- Page 1 and 2:

HEDGE FUNDSAND PRIVATE EQUITY -A CR

- Page 3 and 4:

The need for long-term investmentTh

- Page 5 and 6:

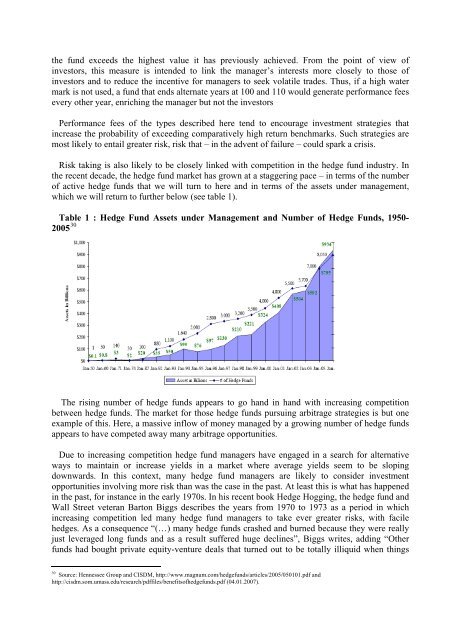

On the basis of a coherent analysis

- Page 7 and 8:

The pension fundsWhere does all the

- Page 9 and 10:

3. The target company is merged wit

- Page 11 and 12:

Societies’ response - current nat

- Page 13 and 14:

In most of the case studies, PE inv

- Page 15 and 16:

huge tax advantages when the rate o

- Page 17 and 18:

known to bank supervisors. Those da

- Page 19 and 20:

provide transparency with respect t

- Page 21:

The demand for change and better re

- Page 24 and 25:

industrial policy, focusing on know

- Page 26 and 27:

AcknowledgementsThis report has bec

- Page 28 and 29:

The situation we are facing now is

- Page 30 and 31:

market to promote the knowledge-eco

- Page 32 and 33:

Our desire to separate the single s

- Page 34 and 35:

Typically a single strategy HF oper

- Page 36 and 37:

In most European countries, fund ma

- Page 38 and 39:

It should also be signalled that:

- Page 40 and 41:

Institutional investorsCurrent and

- Page 42 and 43:

leverage in order to benefit from s

- Page 44 and 45:

1.6 The costs, the management fees

- Page 46 and 47:

only remaining way to boost returns

- Page 48 and 49:

A majority of hedge funds have limi

- Page 50 and 51:

Our analysis is that these concerns

- Page 52 and 53:

Average annual returnsTremont HF in

- Page 54 and 55:

1.11. Tendency of crowdingDespite t

- Page 56 and 57:

• Corporate governance:“In the

- Page 58 and 59:

Onshore FoHFsCountryUnitedKingdomGe

- Page 60 and 61:

ItalyBank ofItaly•Specializedasse

- Page 62 and 63:

1.14 Societies’ response - curren

- Page 64 and 65:

Investments are often in individual

- Page 66 and 67:

employed 21 . Leverage effect expla

- Page 68 and 69:

Investments are sold off to other c

- Page 70 and 71:

Private Equity: European trends in

- Page 72 and 73:

time because of the longer holding

- Page 74 and 75:

Bain CapitalPartners 74.7 9Thomas H

- Page 76 and 77:

Sources of new funds raised (2005)C

- Page 78 and 79:

The private equity manager virtuall

- Page 80 and 81:

The fund structuring arrangements f

- Page 82 and 83:

ownership transfers. But buyout cap

- Page 84 and 85:

equity value chain. The main areas

- Page 86 and 87: of the table but that less mature c

- Page 88 and 89: UCITS (Undertakings for Collective

- Page 90 and 91: Article 49Within the framework of t

- Page 92 and 93: open and secure retail markets and

- Page 94 and 95: offeree company must give its views

- Page 96 and 97: In its Communication on worker info

- Page 98 and 99: est practices, promoting innovative

- Page 100 and 101: - Work to ensure more consistent an

- Page 102 and 103: destabilising the financial markets

- Page 104 and 105: & LBOs invest. It increases financi

- Page 106 and 107: In particular, incumbent managers o

- Page 108 and 109: long-term competitiveness of the ac

- Page 110 and 111: It also leads to further weakening

- Page 112 and 113: If HFs and LBOs have brought uncert

- Page 114 and 115: the social responsibilities of comp

- Page 116 and 117: areas after recapitalisation 11 . I

- Page 118 and 119: Furthermore, the funds in many case

- Page 120 and 121: privatised with a view to stimulati

- Page 122 and 123: asset stripping, and the offering o

- Page 124 and 125: dividend to Valentia.The second pub

- Page 126 and 127: ***The three country case studies o

- Page 128 and 129: eturns well below those achieved by

- Page 130 and 131: investment funds - in the UK alone

- Page 132 and 133: 4.2 The issue of pension fundsThe p

- Page 134 and 135: One year earlier the British Financ

- Page 138 and 139: 5.3 Short sellingHistorically, hedg

- Page 140 and 141: global financial markets. In 1998 t

- Page 142 and 143: implications associated with the li

- Page 144 and 145: The classic source of leverage is l

- Page 146 and 147: I talk to have got a prayer in the

- Page 148 and 149: The main reason for the lack of inf

- Page 150 and 151: 7. The need for change to ensure a

- Page 152 and 153: clearly destructive must be prevent

- Page 154 and 155: European Union.Part III is going to

- Page 156 and 157: 2. Market transparency - a common i

- Page 158 and 159: International Settlements in Switze

- Page 160 and 161: 3.2 The main beneficiaries of regul

- Page 162 and 163: within jurisdictions with enhanced

- Page 164 and 165: In our view, if we want to promote

- Page 166 and 167: investors.The EC should set up an i

- Page 168 and 169: Alternative investment fund manager

- Page 170 and 171: widely differing impacts of PE acti

- Page 172 and 173: estrict investment to specific asse

- Page 174 and 175: Clearly the governance authorities

- Page 176 and 177: paid. There is therefore a need for

- Page 178 and 179: 5. Our immediate proposalsIn the pa

- Page 180 and 181: isks are honestly and clearly commu

- Page 182 and 183: Corporate governance provisionsLong

- Page 184 and 185: ANNEX 1 - Case studiesANNEX 1 - Cas

- Page 186 and 187:

1. Company description ............

- Page 188 and 189:

AA1. Company descriptionThe Automob

- Page 190 and 191:

Autoteile Unger1. Company descripti

- Page 192 and 193:

Bulgarian Telecommunications Compan

- Page 194 and 195:

Deutsche Börse1. Company descripti

- Page 196 and 197:

DIS1. Company descriptionThe DIS De

- Page 198 and 199:

DT-GROUP1. Company descriptionDT Gr

- Page 200 and 201:

(2005 €610m) resulting in an EBIT

- Page 202 and 203:

FRANS BONHOMME1. Company descriptio

- Page 204 and 205:

Friedrich Grohe AG1. Company descri

- Page 206 and 207:

3. LBO exit (secondary LBO, IPO, li

- Page 208 and 209:

industrial sector level. A compromi

- Page 210 and 211:

Linde1. Company descriptionLinde is

- Page 212 and 213:

2.5 Protection of minority sharehol

- Page 214 and 215:

marketing outside Germany and to bo

- Page 216 and 217:

2.3 Effects on job creation, invest

- Page 218 and 219:

Peguform1. Company descriptionThe h

- Page 220 and 221:

PICARD1. Company descriptionPicard

- Page 222 and 223:

STORK1. Company descriptionThe indu

- Page 224 and 225:

TDC1. Company descriptionTDC is the

- Page 226 and 227:

TELECOM ITALIA GROUP1. Company desc

- Page 228 and 229:

2.5 Corporate governance and econom

- Page 230 and 231:

same way like some institutional in

- Page 232 and 233:

Viterra1. Company descriptionViterr

- Page 234 and 235:

Glossary 1Absolute returns: The ret

- Page 236 and 237:

Hurdle rate: A rate of return that

- Page 238:

Stock option: An individual's right