Low interest rates pressuring US bank margins - Deutsche Bank ...

Low interest rates pressuring US bank margins - Deutsche Bank ...

Low interest rates pressuring US bank margins - Deutsche Bank ...

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Research Briefing<br />

Global financial markets<br />

May 11, 2012<br />

Authors<br />

Jan Schildbach<br />

+49 69 910-31717<br />

jan.schildbach@db.com<br />

Sarah Lantz, Robert Bosch Stiftung Fellow<br />

Editor<br />

Bernhard Speyer<br />

<strong>Deutsche</strong> <strong>Bank</strong> AG<br />

DB Research<br />

Frankfurt am Main<br />

Germany<br />

E-mail: marketing.dbr@db.com<br />

Fax: +49 69 910-31877<br />

www.dbresearch.com<br />

Managing Director<br />

Thomas Mayer<br />

<strong>Low</strong> <strong>interest</strong> <strong>rates</strong> <strong>pressuring</strong><br />

<strong>US</strong> <strong>bank</strong> <strong>margins</strong><br />

— With <strong>interest</strong> <strong>rates</strong> likely to remain at depressed levels for years<br />

to come in most developed <strong>bank</strong>ing markets, the focus is on<br />

the impact this may have on <strong>interest</strong> <strong>margins</strong> and <strong>bank</strong>s’ net<br />

<strong>interest</strong> income.<br />

— Historical data for the <strong>US</strong> shows that with a flattening of the<br />

yield curve, <strong>margins</strong> face significant pressure as long-term<br />

<strong>rates</strong> draw closer to short-term <strong>rates</strong>. This margin compression<br />

is exacerbated as funding costs approach the zero bound,<br />

while asset yields continue to fall.<br />

— Whether the recent uptick in <strong>US</strong> commercial lending volumes<br />

will compensate for the negative price effect from lower <strong>interest</strong><br />

<strong>margins</strong> on overall net <strong>interest</strong> income remains in doubt.<br />

The <strong>US</strong> <strong>bank</strong>ing industry in 2011 was a strongly profitable one: return on assets<br />

rose across <strong>bank</strong>s of all sizes and net income was close to pre-crisis levels. A<br />

closer look, however, reveals this profitability was mainly a result of lower loan<br />

loss provisions. Provisions declined year-over-year for the ninth consecutive<br />

quarter, but now appear to be levelling off. Whether or not <strong>bank</strong>s can continue<br />

these profitability trends remains a key concern in the near term given sluggish<br />

credit growth and a lingering low-<strong>interest</strong> rate environment.<br />

Despite the growing importance of non-<strong>interest</strong> income sources such as fees,<br />

much focus is currently on <strong>bank</strong>s’ primary revenue driver, net <strong>interest</strong> income<br />

(which, in 2011, represented more than 64% of total <strong>US</strong> <strong>bank</strong> revenues). Net<br />

<strong>interest</strong> income is a reflection of <strong>bank</strong>s’ traditional earnings strategy: the rate<br />

spread between borrowing short and lending long, or more broadly the<br />

differential between asset yields and funding costs. In previous recessions, <strong>bank</strong><br />

balance sheets benefited from lower <strong>interest</strong> <strong>rates</strong> as funding costs dropped<br />

more quickly than asset <strong>rates</strong>. In fact, <strong>US</strong> <strong>bank</strong>s expanded net <strong>interest</strong> income<br />

by 7% p.a. between 2007 and 2010. As low <strong>rates</strong> persist, however, loan-todeposit<br />

spreads fall as prices adjust, and longer-term securities, held as assets,<br />

roll over to lower-yielding securities (the same holds true on the funding side, of<br />

course, helping to extend the positive impact of falling <strong>interest</strong> <strong>rates</strong> into the<br />

future). The net impact on <strong>bank</strong>s’ net <strong>interest</strong> levels may be negative, though. In<br />

previous recoveries, this effect has been offset by increased loan volumes,<br />

allowing <strong>bank</strong>s to return to sustainable growth levels. Furthermore, as an<br />

economy recovers, <strong>bank</strong>s may quickly benefit as short-term assets roll over at<br />

higher <strong>rates</strong>.

<strong>Low</strong> <strong>interest</strong> <strong>rates</strong> <strong>pressuring</strong> <strong>US</strong> <strong>bank</strong> <strong>margins</strong><br />

The current <strong>bank</strong>ing environment is not conforming to history, however. The<br />

initial benefit of low <strong>rates</strong> has waned without the concurrent growth in lending.<br />

Although funding costs continue to decline, they may not be enough to offset<br />

lower asset yields and they are approaching a limit of zero (see chart 1). With<br />

the Fed announcing no intention to raise <strong>rates</strong> until the end of 2014, this limit<br />

could quickly constrain <strong>bank</strong> profitability. Although there are indicators of a pickup<br />

in lending across recent quarters, it may not be enough to make up for the<br />

compression in net <strong>interest</strong> income. Furthermore, alternative revenue drivers<br />

like non-<strong>interest</strong> income so far have not provided much support.<br />

Funding costs on a downward trend, nearing zero bound 1<br />

%<br />

12<br />

10<br />

8<br />

6<br />

4<br />

2<br />

0<br />

84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11<br />

Sources: St. Louis Fed, FDIC<br />

Asset yields Funding costs of earning assets Fed funds rate<br />

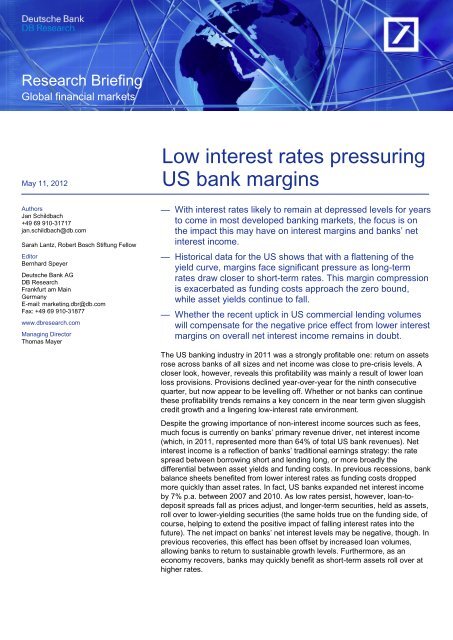

Net <strong>interest</strong> <strong>margins</strong> (defined as net <strong>interest</strong> income over average earning<br />

assets) were 3.6% at year-end 2011, just 11% higher from the 20-year low of<br />

3.2% in the last quarter of 2006 (see chart 2). After the initial benefit from low<br />

<strong>rates</strong>, net <strong>interest</strong> <strong>margins</strong> are likely to continue to trend downwards as funding<br />

costs bottom out and asset yields continue to fall. The chart below demonst<strong>rates</strong><br />

that net <strong>interest</strong> <strong>margins</strong> spiked not only after the most recent crisis but also<br />

during previous recessionary rate environments, as evidenced during the <strong>US</strong><br />

recession in the early 1990s and again in 2001-02. In the second half of the<br />

1980s, the decline in inflation and the reduction in the Fed funds rate led to a<br />

corresponding surge in net <strong>interest</strong> <strong>margins</strong>.<br />

More precisely, it may be the shape of the yield curve (which is heavily<br />

influenced by the official <strong>interest</strong> rate) that largely determines the <strong>interest</strong><br />

margin. The spread between 10- and 2-year Treasuries demonst<strong>rates</strong> that as<br />

the yield curve flattens or becomes inverted (indicated in chart 2 by near-zero or<br />

negative values), net <strong>interest</strong> <strong>margins</strong> tend to fall. For example, at the recent net<br />

<strong>interest</strong> margin low in late-2006, the yield curve was inverted. By contrast, as<br />

spreads widen, net <strong>interest</strong> <strong>margins</strong> follow suit. The yield curve is likely to<br />

continue its flattening trend as long-term <strong>rates</strong> draw closer to short-term <strong>rates</strong>.<br />

The Fed’s recent “Operation Twist” is explicitly targeting lower long-term <strong>rates</strong>,<br />

with the intention of boosting credit volume in products that track longer-term<br />

Treasury yields such as mortgages and corporate bonds. As a result, further<br />

compressions in net <strong>interest</strong> <strong>margins</strong> are likely in the near term.<br />

2 | May 11, 2012 Research Briefing

<strong>Low</strong> <strong>interest</strong> <strong>rates</strong> <strong>pressuring</strong> <strong>US</strong> <strong>bank</strong> <strong>margins</strong><br />

Considering <strong>rates</strong> are likely to be sustained at low levels for the foreseeable<br />

future, how long can lower provisions cover for the sluggish credit environment?<br />

In recent quarters, <strong>bank</strong>s have benefited from lower reserves to protect<br />

profitability, but indicators show that this trend is levelling off. It is clear that loan<br />

growth will be the critical factor to offset the negative impact of <strong>interest</strong> <strong>rates</strong>.<br />

Lending, driven primarily by commercial and industrial loans, grew for the third<br />

consecutive quarter through the end of 2011. Nevertheless, the housing market<br />

remains sluggish and it remains unclear whether the increase in non-consumer<br />

credit volumes will compensate for a lower net <strong>interest</strong> margin in the near term.<br />

Jan Schildbach (+49 69 910-31717, jan.schildbach@db.com)<br />

Sarah Lantz<br />

© Copyright 2012. <strong>Deutsche</strong> <strong>Bank</strong> AG, DB Research, 60262 Frankfurt am Main, Germany. All rights reserved. When quoting please cite “<strong>Deutsche</strong><br />

<strong>Bank</strong> Research”.<br />

The above information does not constitute the provision of investment, legal or tax advice. Any views expressed reflect the current views of the author,<br />

which do not necessarily correspond to the opinions of <strong>Deutsche</strong> <strong>Bank</strong> AG or its affiliates. Opinions expressed may change without notice. Opinions<br />

expressed may differ from views set out in other documents, including research, published by <strong>Deutsche</strong> <strong>Bank</strong>. The above information is provided for<br />

informational purposes only and without any obligation, whether contractual or otherwise. No warranty or representation is made as to the correctness,<br />

completeness and accuracy of the information given or the assessments made.<br />

In Germany this information is approved and/or communicated by <strong>Deutsche</strong> <strong>Bank</strong> AG Frankfurt, authorised by Bundesanstalt für Finanzdienstleistungsaufsicht.<br />

In the United Kingdom this information is approved and/or communicated by <strong>Deutsche</strong> <strong>Bank</strong> AG London, a member of the London<br />

Stock Exchange regulated by the Financial Services Authority for the conduct of investment business in the UK. This information is distributed in Hong<br />

Kong by <strong>Deutsche</strong> <strong>Bank</strong> AG, Hong Kong Branch, in Korea by <strong>Deutsche</strong> Securities Korea Co. and in Singapore by <strong>Deutsche</strong> <strong>Bank</strong> AG, Singapore<br />

Branch. In Japan this information is approved and/or distributed by <strong>Deutsche</strong> Securities Limited, Tokyo Branch. In Australia, retail clients should obtain a<br />

copy of a Product Disclosure Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any<br />

decision about whether to acquire the product.<br />

Internet/E-mail: ISSN 2193-5963<br />

Interest <strong>margins</strong> follow the yield curve 2<br />

%<br />

15<br />

13<br />

11<br />

9<br />

7<br />

5<br />

3<br />

1<br />

-1<br />

84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11<br />

Fed funds rate (left) 10-Yr over 2-Yr Treasury yields (left) Net <strong>interest</strong> margin (right)<br />

Sources: St. Louis Fed, FDIC, DB Research<br />

3 | May 11, 2012 Research Briefing<br />

4.3<br />

4.1<br />

3.9<br />

3.7<br />

3.5<br />

3.3<br />

3.1<br />

2.9<br />

2.7