Basics of Credit Risk - Universität Hohenheim

Basics of Credit Risk - Universität Hohenheim

Basics of Credit Risk - Universität Hohenheim

You also want an ePaper? Increase the reach of your titles

YUMPU automatically turns print PDFs into web optimized ePapers that Google loves.

Investment Banking and Capital Markets – <strong>Universität</strong> <strong>Hohenheim</strong><br />

Investment Banking and Capital Markets<br />

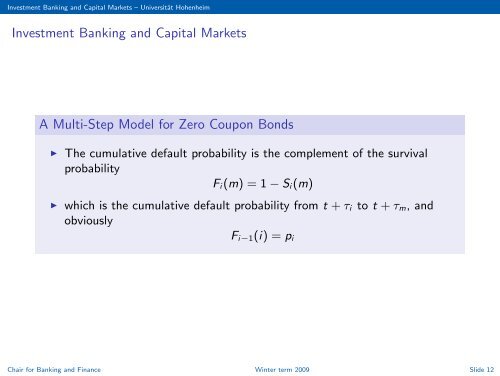

A Multi-Step Model for Zero Coupon Bonds<br />

◮ The cumulative default probability is the complement <strong>of</strong> the survival<br />

probability<br />

Fi(m) = 1 − Si(m)<br />

◮ which is the cumulative default probability from t + τi to t + τm, and<br />

obviously<br />

Fi−1(i) = pi<br />

Chair for Banking and Finance Winter term 2009 Slide 12