A Practical Guide to SR&ED in 2011 - CCH Canadian

A Practical Guide to SR&ED in 2011 - CCH Canadian

A Practical Guide to SR&ED in 2011 - CCH Canadian

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

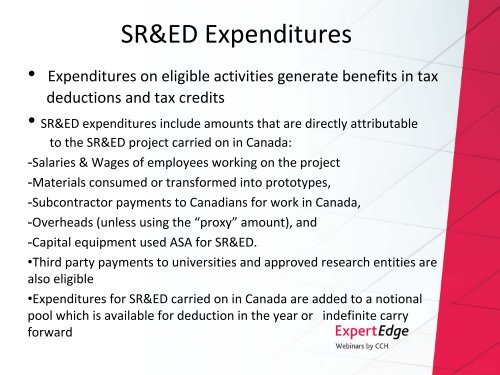

SR&<strong>ED</strong> Expenditures• Expenditures on eligible activities generate benefits <strong>in</strong> taxdeductions and tax credits• SR&<strong>ED</strong> expenditures <strong>in</strong>clude amounts that are directly attributable<strong>to</strong> the SR&<strong>ED</strong> project carried on <strong>in</strong> Canada:-Salaries & Wages of employees work<strong>in</strong>g on the project-Materials consumed or transformed <strong>in</strong><strong>to</strong> pro<strong>to</strong>types,-Subcontrac<strong>to</strong>r payments <strong>to</strong> <strong>Canadian</strong>s for work <strong>in</strong> Canada,-Overheads (unless us<strong>in</strong>g the “proxy” amount), and-Capital equipment used ASA for SR&<strong>ED</strong>.•Third party payments <strong>to</strong> universities and approved research entities arealso eligible•Expenditures for SR&<strong>ED</strong> carried on <strong>in</strong> Canada are added <strong>to</strong> a notionalpool which is available for deduction <strong>in</strong> the year or <strong>in</strong>def<strong>in</strong>ite carryforward