Annual Report 2005 - Tenaris

Annual Report 2005 - Tenaris

Annual Report 2005 - Tenaris

Create successful ePaper yourself

Turn your PDF publications into a flip-book with our unique Google optimized e-Paper software.

Explanatory notes<br />

74. <strong>Tenaris</strong>Confab<br />

c. Dividends and interest on capital<br />

Preferential shares, which do not have voting rights, have<br />

priority on the return of capital, as well as the preferential<br />

right to receipt of fixed non-cumulative dividends of 8%<br />

per year on that portion of the capital attributable to them,<br />

which take priority in payment above all other classes of<br />

shares. After payment of the 8% on the preferred shares,<br />

the ordinary shares are guaranteed the same participation<br />

in profits, being at least equivalent to 25% of adjusted net<br />

profit, whichever is the greater of the two.<br />

In accordance with tax legislation, the company opted to<br />

pay interest to shareholders on capital in line with the<br />

mandatory dividend for <strong>2005</strong> of R$ 41,006. These interest<br />

Net profit for year<br />

Legal reserve<br />

Basis of calculation of dividends<br />

Proposed complementary dividends<br />

Interest on own capital<br />

Total dividends paid out<br />

Percentage of net earnings of year<br />

payments were approved in meetings of the Board held<br />

on July 26 and November 3 <strong>2005</strong> and were paid out on<br />

September 13 and December 2 <strong>2005</strong>.<br />

Although for tax purposes the interest on capital has been<br />

recognized in the results, for purposes of the financial<br />

reports it has been restated as shareholders equity.<br />

Additionally, the Company will be proposing to the<br />

Ordinary General Assembly complementary dividends<br />

of R$ 24,781.<br />

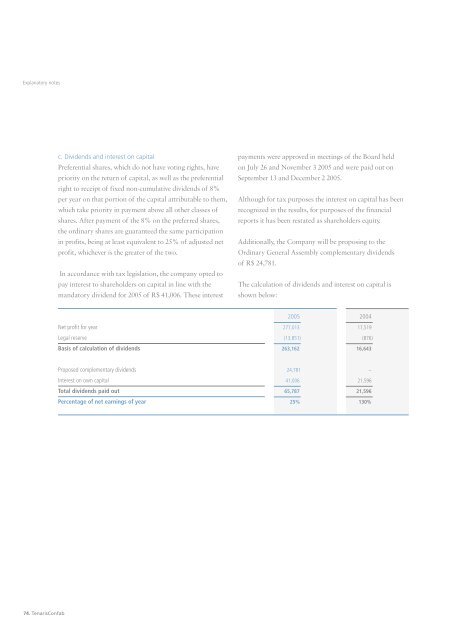

The calculation of dividends and interest on capital is<br />

shown below:<br />

<strong>2005</strong><br />

277,013<br />

(13,851)<br />

263,162<br />

24,781<br />

41,006<br />

65,787<br />

25%<br />

2004<br />

17,519<br />

(876)<br />

16,643<br />

–<br />

21,596<br />

21,596<br />

130%