A Practical Guide to SR&ED in 2011 - CCH Canadian

A Practical Guide to SR&ED in 2011 - CCH Canadian

A Practical Guide to SR&ED in 2011 - CCH Canadian

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

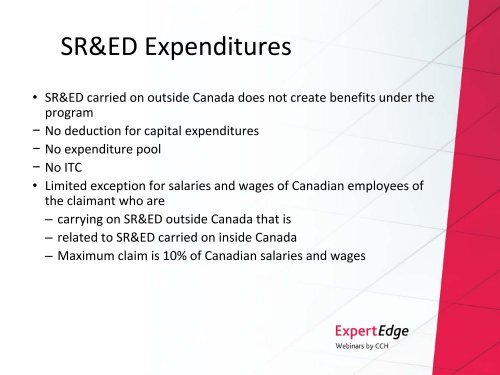

SR&<strong>ED</strong> Expenditures• SR&<strong>ED</strong> carried on outside Canada does not create benefits under theprogram− No deduction for capital expenditures− No expenditure pool− No ITC• Limited exception for salaries and wages of <strong>Canadian</strong> employees ofthe claimant who are– carry<strong>in</strong>g on SR&<strong>ED</strong> outside Canada that is– related <strong>to</strong> SR&<strong>ED</strong> carried on <strong>in</strong>side Canada– Maximum claim is 10% of <strong>Canadian</strong> salaries and wages