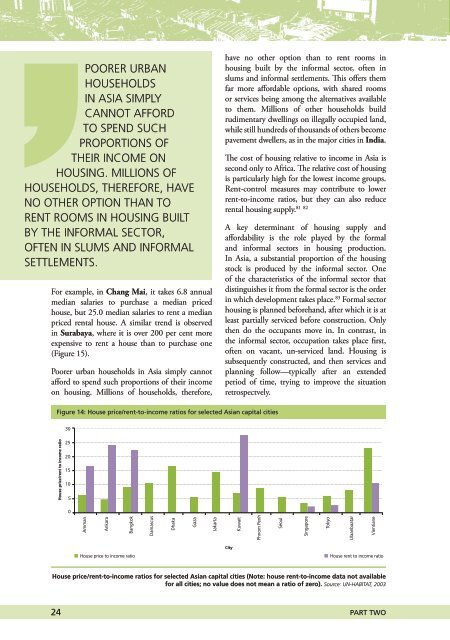

POORER URBANHOUSEHOLDSIN ASIA SIMPLYCANNOT AFFORDTO SPEND SUCHPROPORTIONS OFTHEIR INCOME ONHOUSING. MILLIONS OFHOUSEHOLDS, THEREFORE, HAVENO OTHER OPTION THAN TORENT ROOMS IN HOUSING BUILTBY THE INFORMAL SECTOR,OFTEN IN SLUMS AND INFORMALSETTLEMENTS.For example, <strong>in</strong> Chang Mai, it takes 6.8 annualmedian salaries to purchase a median pricedhouse, but 25.0 median salaries to rent a medianpriced rental house. A similar trend is observed<strong>in</strong> Surabaya, where it is over 200 per cent moreexpensive to rent a house than to purchase one(Figure 15).Poorer urban households <strong>in</strong> Asia simply cannotafford to spend such proportions <strong>of</strong> their <strong>in</strong>comeon <strong>hous<strong>in</strong>g</strong>. Millions <strong>of</strong> households, therefore,have no other option than to rent rooms <strong>in</strong><strong>hous<strong>in</strong>g</strong> built by the <strong>in</strong>formal sector, <strong>of</strong>ten <strong>in</strong>slums <strong>and</strong> <strong>in</strong>formal settlements. This <strong>of</strong>fers themfar more <strong>affordable</strong> options, with shared roomsor services be<strong>in</strong>g among the alternatives availableto them. Millions <strong>of</strong> other households buildrudimentary dwell<strong>in</strong>gs on illegally occupied <strong>l<strong>and</strong></strong>,while still hundreds <strong>of</strong> thous<strong>and</strong>s <strong>of</strong> others becomepavement dwellers, as <strong>in</strong> the major cities <strong>in</strong> India.The cost <strong>of</strong> <strong>hous<strong>in</strong>g</strong> relative to <strong>in</strong>come <strong>in</strong> Asia issecond only to Africa. The relative cost <strong>of</strong> <strong>hous<strong>in</strong>g</strong>is particularly high for the lowest <strong>in</strong>come groups.Rent-control measures may contribute to lowerrent-to-<strong>in</strong>come ratios, but they can also reduce81 82rental <strong>hous<strong>in</strong>g</strong> supply.A key determ<strong>in</strong>ant <strong>of</strong> <strong>hous<strong>in</strong>g</strong> supply <strong>and</strong>affordability is the role played by the forma<strong>l<strong>and</strong></strong> <strong>in</strong>formal sectors <strong>in</strong> <strong>hous<strong>in</strong>g</strong> production.In Asia, a substantial proportion <strong>of</strong> the <strong>hous<strong>in</strong>g</strong>stock is produced by the <strong>in</strong>formal sector. One<strong>of</strong> the characteristics <strong>of</strong> the <strong>in</strong>formal sector thatdist<strong>in</strong>guishes it from the formal sector is the order<strong>in</strong> which development takes place. 83 Formal sector<strong>hous<strong>in</strong>g</strong> is planned beforeh<strong>and</strong>, after which it is atleast partially serviced before construction. Onlythen do the occupants move <strong>in</strong>. In contrast, <strong>in</strong>the <strong>in</strong>formal sector, occupation takes place first,<strong>of</strong>ten on vacant, un-serviced <strong>l<strong>and</strong></strong>. Hous<strong>in</strong>g issubsequently constructed, <strong>and</strong> then services <strong>and</strong>plann<strong>in</strong>g follow—typically after an extendedperiod <strong>of</strong> time, try<strong>in</strong>g to improve the situationretrospectvely.Figure 14: House price/rent-to-<strong>in</strong>come ratios for selected Asian capital cities302520151050AmmanAnkaraBangkokDamascusDhakaHouse price/rent to <strong>in</strong>come ratioGazaJakartaKuwaitPhnom PenhSeoulS<strong>in</strong>gaporeTokyoUlaanbaatarVientianeHouse price to <strong>in</strong>come ratioCityHouse rent to <strong>in</strong>come ratioHouse price/rent-to-<strong>in</strong>come ratios for selected Asian capital cities (Note: house rent-to-<strong>in</strong>come data not availablefor all cities; no value does not mean a ratio <strong>of</strong> zero). Source: UN-HABITAT, 200324PART two

Figure 15: House-price-to-<strong>in</strong>come ratio compared with house rent-to-<strong>in</strong>come ratio <strong>in</strong> selected Asian cities4035House/rent price to <strong>in</strong>come ratio302520151050Chang Mai Chennai Chittagong Hanam Lahore Penang Pokhara Surabaya YangoonHouse price to <strong>in</strong>come ratioHouse rent to <strong>in</strong>come ratioHouse-price-to-<strong>in</strong>come ratio compared with house rent-to-<strong>in</strong>come ratio <strong>in</strong> selected Asian cities.Source: UN-HABITAT, 2003Low <strong>hous<strong>in</strong>g</strong> affordability <strong>in</strong> Asia is pervasive forseveral primary reasons. 84 Firstly, the majority<strong>hous<strong>in</strong>g</strong> f<strong>in</strong>ance mechanisms have high <strong>in</strong>terestrates <strong>and</strong> are <strong>in</strong>flexible, which makes obta<strong>in</strong><strong>in</strong>g<strong>hous<strong>in</strong>g</strong> f<strong>in</strong>ance <strong>and</strong> servic<strong>in</strong>g monthly loanrepayments difficult. Secondly, real estate pricesare high primarily due to high <strong>l<strong>and</strong></strong> costs <strong>and</strong>the high cost <strong>of</strong> build<strong>in</strong>g materials. Thirdly,there are few alternative low-technology <strong>hous<strong>in</strong>g</strong>construction methods available, or used, whichcould reduce <strong>hous<strong>in</strong>g</strong> costs. Fourthly, thecompliance costs <strong>and</strong> regulations surround<strong>in</strong>gformal <strong>hous<strong>in</strong>g</strong> development are expensive <strong>and</strong>time consum<strong>in</strong>g. Lastly, there are significant<strong>in</strong>come disparities between households, <strong>and</strong>the f<strong>in</strong>ancial assets <strong>and</strong> <strong>in</strong>comes <strong>of</strong> low-<strong>in</strong>comehouseholds are not high enough to affordma<strong>in</strong>stream, formal, market-procured <strong>hous<strong>in</strong>g</strong>.Affordability issues are particularly widespread<strong>in</strong> South Asia. Estimates suggest that lowhousehold affordability <strong>in</strong> India affects 30million households. 85 In Sri Lanka 40 per cent<strong>of</strong> households cannot even afford a basic lowcostdwell<strong>in</strong>g. In Pakistan, two thirds <strong>of</strong> thepopulation cannot access formal <strong>hous<strong>in</strong>g</strong> dueto affordability constra<strong>in</strong>ts. Consequently, thesehouseholds seek <strong>hous<strong>in</strong>g</strong> <strong>in</strong> <strong>in</strong>formal, slum areas<strong>and</strong> <strong>in</strong> Karachi alone <strong>in</strong>formal areas house 7.6million people out to a total city population <strong>of</strong>15.1 million. 86Estimates suggest that <strong>in</strong> Afghanistan, 80 percent <strong>of</strong> the population cannot afford to purchaseeven the cheapest new low-cost house. 87 Us<strong>in</strong>gfigures from 2009, the typical monthly earn<strong>in</strong>gsfor low-<strong>in</strong>come households is 30 USD but themortgage repayment on a new low-cost house is49 USD (assum<strong>in</strong>g a loan term <strong>of</strong> 20 years <strong>and</strong><strong>in</strong>terest rate <strong>of</strong> 10 per cent, on a home cost<strong>in</strong>g5,000 USD <strong>of</strong> which 4,000 USD is borrowed).This case <strong>in</strong>dicates that the percentage <strong>of</strong> themonthly mortgage repayment <strong>of</strong> a basic low-costhouse to the median <strong>in</strong>come is 163 per cent,mak<strong>in</strong>g such <strong>hous<strong>in</strong>g</strong> prohibitively expensive<strong>and</strong> near impossible to obta<strong>in</strong> <strong>and</strong> reta<strong>in</strong>. 88Affordability, then, is an issue regard<strong>in</strong>g boththe <strong>in</strong>itial down-payment (<strong>in</strong> this example 1,000USD which would take nearly six years assum<strong>in</strong>ga regular <strong>in</strong>come <strong>of</strong> which 50 per cent is saved)as well as servic<strong>in</strong>g the mortgage repayments(which are 63 per cent more than the <strong>in</strong>come).Of course, this also assumes f<strong>in</strong>ance is available<strong>and</strong> the household has an acceptable credit rat<strong>in</strong>g<strong>and</strong> can therefore obta<strong>in</strong> <strong>hous<strong>in</strong>g</strong> f<strong>in</strong>ance, neither<strong>of</strong> which are always the case.2.4 DOMINANT BUILDING TYPESAffordable <strong>hous<strong>in</strong>g</strong> takes a variety <strong>of</strong> forms <strong>and</strong>many different build<strong>in</strong>g types can be found <strong>in</strong>Asia. They range from traditional rural housetypes that have been adopted for use <strong>in</strong> an urbancontext to modern, multi-storey apartmentcomplexes. Figure 18 shows the range <strong>of</strong> differentdwell<strong>in</strong>g types that can be found <strong>in</strong> selectedcities <strong>in</strong> Asia. Some cities have a large share <strong>of</strong>detached <strong>hous<strong>in</strong>g</strong>, for example Naga, Cebu,AFFORDABLE LAND <strong>and</strong> HOUSING IN Asia25

- Page 3: AFFORDABLE LANDAND HOUSING IN ASIAV

- Page 7 and 8: 3.2.1 HOUSING POLICY AND LEGISLATIV

- Page 13 and 14: LIST OF FIGURESFigure 1: A woman pr

- Page 15 and 16: LIST OF TABLESTable 1: Regional urb

- Page 17 and 18: 1PART oneIntroduction- affordableho

- Page 19 and 20: Figure 3: Regional urbanisation tre

- Page 24 and 25: Figure 7: High-rise multi-household

- Page 26 and 27: can be found throughout Asian citie

- Page 28 and 29: AFFORDABLEHOUSING ISBROADLY DEFINED

- Page 30 and 31: Figure 9: Slum housing in South Asi

- Page 32 and 33: The housingstock in manycountries i

- Page 34 and 35: 2. THE STATE OFAFFORDABLE LANDAND H

- Page 36 and 37: 9.3 square metres in 1998. 62 A stu

- Page 38 and 39: An analysis of sufficient living ar

- Page 42 and 43: THE FORMAL SECTORPlan Service Build

- Page 44 and 45: PART TWO ENDNOTES49 Nenova, T. (201

- Page 46 and 47: Over the lasttwo decadesmicrofinanc

- Page 48 and 49: 3. ADDRESSINGTHE CHALLENGE:AFFORDAB

- Page 50 and 51: HOUSING IS ACATALYST FORSOCIO-ECONO

- Page 52 and 53: lower- to middle-income groups. How

- Page 54 and 55: Grihayan Tahabil (Housing Fund) thr

- Page 56 and 57: provision, especially in countries

- Page 58 and 59: heritage, infrastructure and servic

- Page 60 and 61: market transactions. All units are

- Page 62 and 63: Boatu and Chengdu alone, 600,000 pe

- Page 64 and 65: have built an estimated 700,000 dwe

- Page 66 and 67: 3.2.7 The contribution of NGOsThe m

- Page 68 and 69: quantity and at an affordable cost,

- Page 70 and 71: OVER THE LASTTWO DECADESMICROFINANC

- Page 72 and 73: Table 7: Community savings groups i

- Page 74 and 75: RemittancesRemittances-money transf

- Page 76 and 77: PART THREE ENDNOTES101 UNCHS (1997a

- Page 78 and 79: Access toadequate andaffordablehous

- Page 80 and 81: 4. NOTABLE TRENDS,RECOMMENDATIONSAN

- Page 82 and 83: Overcoming discrimination against w

- Page 84 and 85: Affordable housing for plantation w

- Page 86 and 87: opportunities to solve the underemp

- Page 88 and 89: of other housing delivery systems t

- Page 90 and 91:

PART FOUR ENDNOTES201 UNCHS (1997b)

- Page 92 and 93:

76 PART FIVE

- Page 94 and 95:

AAcioly, C. Jr. (2008). Housing Str

- Page 96 and 97:

JJack, M. (2006). Urbanisation, sus

- Page 98 and 99:

Tipple, A. G. and A. Salim (1999).

- Page 100 and 101:

WWang, Y. P. (2004). Urban poverty,

- Page 102:

AFFORDABLE LANDAND HOUSING INASIAAf