A Practical Guide to SR&ED in 2011 - CCH Canadian

A Practical Guide to SR&ED in 2011 - CCH Canadian

A Practical Guide to SR&ED in 2011 - CCH Canadian

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

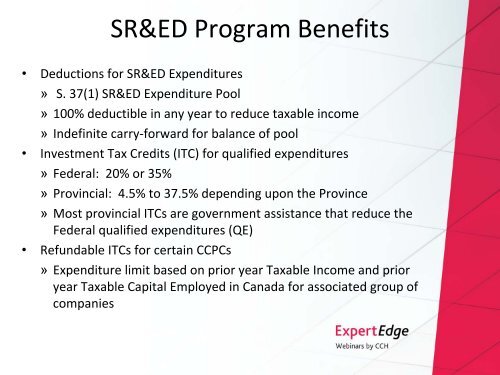

SR&<strong>ED</strong> Program Benefits• Deductions for SR&<strong>ED</strong> Expenditures» S. 37(1) SR&<strong>ED</strong> Expenditure Pool» 100% deductible <strong>in</strong> any year <strong>to</strong> reduce taxable <strong>in</strong>come» Indef<strong>in</strong>ite carry‐forward for balance of pool• Investment Tax Credits (ITC) for qualified expenditures» Federal: 20% or 35%» Prov<strong>in</strong>cial: 4.5% <strong>to</strong> 37.5% depend<strong>in</strong>g upon the Prov<strong>in</strong>ce» Most prov<strong>in</strong>cial ITCs are government assistance that reduce theFederal qualified expenditures (QE)• Refundable ITCs for certa<strong>in</strong> CCPCs» Expenditure limit based on prior year Taxable Income and prioryear Taxable Capital Employed <strong>in</strong> Canada for associated group ofcompanies