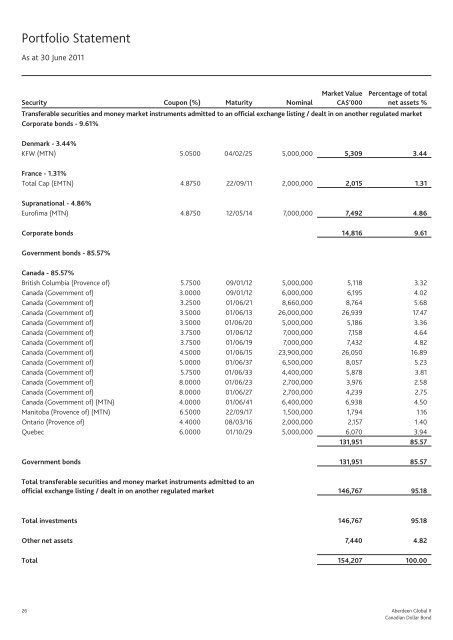

Portfolio StatementAs at 30 June 2011Security Coupon (%) Maturity NominalMarket ValueCA$’000Percentage of totalnet assets %Transferable securities and money market instruments admitted to an official exchange listing / dealt in on another regulated marketCorporate bonds - 9.61%Denmark - 3.44%KFW (MTN) 5.0500 04/02/25 5,000,000 5,309 3.44France - 1.31%Total Cap (EMTN) 4.8750 22/09/11 2,000,000 2,015 1.31Supranational - 4.86%Eurofima (MTN) 4.8750 12/05/14 7,000,000 7,492 4.86Corporate bonds 14,816 9.61Government bonds - 85.57%Canada - 85.57%British Columbia (Provence of) 5.7500 09/01/12 5,000,000 5,118 3.32Canada (Government of) 3.0000 09/01/12 6,000,000 6,195 4.02Canada (Government of) 3.2500 01/06/21 8,660,000 8,764 5.68Canada (Government of) 3.5000 01/06/13 26,000,000 26,939 17.47Canada (Government of) 3.5000 01/06/20 5,000,000 5,186 3.36Canada (Government of) 3.7500 01/06/12 7,000,000 7,158 4.64Canada (Government of) 3.7500 01/06/19 7,000,000 7,432 4.82Canada (Government of) 4.5000 01/06/15 23,900,000 26,050 16.89Canada (Government of) 5.0000 01/06/37 6,500,000 8,057 5.23Canada (Government of) 5.7500 01/06/33 4,400,000 5,878 3.81Canada (Government of) 8.0000 01/06/23 2,700,000 3,976 2.58Canada (Government of) 8.0000 01/06/27 2,700,000 4,239 2.75Canada (Government of) (MTN) 4.0000 01/06/41 6,400,000 6,938 4.50Manitoba (Provence of) (MTN) 6.5000 22/09/17 1,500,000 1,794 1.16Ontario (Provence of) 4.4000 08/03/16 2,000,000 2,157 1.40Quebec 6.0000 01/10/29 5,000,000 6,070 3.94131,951 85.57Government bonds 131,951 85.57Total transferable securities and money market instruments admitted to anofficial exchange listing / dealt in on another regulated market 146,767 95.18Total investments 146,767 95.18Other net assets 7,440 4.82Total 154,207 100.0026 <strong>Aberdeen</strong> <strong>Global</strong> <strong>II</strong>Canadian Dollar Bond

Convertible EuropeFor the period 24 September 2010 to 30 June 2011PerformanceFor the period 24 September 2010 to 30 June 2011, the value of Convertible Europe - A Accumulation shares increased by 4.94% comparedto an increase of 6.09% in the benchmark, UBS Europe Convertible Index.Source: Lipper, Basis: total return, NAV to NAV, net of annual charges, gross income reinvested, EUR.Corporate activityOn 24 September 2010, Credit Suisse Bond Fund (Lux) Convert Europe <strong>Aberdeen</strong> transferred its assets into the <strong>Aberdeen</strong> <strong>Global</strong> <strong>II</strong> -Convertible Europe Fund resulting in a contribution in kind worth €335 million in investments and cash.Shareholders involved in the transfer were either A or I shares in the <strong>Aberdeen</strong> <strong>Global</strong> <strong>II</strong> - Convertible Europe Fund for every 1 share previouslyheld in Credit Suisse Bond Fund (Lux) Convert Europe <strong>Aberdeen</strong> as follows:Contribution inCredit Suisse Bond Fund (Lux) Share Class <strong>Aberdeen</strong> <strong>Global</strong> <strong>II</strong> Share Classkind (‘000) Transfer RatioConvert Europe <strong>Aberdeen</strong> B Convertible Europe Fund A-2 €249,147 1.000000000Convert Europe <strong>Aberdeen</strong> I Convertible Europe Fund I-2 €86,211 1.000000000Manager’s reviewSince the second half of 2010 until the first quarter of 2011, theprospect of a sustainable economic recovery was greatly enhancedby the expansion of the global manufacturing sector and animproving labour market in the US. But those expectations wereto be challenged rapidly. First, the surge in oil prices followingthe political events in North Africa and the Middle East has liftedfears of a consumption slowdown. Thereafter, the natural disasterwhich affected Japan in March had a considerable negative impacton the global manufacturing sector. The third risk factor whichcontinued to exert a growing influence over the financial marketwas the European sovereign debt crisis. After the interest rates ofits sovereign debt reached unsustainable levels, Portugal became inApril the third state to demand financial support from the EuropeanUnion. In reaction to those multiple risk factors, financial marketparticipants downgraded their economic growth forecasts andall risky asset classes declined over the last two months ofthis semester.The European convertible bond market has benefited from risingequity and credit markets over the first three quarters of the period.Also, the asset class gained from a marked increase in convertiblebond valuations up until the month of March 2011. Since then,demand for the asset class from outright investors was reduceddue to the decline in equity markets, forcing convertible bonds’volatility valuations to weaken. The volume of new issuance waslow over the period, with around $21.9billion raised in Europe.Portfolio reviewThe Fund’s performance was below the benchmark overthe period.Our overweight position in terms of overall equity exposure wasbeneficial for the portfolio. However, our conservative positioning interms of credit, avoiding lower credit quality names, was detrimentalto the relative performance of the Fund, as credit spreads continuedto tighten by a larger extent in this segment. Security selection wasalso source of underperformance, the main examples being ourunderweight position in Alcatel and Bulgari which had exceptionalreturns over the period.OutlookWe have been surprised by the depth and the length of thecorrection in equities. However, we see two reasons to be positiveat present. First, it seems to us that equity markets have correctedas a result of rising risk aversion as opposed to deterioratingfundamentals. It currently makes European equities look remarkablycheap. Second, we think that European policy makers will engineera temporary solution for Greece which should help improve marketsentiment in the short run. For these reasons and considering thepotential impact of the summer seasonal effect, we would expecta rebound. We intend to maintain our slight overweight equitysensitivity.Despite the recent correction in credit spreads, we still think that it isworth trying to maintain a high level of carry in the portfolio as theoutlook for corporate cashflows remains positive.The correction in European convertible bond valuations has beenquite sharp, leaving a good entry point for new investors. Moreover,there are several large issues that are maturing in the coming weekswhich we think could push secondary market valuations higheras investors re-invest the cash. We will be looking to increaseour sensibility to higher valuation sensitive converts in thecoming weeks.<strong>Aberdeen</strong> <strong>Global</strong> <strong>II</strong> 27Convertible Europe