<strong>in</strong>hart, C M. 1999. When Capital Inflows Come to a Sudden Stop:Consequences and Policy Options”, at:http://www.puaf.umd.edu/faculty/papers/re<strong>in</strong>hart/imfbook.pdf [04.08.2003].Caramazza, F, Ricci, L and Salgado, R. 2000. Trade and F<strong>in</strong>ancial Contagion <strong>in</strong> CurrencyCrises. IMF Work<strong>in</strong>g Paper 00/55. Wash<strong>in</strong>gton: International Monetary Fund.Edison, H. 2000. Do Indicators of F<strong>in</strong>ancial Crises Work? An Evaluation of an Early Warn<strong>in</strong>gSystem. Board of Governors of the Federal <strong>Reserve</strong> System. International F<strong>in</strong>ance DiscussionPapers, 675. 1-74.Eichengreen, B, Rose, A and Wyplosz, C. 1996. Contagious Currency Crises: First Tests. InScand<strong>in</strong>avian Journal of Economics, 98(4), 468-484.Flood, R and Garber, P. 1984. Collaps<strong>in</strong>g exchange rate regimes, some l<strong>in</strong>ear examples.Journal of International Economics, 17, 1-13.Gerber, J. 2002. International Economics. International Edition. 2 nd ed. Boston: Pearson Education.Girton, L and Roper, D. 1997. A Monetary Model of Exchange Market Pressure Applied to thePostwar Canadian Experience. American Economic Review, 67, 537-548.Glick, R and Hutchison, M M. 2001. <strong>Bank</strong><strong>in</strong>g and Currency Crises: How Common Are Tw<strong>in</strong>s?.In Glick, R, Moreno, R and Spiegel, M M (eds.): F<strong>in</strong>ancial Crises <strong>in</strong> Emerg<strong>in</strong>g Markets.Cambridge University Press: Cambridge.Knedlik 215