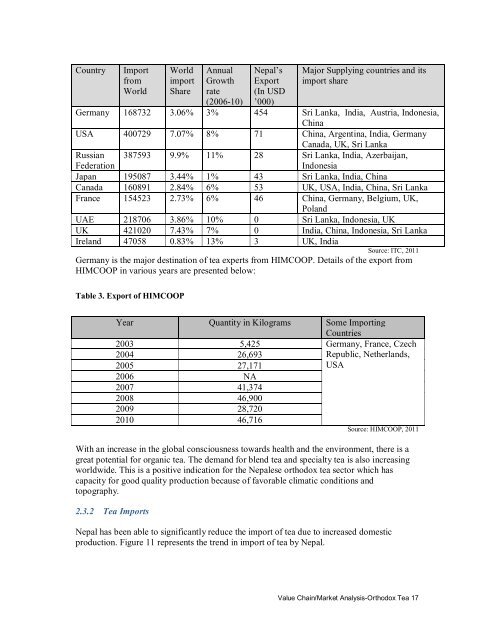

covers about 3 percent The green <strong>tea</strong> exported to India is also negligible. The major suppliersto India besides <strong>Nepal</strong> are Kenya, Indonesia, China, and Sri Lanka.Figure 10 Import data <strong>of</strong> <strong>tea</strong> <strong>of</strong> India (2009)29%71%India's import from <strong>Nepal</strong> (USD '000)India's import from o<strong>the</strong>r countries except <strong>Nepal</strong> (USD '000)According to a discussion with an Indian customs clearing agent, around 120 to 130truckloads <strong>of</strong> <strong>orthodox</strong> <strong>tea</strong> is exported from <strong>the</strong> Kakarbhitta border to India.Source: ITC, 2011<strong>Nepal</strong>ese traders usually sell <strong>the</strong>ir products to importers and commission agents in India. Themajor destinations <strong>of</strong> <strong>the</strong> <strong>Nepal</strong>ese <strong>tea</strong> in India are Kolkata and Siliguri. Some <strong>of</strong> <strong>the</strong><strong>Nepal</strong>ese exporters have <strong>the</strong>ir <strong>market</strong>ing <strong>of</strong>fices in Kolkata, India.Indias <strong>market</strong> is vast and has a high capacity for <strong>tea</strong>. Every grade <strong>of</strong> <strong>tea</strong> (whole leaf, broken,fanning, and dust) is sold in <strong>the</strong> Indian <strong>market</strong>. Most <strong>of</strong> <strong>the</strong> <strong>orthodox</strong> <strong>tea</strong> goes to India withoutany <strong>value</strong> addition. Much <strong>of</strong> <strong>the</strong> <strong>value</strong> addition is completed in India such as producing blend<strong>tea</strong>s, flavor <strong>tea</strong>s, and specialty <strong>tea</strong>s. <strong>Nepal</strong>ese exporters complain <strong>of</strong> <strong>the</strong> low prices received in<strong>the</strong> Indian <strong>market</strong>. <strong>Nepal</strong>ese <strong>tea</strong>s sell for lower prices than Darjeeling <strong>tea</strong>s. There is a greatopportunity for <strong>Nepal</strong>ese <strong>tea</strong> to continue exploring <strong>the</strong> lucrative <strong>market</strong> <strong>of</strong> India which is vastand expanding.Potential overseas <strong>market</strong> for <strong>Nepal</strong>ese <strong>orthodox</strong> <strong>tea</strong>In consultation with exporters, commodity organization (HOTPA, HIMCOOP), <strong>analysis</strong> <strong>of</strong>export/import data, and by literature review, some <strong>of</strong> <strong>the</strong> potential overseas <strong>market</strong> for<strong>Nepal</strong>ese <strong>orthodox</strong> <strong>tea</strong>s are USA, Russia, Canada, Germany, France, Japan, UAE, UK, andIreland. The NTIS 2010 has listed Egypt, UAE, Russia, USA, UK, Iran, Pakistan, Germany,Kazakhstan, and Australia as <strong>the</strong> 10 most attractive <strong>market</strong>s for export <strong>of</strong> <strong>Nepal</strong>ese <strong>tea</strong> (bothCTC and Orthodox combined) (MoCS, 2010). More detail is presented in <strong>the</strong> table below:Table 2 Import <strong>analysis</strong> <strong>of</strong> <strong>the</strong> potential countriesValue Chain/Market Analysis-Orthodox Tea 16

CountryImportfromWorldWorldimportShareAnnualGrowthrate(2006-10)<strong>Nepal</strong>sExport(In USD000)Major Supplying countries and itsimport shareGermany 168732 3.06% 3% 454 Sri Lanka, India, Austria, Indonesia,ChinaUSA 400729 7.07% 8% 71 China, Argentina, India, GermanyCanada, UK, Sri LankaRussianFederation387593 9.9% 11% 28 Sri Lanka, India, Azerbaijan,IndonesiaJapan 195087 3.44% 1% 43 Sri Lanka, India, ChinaCanada 160891 2.84% 6% 53 UK, USA, India, China, Sri LankaFrance 154523 2.73% 6% 46 China, Germany, Belgium, UK,PolandUAE 218706 3.86% 10% 0 Sri Lanka, Indonesia, UKUK 421020 7.43% 7% 0 India, China, Indonesia, Sri LankaIreland 47058 0.83% 13% 3 UK, IndiaSource: ITC, 2011Germany is <strong>the</strong> major destination <strong>of</strong> <strong>tea</strong> experts from HIMCOOP. Details <strong>of</strong> <strong>the</strong> export fromHIMCOOP in various years are presented below:Table 3. Export <strong>of</strong> HIMCOOPYear Quantity in Kilograms Some ImportingCountries2003 5,425 Germany, France, Czech2004 26,6932005 27,1712006 NA2007 41,3742008 46,9002009 28,7202010 46,716Republic, Ne<strong>the</strong>rlands,USASource: HIMCOOP, 2011With an increase in <strong>the</strong> global consciousness towards health and <strong>the</strong> environment, <strong>the</strong>re is agreat potential for organic <strong>tea</strong>. The demand for blend <strong>tea</strong> and specialty <strong>tea</strong> is also increasingworldwide. This is a positive indication for <strong>the</strong> <strong>Nepal</strong>ese <strong>orthodox</strong> <strong>tea</strong> sector which hascapacity for good quality production because <strong>of</strong> favorable climatic conditions andtopography.2.3.2 Tea Imports<strong>Nepal</strong> has been able to significantly reduce <strong>the</strong> import <strong>of</strong> <strong>tea</strong> due to increased domesticproduction. Figure 11 represents <strong>the</strong> trend in import <strong>of</strong> <strong>tea</strong> by <strong>Nepal</strong>.Value Chain/Market Analysis-Orthodox Tea 17