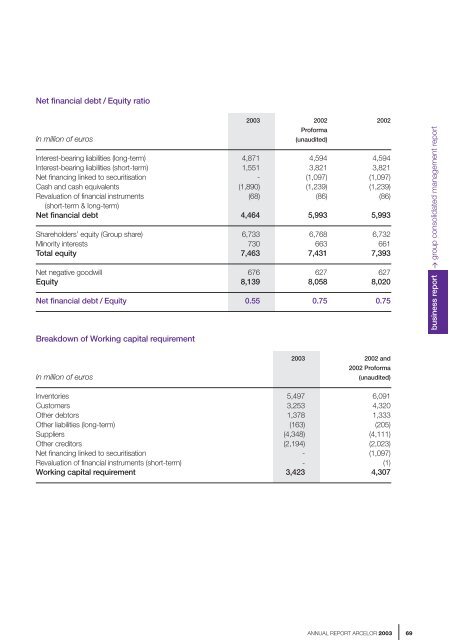

Financial highlights for the GroupIn million of euros<strong>2003</strong> 2002 2002Proforma(unaudited)Revenues 25,923 26,594 24,533Change (1) (2.5%) - -Gross operating result 2,228 1,978 1,811Operating result (OR) 738 780 680Net result (Group share) 257 (121) (186)Net result per share (in euros) 0.54 (0.25) (0.38)(1) Change from 2002 proforma (unaudited)The Group had consolidated revenues of 25,923 millioneuros in <strong>2003</strong> compared with 26,594 million in 2002*, adecline of 2.5% (a 0.6% decline at comparable consolidation).The financial year was characterised by a risein steel prices that was only partly dampened by thevolume reductions made during the year, and by a currencyeffect due to the appreciation of the euro.The consolidated gross operating result posted bythe Group, amounting to 2,228 million euros in <strong>2003</strong>compared with 1,978 million in 2002*, includes (75) millionin non-recurring items (essentially restructuringcosts net of capital gains from the sale of PUM Plastiques).The effect of cost cutting, synergies from themerger, and the recovery of steel prices by and largeoffset the impact of the business slowdown and thedecline in volume – mainly in flat carbon products.The consolidated operating result posted by theGroup, standing at 738 million euros in <strong>2003</strong> comparedwith 780 million in 2002, included (543) million euros innon-recurring charges; the Group reflected in its booksthe strategies announced during the first half of <strong>2003</strong> forthe Flat Carbon Steels sector and particularly for theStainless Steels, Alloys and Specialty Plates sector.After net financial charges of 321 million euros, a positivecontribution from the associated companies of 140 million,a tax charge of 141 million, and taking into account159 million in minority interests, consolidated net result(Group share) was 257 million euros compared with aloss of 121 million for the 2002 financial year*.Changes in Net Financial DebtSubstantially surpassing its goals and undertakings, theGroup reduced its net financial debt by more than 1.5 billioneuros in the <strong>2003</strong> financial year (4,464 million euros as atDecember 31, <strong>2003</strong> compared with 5,993 million as atDecember 31, 2002*). Cash generation accelerated substantiallyover the second part of the year. The programmeto reduce working capital requirements instituted shortlyafter the merger has borne fruit and the special attentiongiven to inventory reduction has paid off. The Group alsopursued a policy to control investment costs whilecollecting the proceeds from the sale of PUM Plastiquesat the end of <strong>2003</strong>. The financial structure of the Groupis, therefore, significantly reinforced and the net financialdebt/equity ratio is now close to the 0.5 target set for2004.* Figures for 2002 proforma (unaudited)68<strong>ANNUAL</strong> <strong>REPORT</strong> <strong>ARCELOR</strong> <strong>2003</strong>

Net financial debt / Equity ratioIn million of euros<strong>2003</strong> 2002 2002Proforma(unaudited)Interest-bearing liabilities (long-term) 4,871 4,594 4,594Interest-bearing liabilities (short-term) 1,551 3,821 3,821Net financing linked to securitisation - (1,097) (1,097)Cash and cash equivalents (1,890) (1,239) (1,239)Revaluation of financial instruments (68) (86) (86)(short-term & long-term)Net financial debt 4,464 5,993 5,993Shareholders’ equity (Group share) 6,733 6,768 6,732Minority interests 730 663 661Total equity 7,463 7,431 7,393Net negative goodwill 676 627 627Equity 8,139 8,058 8,020Net financial debt / Equity 0.55 0.75 0.75business report > group consolidated management reportBreakdown of Working capital requirementIn million of euros<strong>2003</strong> 2002 and2002 Proforma(unaudited)Inventories 5,497 6,091Customers 3,253 4,320Other debtors 1,378 1,333Other liabilities (long-term) (163) (205)Suppliers (4,348) (4,111)Other creditors (2,194) (2,023)Net financing linked to securitisation - (1,097)Revaluation of financial instruments (short-term) - (1)Working capital requirement 3,423 4,307<strong>ANNUAL</strong> <strong>REPORT</strong> <strong>ARCELOR</strong> <strong>2003</strong> 69

- Page 1:

ANNUAL REPORT ARCELOR 2003ANNUAL RE

- Page 4 and 5:

Message from the Chairman ofthe Boa

- Page 6 and 7:

Message from the Chairman ofthe Man

- Page 8 and 9:

Does this mean that the Group is en

- Page 10 and 11:

8ANNUAL REPORT ARCELOR 2003

- Page 12 and 13:

Portrait of the GroupArcelor was bo

- Page 14 and 15:

The Arcelor/Nippon Steel Corporatio

- Page 16 and 17:

Key Figures for 2003Revenues (1) Re

- Page 18 and 19:

2003 highlightsOn January 24, 2003,

- Page 20 and 21: Corporate GovernanceBoard of Direct

- Page 22 and 23: Report of the Chairman of the Board

- Page 24 and 25: Role and authority of the Board of

- Page 26 and 27: 4.2. The Audit Committee andthe App

- Page 28 and 29: AuthorityThe powers of the Manageme

- Page 30 and 31: B. Internal Control Procedures1. GO

- Page 32 and 33: 3.3. Internal control procedures go

- Page 34 and 35: Information regarding capital, mark

- Page 36 and 37: Market informationListingArcelor sh

- Page 38 and 39: Information policyArcelor intends t

- Page 40 and 41: 38ANNUAL REPORT ARCELOR 2003

- Page 42 and 43: table of contents >Flat Carbon Stee

- Page 44 and 45: Within this context, and in order t

- Page 46 and 47: 3.3. Packaging steelsThe packaging

- Page 48 and 49: table of contents >Long Carbon Stee

- Page 50 and 51: 3. THE SECTOR’S PRODUCTS ANDMARKE

- Page 52 and 53: table of contents >Stainless Steels

- Page 54 and 55: The distribution of the UGINE & ALZ

- Page 56 and 57: The adaptation plan - industrial re

- Page 58 and 59: table of contents >Distribution-Pro

- Page 60 and 61: 2. ORGANISATION OF THE SECTORThe ye

- Page 62 and 63: Other ActivitiesThe “Other Activi

- Page 64 and 65: 62ANNUAL REPORT ARCELOR 2003

- Page 66 and 67: Group Consolidated Management Repor

- Page 68 and 69: Trends in global crude steel produc

- Page 72 and 73: Return on capital employed (ROCE) b

- Page 74 and 75: BUSINESS BY SECTORFlat Carbon Steel

- Page 76 and 77: Even though shipments in 2003 in th

- Page 78 and 79: From a financial standpoint, and ex

- Page 80 and 81: The Trading and Distribution busine

- Page 82 and 83: - in September 2003, the sale of th

- Page 84 and 85: The market tightness provoked by th

- Page 86 and 87: Risk ManagementGeneral legal risks

- Page 88 and 89: Group purchasing performanceIn addi

- Page 90 and 91: 88ANNUAL REPORT ARCELOR 2003

- Page 92 and 93: Implementation of the Sustainable D

- Page 94 and 95: Arcelor’s principles Principal ac

- Page 96 and 97: Organisation of Sustainable Develop

- Page 98 and 99: indicators 2002 2003Principle 4 - O

- Page 100 and 101: Group profitabilityObjectives• Av

- Page 102 and 103: Arcelor Health and Safety policyArc

- Page 104 and 105: Safety certificationsSeveral Arcelo

- Page 106 and 107: Arcelor Environmental PolicyArcelor

- Page 108 and 109: Implementation of a monitoring plan

- Page 110 and 111: Dialogue with all stakeholdersObjec

- Page 112 and 113: Dialogue with societyArcelor partic

- Page 114 and 115: Development of individual interview

- Page 116 and 117: Scientific CouncilChairman:• Marc

- Page 118 and 119: Corporate governanceObjectives• E

- Page 120 and 121:

SponsorshipEvery year, the various

- Page 122 and 123:

Durability: Manufacturers are now a

- Page 124 and 125:

122ANNUAL REPORT ARCELOR 2003

- Page 126 and 127:

GENERAL INFORMATION ABOUTARCELORCor

- Page 128 and 129:

Cold-rolled flat products: In 2001,

- Page 130 and 131:

Safeguard clause• United States:

- Page 132 and 133:

130ANNUAL REPORT ARCELOR 2003

- Page 134 and 135:

Consolidated financial statementsof

- Page 136 and 137:

CONSOLIDATED CASH FLOW STATEMENTIn

- Page 138 and 139:

NOTES TO THE CONSOLIDATED FINANCIAL

- Page 140 and 141:

Assets intended to be disposed of o

- Page 142 and 143:

AmortisationAmortisation is recogni

- Page 144 and 145:

13) EquityRepurchase of share capit

- Page 146 and 147:

18) Other provisionsA provision is

- Page 148 and 149:

The major changes in the consolidat

- Page 150 and 151:

NOTE 4 - INTANGIBLE ASSETSGoodwill

- Page 152 and 153:

NOTE 5 - PROPERTY, PLANT AND EQUIPM

- Page 154 and 155:

NOTE 7 - OTHER INVESTMENTSThe main

- Page 156 and 157:

NOTE 13 - EQUITY13.1 Issued capital

- Page 158 and 159:

NOTE 15 - MINORITY INTERESTSIn the

- Page 160 and 161:

16.6 Detail of main individual long

- Page 162 and 163:

17.2.2 Additional pension plansFran

- Page 164 and 165:

17.2.3 Leaving indemnities (continu

- Page 166 and 167:

18.2 Early retirement plansAn actua

- Page 168 and 169:

NOTE 22 - NET FINANCING RESULTIn EU

- Page 170 and 171:

NOTE 24 - RELATED PARTY DISCLOSURES

- Page 172 and 173:

The portfolio of financial instrume

- Page 174 and 175:

NOTE 26 - COMMITMENTS GIVEN AND REC

- Page 176 and 177:

27.1 Breakdown by activity (continu

- Page 178 and 179:

27.2 Geographical breakdown(Figures

- Page 180 and 181:

NOTE 29 - RECONCILIATION OF THE ARC

- Page 182 and 183:

Company name Consolidation Country

- Page 184 and 185:

Company name Consolidation Country

- Page 186 and 187:

Company name Consolidation Country

- Page 188 and 189:

Company name Consolidation Country

- Page 190 and 191:

Company name Consolidation Country

- Page 192 and 193:

Audit31, Allée Scheffer Telephone

- Page 194 and 195:

Annual accounts Arcelor S.A.ANNUAL

- Page 196 and 197:

INCOME STATEMENT FROM JANUARY 1 TO

- Page 198 and 199:

NOTE 3 - STATEMENT OF TANGIBLE FIXE

- Page 200 and 201:

NOTE 8 - PROVISIONS FOR LIABILITIES

- Page 202 and 203:

NOTE 14 - DIRECTORS’ REMUNERATION

- Page 204 and 205:

Arcelor Ordinary General Meeting on

- Page 206 and 207:

GlossaryAnnealing:The heat treatmen

- Page 208 and 209:

How steel is made?a 3-stage process

- Page 210 and 211:

Arcelor’s main steel-manufacturin

- Page 212 and 213:

NOTES210ANNUAL REPORT ARCELOR 2003

- Page 214:

Concept and realization133, avenue