IMPUESTO A LA RENTA - GASTOS DEDUCIBLES Y NO ...

IMPUESTO A LA RENTA - GASTOS DEDUCIBLES Y NO ...

IMPUESTO A LA RENTA - GASTOS DEDUCIBLES Y NO ...

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

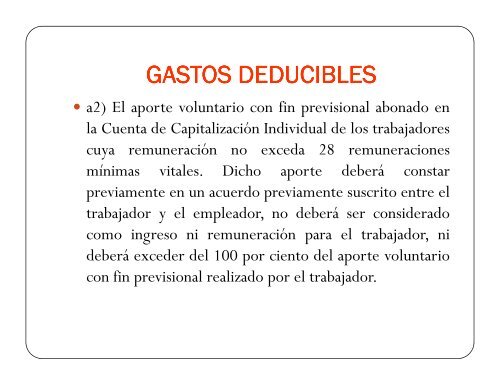

<strong>GASTOS</strong> <strong>GASTOS</strong> <strong>DEDUCIBLES</strong><br />

<strong>DEDUCIBLES</strong><br />

a2) El aporte voluntario con fin previsional abonado en<br />

la Cuenta de Capitalización Individual de los trabajadores<br />

cuya remuneración no exceda 28 remuneraciones<br />

mínimas vitales. Dicho aporte deberá constar<br />

previamente en un acuerdo previamente suscrito entre el<br />

trabajador y el empleador, no deberá ser considerado<br />

como ingreso ni remuneración para el trabajador, ni<br />

deberá exceder del 100 por ciento del aporte voluntario<br />

con fin previsional realizado por el trabajador.