Manual for the Scrutiny of Central Excise Returns 2008

Manual for the Scrutiny of Central Excise Returns 2008

Manual for the Scrutiny of Central Excise Returns 2008

- No tags were found...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

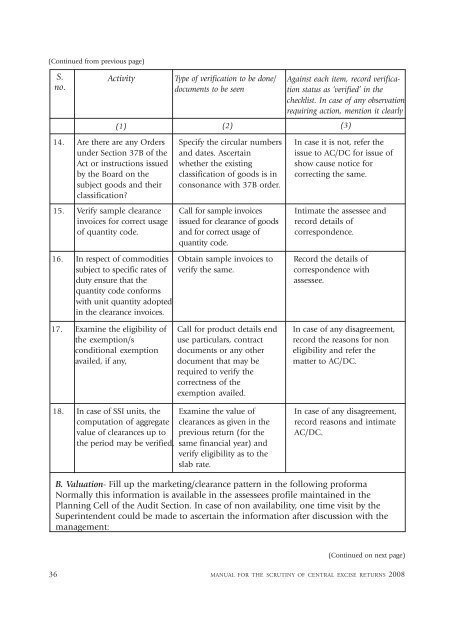

(Continued from previous page)S.no.ActivityType <strong>of</strong> verification to be done/documents to be seenAgainst each item, record verificationstatus as ‘verified’ in <strong>the</strong>checklist. In case <strong>of</strong> any observationrequiring action, mention it clearly(1)(2)(3)14. Are <strong>the</strong>re are any Ordersunder Section 37B <strong>of</strong> <strong>the</strong>Act or instructions issuedby <strong>the</strong> Board on <strong>the</strong>subject goods and <strong>the</strong>irclassification?Specify <strong>the</strong> circular numbersand dates. Ascertainwhe<strong>the</strong>r <strong>the</strong> existingclassification <strong>of</strong> goods is inconsonance with 37B order.In case it is not, refer <strong>the</strong>issue to AC/DC <strong>for</strong> issue <strong>of</strong>show cause notice <strong>for</strong>correcting <strong>the</strong> same.15. Verify sample clearanceinvoices <strong>for</strong> correct usage<strong>of</strong> quantity code.Call <strong>for</strong> sample invoicesissued <strong>for</strong> clearance <strong>of</strong> goodsand <strong>for</strong> correct usage <strong>of</strong>quantity code.Intimate <strong>the</strong> assessee andrecord details <strong>of</strong>correspondence.16. In respect <strong>of</strong> commoditiessubject to specific rates <strong>of</strong>duty ensure that <strong>the</strong>quantity code con<strong>for</strong>mswith unit quantity adoptedin <strong>the</strong> clearance invoices.Obtain sample invoices toverify <strong>the</strong> same.Record <strong>the</strong> details <strong>of</strong>correspondence withassessee.17. Examine <strong>the</strong> eligibility <strong>of</strong><strong>the</strong> exemption/sconditional exemptionavailed, if any,Call <strong>for</strong> product details enduse particulars, contractdocuments or any o<strong>the</strong>rdocument that may berequired to verify <strong>the</strong>correctness <strong>of</strong> <strong>the</strong>exemption availed.In case <strong>of</strong> any disagreement,record <strong>the</strong> reasons <strong>for</strong> noneligibility and refer <strong>the</strong>matter to AC/DC.18. In case <strong>of</strong> SSI units, <strong>the</strong>computation <strong>of</strong> aggregatevalue <strong>of</strong> clearances up to<strong>the</strong> period may be verified.Examine <strong>the</strong> value <strong>of</strong>clearances as given in <strong>the</strong>previous return (<strong>for</strong> <strong>the</strong>same financial year) andverify eligibility as to <strong>the</strong>slab rate.In case <strong>of</strong> any disagreement,record reasons and intimateAC/DC.B. Valuation- Fill up <strong>the</strong> marketing/clearance pattern in <strong>the</strong> following pro<strong>for</strong>maNormally this in<strong>for</strong>mation is available in <strong>the</strong> assessees pr<strong>of</strong>ile maintained in <strong>the</strong>Planning Cell <strong>of</strong> <strong>the</strong> Audit Section. In case <strong>of</strong> non availability, one time visit by <strong>the</strong>Superintendent could be made to ascertain <strong>the</strong> in<strong>for</strong>mation after discussion with <strong>the</strong>management:(Continued on next page)36 MANUAL FOR THE SCRUTINY OF CENTRAL EXCISE RETURNS <strong>2008</strong>